- Riders: Add-on benefits you can include in your insurance plan to increase coverage

- Corporate Bonds: Company-issued debt securities that offer fixed interest returns

- NAV: Net Asset Value is the price of one unit of a fund, based on total assets minus liabilities

- Lock-in Period: The minimum time your investment must remain before withdrawal is allowed

- Equity: Investment in company shares with higher growth potential and higher risk

Choosing an investment product can feel challenging when you need to balance financial protection, long-term goals, and changing market conditions. Some products focus only on growth without offering security, while others provide protection but limited wealth-building potential. This is where understanding ULIP plans becomes valuable.

In this guide, we will walk through what a ULIP is, the different types available, how it works, and how to select the right one based on your needs.

Key Takeaways

|

What is a ULIP Plan?

A ULIP (Unit Linked Insurance Plan) is an insurance product that offers you a dual benefit of life cover and investment to achieve long-term wealth creation. The premium paid for this plan is divided into two parts: one part of the premium goes towards life cover, and the remaining sum is invested in the fund of your choice. In ULIP plans, you can invest your money in equity, debt, or both as per your risk appetite. The ROI depends upon the performance of funds.

Investment Calculator

Our investment calculator can easily help you plan the needed financial corpus for your goals.

1

My Goal

2

Investment Amount

3

Additional Details

4

Our Recommendation

My Goal

Investment Amount

Additional Details

Our Recommendation

Corpus Created in {corpusYear} year

you Invest {investAmount} over {totalYear} Years

0 year

₹ 1.20Lakh

1 year

₹ 1.20Lakh

2 year

₹ 1.20Lakh

8 year

₹ 1.20Lakh

9 year

₹ 1.20Lakh

10 year

₹ 1.20Lakh

Hi {name}, We recommend to start investing

Disclaimer-

The above calculation and illustration of figures are indicative only and not on actual basis.

What are the Different Types of ULIPs?

Let's understand the top 10 types of ULIP plans based on funds and structure:

- Based on Funds: ULIPs give you the flexibility to choose how your premium is invested. Each fund type carries a different balance of risk and return. You can switch between funds as your financial goals or market conditions change.

- Equity Funds: Equity funds invest mainly in stocks. They aim for higher growth over time and are suitable for long-term investors who can handle market fluctuations. These funds carry higher risk, but they offer the potential for better returns if you stay invested for several years.

- Debt Funds: Debt funds invest in bonds, government securities, and fixed-income instruments. The focus is on stability and predictable returns rather than high growth. They suit investors who prefer lower risk and want to protect their capital while earning steady returns over the policy term.

- Balanced (Hybrid) Funds: Balanced funds split the investment between equity and debt. The equity portion contributes to growth, while the debt portion provides stability. These funds are suitable for moderate risk takers who want a blend of potential returns with controlled volatility in market fluctuations.

- Liquid Funds: Liquid funds invest in short-term money market instruments such as treasury bills and certificates of deposit. These funds are suitable for managing short-term financial needs or parking surplus money without locking it away.

- Based on Their Structure: The structure of a ULIP influences how the policy manages investment and life cover benefits. Different structures cater to various life goals, including wealth creation, retirement planning, and child education.

- Traditional ULIP: Traditional ULIP prioritise life insurance protection and offer limited fund choices. They provide stable, low-risk returns over time. These plans are suitable for individuals who prefer simplicity and want guaranteed coverage along with a conservative approach to investment growth.

- Market-Linked ULIP: Market-linked ULIPs invest mainly in equity and market-driven funds. Returns vary based on market performance, offering higher growth potential along with higher risks. These plans are best suited for investors with a long-term horizon and the ability to withstand fluctuating market conditions.

- Pension (Retirement) ULIP: Pension ULIPs help you build a retirement corpus over time. The plan focuses on long-term savings, often allowing regular contributions throughout your working years. At retirement, the accumulated amount can provide income security and support your lifestyle needs after you stop working.

- Child ULIP: A child ULIP plan is designed to secure your child’s financial future, especially for education or major life milestones. They offer market-linked growth with life cover. Even if something happens to the parent, the plan continues, ensuring the child’s goals remain financially supported.

Get a Personalised ULIP Plan for Wealth Creation & Protection

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Features of ULIP Plans

ULIP is designed to combine insurance protection with investment growth, making it a flexible financial tool for different life stages.

Some key features of a ULIP plan include:

- Flexible Fund Choices: ULIPs allow you to invest based on your risk comfort. If you prefer steady and low-risk growth, debt funds work well. If you seek higher returns and are comfortable with market fluctuations, equity funds are a suitable option. You can also switch between funds as your goals change.

