Written by : Knowledge Centre Team

2026-07-23

9127 Views

13 minutes read

Share

Every Indian citizen is responsible for paying income tax and filing income tax returns. This is a good practice that helps you recover TDS (tax deducted at source) payments. The government uses your taxes as a major source of revenue for important public programs and services.

One such tool that can be leveraged for such benefits is insurance. A term plan or a life insurance plan can offer tax reduction and savings provisions that can reduce your eventual payable amount. However, the key element to get those tax benefits is filing the return timely. Sections 234 A, B, and C of the Income Tax Act cover related regulations.

In this blog, let us learn more about these sections and how to avoid interest imposition due to delayed tax filing.

Key Takeaways

|

Timely tax compliance is a crucial aspect of financial planning, and the Income Tax Act of India enforces this through interest provisions under Sections 234A, 234B, and 234C. These sections impose interest penalties on taxpayers who delay filing their returns, fail to pay advance tax on time, or fall short in their tax payments.

The primary objective of these sections is to ensure that taxpayers fulfil their obligations promptly and understand the consequences of not doing so. The interest serves as a deterrent against delays and shortfalls, encouraging disciplined tax payment habits. It also compensates the government for the time value of money lost due to late payments.

An important aspect of this is advance tax, which plays a key role in preventing interest charges under Sections 234A, 234B, and 234C. Since these provisions penalise delays and shortfalls in tax payments, ensuring timely and adequate advance tax payments can help taxpayers avoid unnecessary interest and maintain smooth compliance.

Advance tax refers to the payment of income tax in instalments throughout the financial year instead of making a lump sum payment at the end. It is also known as the "pay as you earn" tax system. This ensures a steady inflow of revenue for the government and helps taxpayers avoid a heavy tax burden at the end of the year.

Any individual or business whose total tax liability exceeds ₹10,000 in a financial year must pay advance tax. This includes:

Salaried individuals with additional income from investments, freelancing, or rental earnings

Self-employed professionals such as doctors, lawyers, and consultants

Businesses with taxable income

Taxpayers earning from capital gains, dividends, or interest

Senior citizens (aged 60 and above) who do not have business income are exempt from advance tax payments.

Assessed tax refers to the total tax liability after deducting TDS, TCS, and advance tax already paid. It forms the basis for calculating interest under Section 234B. The Interest is charged at 1% per month or part of a month on the assessed tax. The levy starts from 1st April of the assessment year until the date of actual payment.

Example: If a taxpayer’s total tax liability is ₹1,00,000 and only ₹70,000 was paid as advance tax, interest is levied on the remaining ₹30,000 from 1st April until the payment date.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Understanding the timeline for advance tax payments helps plan finances and avoid interest or penalties. Both corporate and non-corporate assessees are expected to deposit advance tax in instalments spread across the financial year. The table below outlines the advance tax schedule for Assessment Year 2025-26 so you can stay compliant and organised:

| Due Date (AY 2025-26) | Advance Tax Payable (Non-Corporate Assessees) | Advance Tax Payable (Corporate Assessees) |

|---|---|---|

| 15th June | 15% of Total Tax | 15% of Total Tax |

| 15th September | 45% of Total Tax (Cumulative) | 45% of Total Tax |

| 15th December | 75% of Total Tax (Cumulative) | 75% of Total Tax |

| 15th March | 100% of Total Tax | 100% of Total Tax |

With proper planning, one can maintain timely tax payments. However, if not planned on time, you might end up delaying your payments.

The 3 types of interest covered under section 234 are:

Section 234A of the Income Tax Act provides details for delays in filing income tax returns

Section 234B of the Income Tax Act covers delays in the payment of the advance taxes

Section 234C of the Income Tax Act is for postponed payments of advance taxes

Let us have a look at all of them in detail.

The interest levied for delay in filing the return of income comes under section 234A of the Income Tax Act. If the taxpayer files their income tax return after the due date specified by the authorities, an interest under this section will be levied.

