Written by : Knowledge Centre Team

2026-06-03

13754 Views

9 minutes read

Share

Tax Deducted at Source (TDS) serves as a crucial mechanism for the government’s tax collection by directly deducting taxes from the source of income. This system alleviates the taxpayer's responsibility by allowing them to claim credit for the deducted taxes when filing their income tax returns, thus streamlining the tax payment process.

Section 194J is one of the numerous subsections of the Income Tax Act 1961 that addresses Tax Deducted at Source (TDS). It is a highly efficient method of tax collection as it reduces tax evasion. It benefits the government and taxpayers, but applies only to payments made through different professional or technical services.

Key Takeaways

|

Professional and technical service fees are among the most common payments under Section 194J and are further elaborated on in the blog. Paying professional or technical service fees is one of the most significant and frequent payment categories that organisations make. Fees paid to lawyers, doctors, engineers, architects, chartered accountants, interior decorators, advertisers, etc., are some examples of professional fees. The provision of management, technical, or consulting services is included in technical services.

Section 194J of the Income Tax Act covers payroll deduction for technical service providers and professionals. Before payment to the professional or technical service provider, the payer must subtract income tax at the source.

A person is only required to deduct Tax Deducted at Source (TDS) at the rate of 10% for professional services and 2% for technical services when payments are made to a specific resident, as per the guidelines of Section 194J of the Income Tax Act, 1961. The Indian government uses TDS to collect taxes from income sources.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Section 194J mandates the deduction of TDS (Tax Deducted at Source) on payments made for professional and technical services, royalty, non-compete fees, and remuneration to directors (excluding salary). Here’s an overview of who is responsible for making these deductions:

Section 194J TDS must be deducted by anyone (except individuals not covered under Section 44 (AB) who makes payments for professional or technical services. This includes:

Government bodies (central or state)

Enterprises (including public sector undertakings)

Cooperative organisations

Universities

Trusts

Businesses across industries

However, individuals are required to deduct TDS only if they are subject to audit under Section 44AA and 44AB in the previous fiscal year.

Section 194J applies to a wide range of specialised services where professional expertise or technical skills are involved. Whether a business hires consultants, technical experts, or creative professionals, this section ensures transparency and accountability in how such payments are taxed.

The section covers various types of services, including:

Professional Services: Medical, legal, architectural, engineering, accountancy, interior decoration, advertising, and technical consultancy services

Technical Services: Consultancy, technical, or managerial services

Other Specific Cases: Medical services in hospitals, professional fees charged by film artists, recruitment agency payments, etc

Additionally, individuals in the following categories are covered:

Film artists, company secretaries, and authorised representatives

Sportspersons, event managers, coaches, and other related professionals

The threshold for TDS deduction under Section 194J is tied to the amount of payment made in a fiscal year.

Below are the two key points regarding the threshold limits:

Professional and Technical Fees: Tax must be deducted at source only if the total payment for professional or technical services exceeds ₹30,000 in a financial year. This limit applies to each individual payment or item, not the aggregate sum.

Other Specific Payments: Certain other payments, such as non-compete fees and royalties, do not have a threshold limit. TDS must be deducted even if these payments are below ₹30,000.

Section 194J deals with payments that arise from skilled professional work or specialised services. These payments are often part of regular business operations, and the law ensures they are tracked correctly through TDS. Before making any such payment, it’s important to know whether it falls under this section so the correct tax can be deducted. The types of payments to residents covered under this section are as follows:

Supplying any information regarding expertise, experience, or understanding in the fields of technology, industry, commerce, or science

Before deducting tax under Section 194J, it is important to understand the applicable rates and thresholds. These limits help you determine how much tax must be withheld when making payments for professional, technical, or specialised services. The table below lists the TDS rate under Section 194J of the Income Tax Act:

| Nature of Payment | Tax Deduction Rate |

|---|---|

| Fee payments for technical services | 2% |

| Fee payments made to call centres | 2% |

| Royalty paid for the sale, distribution, or screening of a film | 2% |

| Other payments | 10% |

| If the payee fails to provide a PAN | 20% |

Once TDS is deducted, it must be deposited with the government within the prescribed timeline. Timely payment ensures smooth compliance and prevents interest or penalties. The deadlines vary depending on when the deduction is made and the type of deductor involved. The following is an overview of the time limits for government and non-government deductors:

| NPayment Type | Non-Government Deductors | Government Deductors |

|---|---|---|

| Payment made before 1st March | 7th day from the end of the month | 7th day from the end of the month |

| Payment made in March | April 30th | Tax payment is made on the date of the professional or technical fees to the payee. Still, the corresponding challan will be deposited by the 7th day at the end of March. |

Recent amendments to Section 194J of the Income Tax Act have led to significant changes regarding Tax Deductions at Source (TDS) for payments made for professional and technical services. Here’s an overview of the same:

The TDS rate for specialised services, previously classified under skilled professional services, is now set at 2%, while other payments remain at 10%.