- Lock-In Period: ULIP come with a five-year lock-in period, encouraging disciplined savings. Staying invested for longer generally improves your chances of earning better returns. It is suitable for long-term financial goals.

- Flexible Premium Payment Options: You can choose how to pay your premiums:

- Single Pay: one lump sum at the start

- Limited Pay: pay for a few years while coverage continues longer

- Regular Pay: pay throughout the policy term

This flexibility helps you match the plan with your financial capacity

- Partial Withdrawals: This offers liquidity once the five-year lock-in ends. You can make partial withdrawals for needs like emergencies or planned expenses. This helps you access funds when necessary while keeping the rest of your investment growing.

How Does a ULIP Plan Work?

Understanding how a ULIP works becomes easier when you follow the complete roadmap from purchase to payout.

Here is a simple breakdown:

Choose Your Policy: Start by selecting a ULIP based on your financial goals, risk appetite, and investment horizon.

Pay the Premium: You pay regular or one-time premiums. A part goes towards life insurance cover, and the rest is invested in market-linked funds.

Fund Allocation: Choose between equity, debt, or balanced funds. You may switch funds anytime based on market conditions or changing goals.

Track Your Growth: The value of your policy varies as per the performance of the chosen funds. Your statement will reflect units purchased and the current NAV.

Maturity or Claim: If you survive the policy term, you receive the fund value as a maturity benefit. In case of an unfortunate event, your nominee gets the life cover amount.

Who Should Consider Buying a ULIP Plan?

A ULIP plan is suitable for individuals who want to grow their wealth while ensuring life protection under one policy. It is especially helpful for:

Young professionals who want to start early and benefit from long-term market growth

Single or primary earners who want life cover along with disciplined investment planning

Individuals with long-term goals such as children's education, marriage, or buying a house

Self-employed individuals or entrepreneurs seeking both financial protection and wealth-building options without relying on employer benefits

Salaried individuals in urban and semi-urban regions who want market-linked growth with the flexibility to switch funds when required

Did You Know?

In FY25, ULIPs contributed approximately 42% to certain insurers’ portfolios, indicating robust demand and a large market share

Source: Money Control

How to Choose the Right ULIP Plan?

Below are some steps that can help you select the best ULIP for your needs:

- Determine your Financial Objectives: It is important to clearly define your financial goals, such as wealth creation, retirement planning, home ownership and more. This can help you align the ULIP to your goals effectively.

- Evaluate your Risk Appetite: ULIPs offer a range of funds, including equity, debt and balanced funds. Your choice of funds will depend on your risk appetite. For instance, equity funds are considered high-risk investments, whereas debt funds are considered low-risk investments. Balanced funds strike a balance between the two.

You must assess your risk tolerance for investments and choose a ULIP that matches your comfort level. - Compare Fees and Charges: ULIP have premium allocation, fund management and policy administration charges. These fees can vary from plan to plan. Therefore, it is necessary to thoroughly understand and compare the various fees associated with these plans and select the most cost-effective one.

- Check Fund Options: ULIPs offer a diverse range of investment funds to cater to different investment goals and risk appetites. Equity funds allocate most of their portfolio to stocks. In contrast, debt funds primarily invest in fixed-income assets like government and corporate bonds, along with money market instruments. Lastly, hybrid funds invest in a mix of equities and debt instruments to provide a balanced approach to risk and return.

You need to evaluate different investment funds to build a well-diversified ULIP portfolio tailored to your needs. - Compare Lock-in Period: ULIPs have a lock-in period of five years. During this duration, your investment remains locked, and you cannot make partial withdrawals. You must carefully understand the terms and conditions of the plan, particularly regarding the lock-in period, and evaluate your liquidity needs to avoid any hassles later.

- Carefully Read Policy Documents: It is essential to review the policy documents, including terms, conditions, features, exclusions, inclusions, benefits, and more, to gain a comprehensive understanding of the plan. The best ULIP investment plan offers transparency, ensuring you understand how the plan works and can make well-informed decisions.

- Compare Fund Performance: Along with the choice of funds, you must also analyse the performance of the funds within the ULIP. This allows you to understand their return rate and confirm if they align with your investment objectives.

- Check Out the Tax Benefits: Investing in ULIP offers tax benefits. You can claim a deduction on your ULIP premiums of up to ₹ 1.5 lakh per annum, subject to conditions prescribed under Section 80C of the Income Tax Act, 1961. Additionally, the maturity benefit is exempted subject to conditions prescribed under Section 10(10D)* of The Income Tax Act, 1961, which further maximises your tax efficiency.