Example: Let’s assume Mr. X has an outstanding amount of ₹2,00,000, which includes his net advance tax plus TDS for AY 2025-26. The due date for filing his return was July 31, 2025. He files his returns on December 3, 2025. He is hence, late by five months (August, September, October, November, December are counted as full months). His interest will thus be:

₹2,00,000 X 1% X 5 = ₹10,000

Mr. X will now pay an additional ₹10,000. If he continues to not pay his dues, an additional interest of 1% will be added every month.

Interest u/s 234B of the Income Tax Act is levied in the following two cases:

If the taxpayer has failed to pay advance tax, which he is liable to pay if his estimated tax liability for the year is ₹10,000 or more, or

If the advance tax paid by the taxpayer is less than 90% of the assessed tax, which is the amount of tax as calculated under section 143(1) and where regular assessment is made, the tax on the total income determined under such regular assessment.

Let’s retake the example of Mr X, and assume that he has a payable tax amount of ₹1,00,000.

The TDS calculated is ₹82,650. This makes the Assessed Tax (1,00,000- 82,650) = ₹17,350. He should’ve paid a minimum of ₹15,615 (90% of ₹17,350) by the 15th of June, 2025. However, let’s assume he had paid only ₹6,000 on the due date and the rest on November 15, 2025.

Now, he will pay the following interest.

₹15,615 X 1% X 5 months (delay) = ₹781 (rounded off)

Rate of Interest under Section 234B: Interest under 234B is levied for default in payment of advance tax. Interest is levied at 1% per month or part of a month. The interest needs to be paid is simple interest. The taxpayer is liable to pay simple interest at 1% per month or part of a month for default in payment of advance tax.

Period of Levy of Interest: Interest under section 234B is levied from the first day of the assessment year (mostly from 1st April) till the date of determination of income under section 143(1) or when a regular assessment is made. In cases where the income is increased based on the assessment or re-computation, the interest is levied on the differential amount from the first day of the assessment year till the date of assessment or re-computation.

Amount on which Interest is to be Levied: The taxpayer is liable to pay interest on the amount as follows:

If the taxpayer has failed to pay advance tax on the amount equal to the assessed tax, or

If the advance tax paid by the taxpayer is less than 90% of the assessed tax, the amount by which the advance tax paid as aforesaid falls short of the assessed tax.

Example 1: Monica’s total tax liability was ₹50,000 in the previous year.

She paid her income tax on 15th July during the ITR filing.

There was no TDS deduction.

But since her total tax liability was more than ₹10,000, she was liable for the advance tax. However, she didn’t pay the advance tax

Hence, now Monica has to pay the interest u/s 234B of the Income Tax Act

Here is the amount of Interest she has to pay:

50,000 x 1% x 4 (April, May, June, July) = ₹2,000 is the amount of interest Monica has to pay towards interest under section 234B.

Example 2: Manav had a total tax payable of ₹50,000.

Out of this, he has paid ₹44,000 on 29th March as the advance tax. He paid the remaining ₹6,000 while filing his income tax return on 30th May.

Now, you can see that he has paid less than 90% of the assessed advance tax. The assessed tax of ₹50,000 is ₹45,000.

Hence, Manav has to pay the interest under section 234B.

Here is the amount of interest he has to pay:

Difference between assessed advance tax: 50,000 (assessed advance tax) – ₹44,000 (advance tax paid) = 6,000

Interest to be paid: 6000 x 1% x 2 (April and May) = ₹120 is the amount payable towards the interest under section 234B.

Section 234C of the Income Tax Act defines the rate of interest and conditions if you delay the advance tax instalments. Everyone, including salaried taxpayers, is required to pay advance tax every quarter of the financial year.

If your advance tax instalments have been delayed, you are required to pay a penalty as defined in section 234C of the Income Tax Act. Interest u/s 234C is levied in case of deferment of different instalments of advance tax in the following cases:

For taxpayers other than those who have opted for a presumptive taxation scheme under section 44AD or section 44ADA, interest shall be levied:

If the advance tax paid on or before the 15th day of June is less than 12% of the tax payable on the returned income,

If the advance tax paid on or before the 15th day of September is less than 36% of the tax payable on the returned income,

If the advance tax paid on or before the 15th day of December is less than 75% of the tax payable on the returned income and

If the advance tax paid on or before the 15th day of March is less than 100% of the total tax due on the returned income.