Effective FY 2025 - 26, the threshold limit for TDS deduction under Section 194J has been revised from ₹30,000 to ₹50,000 in a financial year. This change provides additional compliance relief for small-scale service transactions.

Additionally, individuals and Hindu Undivided Families (HUFs) must deduct TDS if their turnover exceeds ₹1 crore from business or ₹50 lakh from profession in the prior financial year.

A crucial clarification has been made that payments under this section will not be classified as "work" under Section 194C, effective from October 1, 2024, preventing misapplication of tax provisions.

Failing to follow the TDS rules under Section 194J can lead to financial and legal complications for the deductor. The Income Tax Department treats timely deduction and deposit of TDS as a key part of tax compliance, so any lapses, whether intentional or accidental, can attract penalties, interest charges, or disallowance of expenses. Understanding these consequences helps businesses and professionals stay compliant and avoid unnecessary liabilities.

Non-compliance under Section 194J TDS provision can lead to serious repercussions for businesses and individuals alike, including:

One of the primary consequences of failing to deduct or pay TDS late is the disallowance of expenses. When an individual or entity claims a business expense requiring a TDS deduction, the failure to deduct TDS will result in a 30% disallowance. This deduction is of the expenditure for the year the expense is claimed for.

However, once the TDS is deducted and paid to the government, the disallowed amount will be reallowed in the year the tax is deposited. This ensures that while the expense is temporarily disallowed, the taxpayer can recover it once compliance is met.

Interest is another significant consequence of non-compliance, and it can be levied in two scenarios:

Failure to Deduct TDS: If TDS is not deducted when required, interest is charged at 1% per month (or part of the month) from the due date of deduction until the actual date of deduction.

Failure to Pay or Deposit TDS: If TDS is deducted but not deposited with the government on time, the interest rate increases to 1.5% per month (or part of the month) from the date the tax was deducted until the date the payment is made to the government.