For taxpayers who have opted for a presumptive taxation scheme under section 44AD or section 44ADA, interest shall be levied if the advance tax paid on or before the 15th day of March is less than 100% of the tax due on the returned income.

Late payment interest under this Section 234C is applied at the rate of 1% on the outstanding amount of tax, starting from the individual dates listed above up to the payment date.

Rate of Interest under Section 234C: Interest u/s 234C for default in payment of instalments of advance tax is levied at 1% per month or part of a month. The taxpayer is liable to pay simple interest at 1% per month or part of a month for short payment/non-payment of an individual’s instalments of advance tax.

Period of Levy of Interest: Interest u/s 234C is levied for a period of 1 month in case of a shortfall in payment of the last instalment and a period of 3 months in case of a shortfall in payment of the first, second, and third instalments.

Amount on which Interest is to be Levied: The taxpayer shall be liable to pay interest on the shortfall of advance tax on respective individual instalments in case of shortfall therein.

Situations Where Section 234C is Applicable:

The advance tax instalment is less than the required percentage on the due date

No advance tax is paid, leading to a lump-sum payment at the end of the year

Sudden spike in income in the last quarter, making earlier instalments inadequate

Exceptions to the Levy of Interest Under Section 234C:

If the shortfall in advance tax is due to capital gains or income from lottery winnings, and the taxpayer pays the due tax in the next advance tax instalment

If the taxpayer is a senior citizen (60+ years) not having a business income, they are exempt from advance tax and thus not liable under Section 234C

Understanding the calculation of interest under Sections 234A, 234B, and 234C helps taxpayers estimate their penalties accurately. It also encourages better tax planning.

Whether the delay relates to filing your return or paying advance tax on time, each section applies a specific method for computing interest. To make this easier, here is a simple step-by-step approach that shows how the calculation works and how the interest amount is derived:

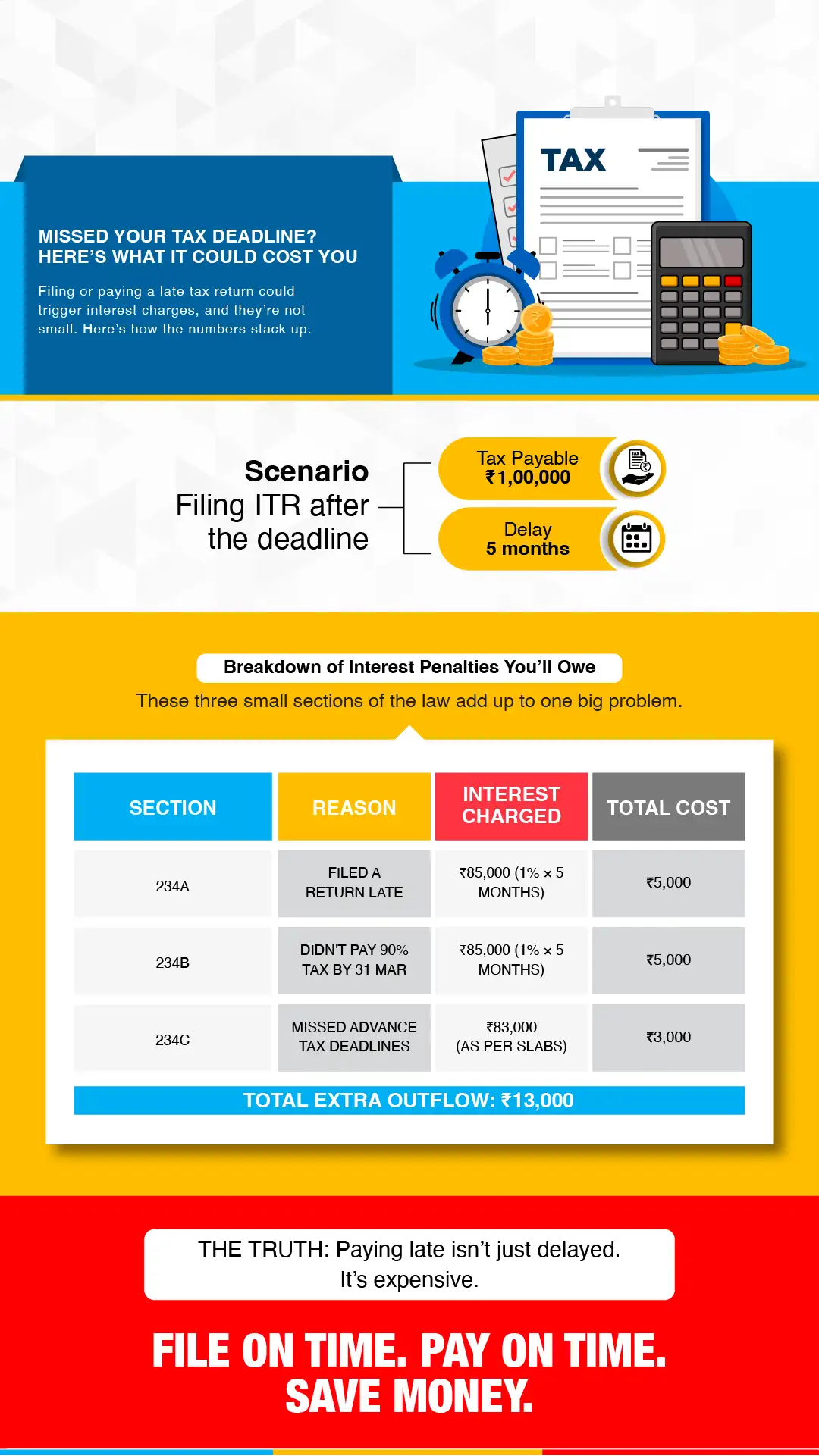

Example:

Tax payable for AY 2025-26: ₹1,00,000

Illustration for Late Payment: Combined 234A and 234B

Assume Mr. A has a total tax liability of ₹1,20,000 for AY 2025-26. He paid only ₹80,000 as advance tax by March 15, 2025. The final ITR filing due date was July 31, 2025. He filed his return and paid the remaining tax on November 30, 2025.

Section 234A (Late filing interest):

Interest on the shortfall of ₹40,000 from April 1, 2025 to July 31, 2025 (until the ITR due date). Note: 234B stops when 234A starts.

Total interest penalty = ₹1,600 (234A) + ₹1,600 (234B) = ₹3,200

Section 234C interest is calculated if the advance tax installments paid by the specific quarterly dates fall short of the minimum required cumulative percentage (15%, 45%, 75%, 100%). The interest is levied at 1% for a fixed period (3 months for the first three installments, and 1 month for the last one) on the amount of the shortfall.

| Payment Due Dates | Minimum Req. Cumulative Tax Paid | Actual Advance Tax paid | Shortfall Amount | Interest Calculation (Rate x Duration) | Penalty Amount |

|---|---|---|---|---|---|

| 15th June | 15% (₹15,000) | 5,000 | 10,000 | @1% x 3 months | ₹300 |

| 15th September | 45% (₹45,000) | 25,000 | 20,000 | @1% x 3 months | ₹600 |

| 15th December | 75% (₹75,000) | 35,000 | 40,000 | @1% x 3 months | ₹1,200 |

| 15th March | 100% (₹1,00,000) | 50,000 | 50,000 | @1% x 1 month | ₹500 |

Taxpayers can prevent unnecessary interest charges by following best practices for tax payments.

File returns on time: Ensure tax returns are submitted before the due date.

Check outstanding tax: Pay any outstanding tax before filing to avoid additional interest.

Use online filing platforms: Faster submission helps in meeting deadlines.

Pay at least 90% of your tax liability as advance tax before 31st March.

Regularly review income sources to estimate tax liability correctly.

Use Form 26AS to check TDS credits and avoid underpayment.

Follow the advance tax schedule: Pay the correct percentage of tax on the due dates.

Adjust for unexpected income: If you earn capital gains or windfall income, pay the tax in the next instalment to avoid penalties.

Use tax calculators to forecast and plan advance tax payments efficiently.