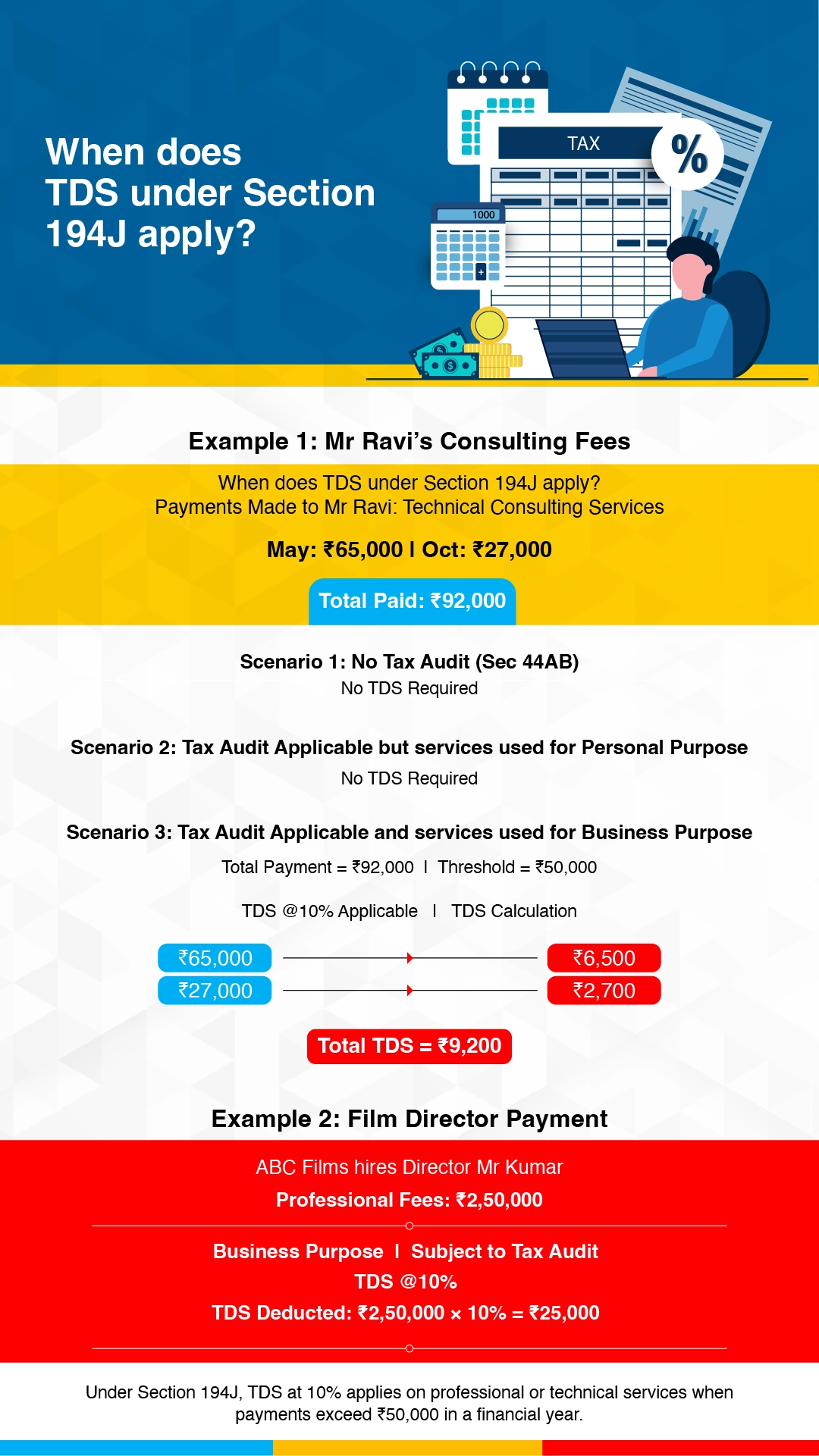

Example 1: Mr Ravi Consulting Fees for Technical Services

Mr Ravi is a freelance consultant who provides technical services to Mr Suraj, who owns a software company. In the Financial Year (FY) 2025-26, Mr Ravi received two payments for his services: the first payment of ₹65,000 in May and the second payment of ₹27,000 in October.

Let's analyse Mr Suraj’s TDS liability in three scenarios:

Scenario 1: Mr Suraj is not liable for audit u/s 44AB.

Since Mr Suraj is not liable for a tax audit under Section 44AB, there is no requirement to deduct TDS on these payments, regardless of the amount.

Scenario 2: Mr Suraj is liable for audit u/s 44AB, and the services were for personal purposes.

Even though Mr Suraj is liable for a tax audit, the services provided by Mr Ravi were for personal purposes. Therefore, no TDS is required to be deducted from these payments.

Scenario 3: Mr Suraj is liable for audit u/s 44AB, and the services were for business purposes.

Since Mr Suraj is subject to a tax audit, and the services were used for business, total payments (₹92,000) exceed the ₹50,000 threshold.

TDS at 10% must be deducted from the entire amount paid during the year.

TDS calculation:

On ₹65,000, the TDS will be ₹6,500

On ₹27,000, the TDS will be ₹2,700

Example 2: A Film Production Company Hiring a Director

ABC Films is a film production company that hires the renowned director, Mr Kumar, for a project. The director is paid ₹2,50,000 for his services during the production. Since this is a professional service under Section 194J for which the remuneration is more than ₹50,000, TDS must be deducted.

Scenario: ABC Films is liable for tax audit u/s 44AB.

As the services are professional services for business purposes, ABC Films will deduct TDS at 10% on ₹2,50,000, which amounts to ₹25,000. This amount will be deducted and remitted to the government.

In this case, the film production company must comply with TDS provisions, ensuring that the deduction is made on time and the tax is paid to the authorities.

A vital component of the Income Tax Act's regulation of professional service taxation is the Tax Deducted at Source (TDS) method found in Section 194J of the Income Tax Act. Stakeholders can fulfil their tax obligations and support an open and accountable financial environment by being aware of the subtleties of Section 194J. A tax-compliant and financially stable corporate climate is fostered by keeping informed and seeking professional assistance, even as the regulatory environment changes.

Section 194J requires TDS on payments for professional, technical, managerial, consultancy services, royalty, and non-compete fees made to resident service providers when payments exceed the specified threshold.

Tax must be deducted only when total professional or technical service payments to a person exceed ₹30,000 in a financial year. This limit applies per payee per year, not per individual payment. From the financial year 2025-26 onwards, the threshold has been increased to ₹50,000.

From April 2025, TDS under Section 194J applies only when total payments to a resident service provider exceed ₹50,000 in a financial year, helping reduce unnecessary deductions for small payments.

TDS under Section 194J must be deducted at whichever point occurs earlier, either when the expense is credited to the service provider’s account or when the actual payment is made.

If the payee's gross net income for the year is less than the taxable income and the TDS is excluded under section 194J, the payee may request a refund of the TDS by filing an income tax return.

Form ITR 4. You can file ITR Form 4 if the 194J receipt is less than ₹50 lakh; otherwise, you should file ITR 3.

If the payee does not furnish a permanent account number, TDS must be deducted at 20%, which is significantly higher than normal rates and can reduce the payee’s actual receipt.

TDS is 2% for technical services and certain royalty payments, 10% for other professional services, and 20% whenever the payee fails to furnish a valid permanent account number.

Advocate fees have a 10% TDS rate, subtracted at the time of payment. If the fees paid to the advocate exceed ₹30,000 in a financial year, TDS is applicable, regardless of whether the advocate is an individual or a Hindu Undivided Family (HUF).

Yes, if you have had excess TDS withheld from your income, you can receive your TDS refund without filing an ITR.

You can claim Section 194J TDS by checking the deducted amount in your Form 26AS or AIS and reporting it in your income tax return to adjust your final tax liability accurately.

To reflect 194J income in your Income Tax Return (ITR), you need to report it under the "Income from Other Sources" section, specifying the payer's details, nature of payment, and the amount received, ensuring compliance with relevant tax regulations.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.