It is important to know details about these sections, but what is more important is keeping track of due dates and making payments on time. For reducing your tax liability, there are always life insurance and other instruments that also add value to your savings.

iSelect Smart360 Term Plan by Canara HSBC Life Insurance is a tailor-made plan with features such as return of premium, multiple payout options, increased coverage options, and tax benefits. You can also buy coverage for your spouse under the same plan. Plus, you will have the flexibility to choose from among various coverage options, premium payment, and benefit payout options. The best part is that all of this is just a few clicks away!

Some interests are urged upon the taxpayer in case there is a delay/non-payment of income tax. The interest penalty is calculated under sections 234A, 234B and 234C of the Income Tax Act.

Advance tax refers to income tax, which is required to be paid in the same year in which the income has been earned, that is, in advance. Advance tax is payable if an individual’s total payable tax in a financial year exceeds ₹10,000.

Interest Penalty = Outstanding Tax X 1% X Number of months (delayed), where a fraction of a month is considered as a full month. For example, if you are 4 months 10 days late, the interest will be charged for 5 months.

Assessed tax is the amount of tax as calculated under section 143(1), and where regular assessment is made, the tax on the total income is determined under such regular assessment.

There is no fee under Section 234A of the Income Tax Act. Section 234A imposes interest for delay in filing income tax returns.

An updated return is an income return that can be filed by a taxpayer through ITR-U. This is even if the taxpayer hasn't filed one before, within 24 months of the conclusion of the applicable assessment year. 25% or 50% of the additional tax that must be paid with these revised documents comes back.

Interest under Section 234A applies when you file your income tax return after the due date, and there is still some tax outstanding on that date. Interest at 1% per month is charged on the unpaid tax from the day after the due date until the actual filing date.

Section 234B applies when you were liable to pay advance tax but either did not pay any advance tax at all or paid less than 90% of the assessed tax. In such cases, interest at 1% per month is charged on the shortfall from the first day of the assessment year until the date you pay the tax.

If you file an updated return under Section 139(8A) and there is additional tax payable, interest under Section 234B is also levied on that extra liability. For this calculation, the advance tax you had already paid is considered only once. This means any extra tax disclosed in the updated return will attract additional interest under Section 234B.

Section 234C deals with interest for the deferment of advance tax instalments during the financial year. It is charged when the advance tax paid by the specified due dates is less than the prescribed percentage of the tax on your returned income, that is, the tax computed on the income you finally declare in your return after reducing TDS.

Interest under Section 234C is generally charged at 1% per month on the shortfall in the required advance tax instalment. For most taxpayers who are not under presumptive schemes, the law prescribes that by the June, September, December and March due dates, you should have paid at least 15%, 45%, 75%, and 100% of your total advance tax, respectively. Interest is calculated on any deficit arising from these milestones.

Section 234A covers interest for late filing of the income tax return when tax remains unpaid. Section 234B covers interest for default in payment of advance tax or paying less than 90% of the assessed tax as advance tax. Section 234C covers interest for delay or shortfall in each instalment of advance tax during the year.

You are charged interest under these sections because the law treats interest as compensation for the delay or short payment of tax that was due earlier. Section 234A applies if you filed your return late with tax still unpaid, Section 234B applies if you did not pay enough advance tax, and Section 234C applies if your advance tax instalments were not paid on time or were insufficient.

The law treats interest under Sections 234A, 234B, and 234C as mandatory in normal situations, and an old CBDT explanatory circular notes that there is no general power in the Act or Rules to waive this interest. However, CBDT has issued separate instructions allowing waiver or reduction in very specific cases of genuine hardship or natural calamities, and such relief is granted only through a special order by the Board or authorised officials.

Yes, TDS directly affects the computation of interest under these sections. For advance tax interest, “tax due on returned income” is defined explicitly as tax on the total income reduced by the TDS that should have been deducted, so higher TDS reduces the base on which 234B and 234C interest is calculated.

Interest under Section 234A is charged only on tax that remains unpaid as of the due date of filing the return. If your entire tax liability is already discharged through TDS, advance tax, and self-assessment tax before the due date, then no interest under Section 234A is levied even if the return is filed late.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.