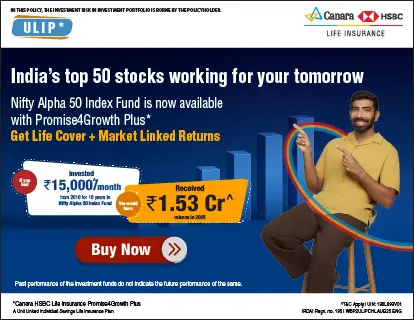

Unit Linked Insurance Plans - Top Selling Plans

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.

Wealth Today, Protection Always

Promise4Growth Plus

- Life Cover up to 100 Years

- 13 Fund Options

- Fund Switching Option

- Waiver Of Premium

Secure Your Future with Confidence

SecureInvest

- Life Cover up to 100× Annual Premium

- 12 Fund Choices

- Automated Portfolio Strategies

- Maturity Booster

Invest Smart, Live Smart

Wealth Edge:

- Flexible Premium Options

- Multiple Fund Allocations

- Systematic Withdrawals

- Premium Waiver Benefit

Why Canara HSBC Life Insurance?

Choosing the right ULIP plan becomes easier when you have a provider you can trust. Here’s what makes Canara HSBC Life Insurance a reliable choice:

Strong and Trusted Background: The company is backed by established financial institutions, offering stability, credibility, and confidence in long-term investment and protection.

Consistent Claim Support: A strong track record of transparent and timely claim settlements ensures your loved ones receive the benefits without stress or delays. We offer a claim settlement ratio of 99.52%.

Wide Choice of ULIP Plans: Whether your goal is wealth creation, child education planning, or retirement readiness, you can find a ULIP option suited to different financial journeys. We offer various ULIP plans, including the Promise4Growth Plan, Secure Invest Plan, and Wealth Edge Plan, to help you grow, protect, and future-proof your wealth.

Flexibility to Personalise Your Plan: You can choose fund options, switch between equity and debt funds, add riders, and select premium payment modes, making the plan adaptable to your needs.

Seamless Digital Experience: From comparing plans to managing investments, the entire process is simple, accessible, and easy to manage online.

Final Thoughts

Choosing the right ULIP plan is ultimately about striking the right balance between wealth creation and financial security. Whether you seek disciplined long-term savings, market-linked growth, or flexible fund switching options, ULIPs provide a structured approach to building your financial future. Start early, stay invested, and review your fund strategy regularly to maximise your returns and meet your long-term goals confidently.

Establish a dependable financial safety net that safeguards your family's future.

Glossary

FAQs

Your premium is invested in market-linked funds. The value of your plan grows based on the performance of these funds over time.

Yes. Premiums paid may qualify for tax benefits under Section 80C, and maturity benefits may also be tax-efficient as per prevailing tax laws.

Partial withdrawals are allowed after the 5-year lock-in period, making it useful for long-term financial planning.

Yes, especially for those who want guided investing with flexibility. You can start with balanced funds and switch later if needed.

If premiums are not paid during the lock-in period, the policy shifts to a discontinuance fund. You can revive it within the allowed revival period.

How to Choose ULIP Funds: Types, Risk Profile & Strategy

22 July '26

291 Views

7 minute read

Know how to choose ULIP funds based on risk profile, fund types & investment goals for better returns.

Read More

Ulip

Is ULIP a Good Investment for Short-Term Gains?

09 July '26

2201 Views

7 minute read

Discover whether ULIPs are suitable for short-term investment goals and understand the risks, returns and lock-in period.

Read More

Ulip

When Is the Right Time to Invest in ULIPs?

29 June '26

896 Views

8 minute read

When is the right time to invest in ULIP? Learn how timing, goals, and market conditions impact returns and why starting early can maximise long-term benefits.

Read More

Ulip

How Do Top-Ups Work in ULIPs? Benefits & Key Considerations

29 June '26

899 Views

6 minute read

What is a top-up premium in ULIP? Learn how ULIP top-ups work, their benefits, and how additional investments can help boost long-term returns.

Read More

Ulip

Professional vs. Retail Investors: How Do They Structure Their Portfolios Differently?

29 June '26

134 Views

4 minute read

Discover how retail and professional investors differ in strategy, risk, and portfolio structure. Learn which approach suits your investment goals.

Read More

Ulip

ULIP Tax Benefits Explained: Save Tax Under 80C

29 June '26

2768 Views

10 minute read

Find out why ULIPs are an excellent way to save money on taxes. Gain tax advantages, market-linked returns, and life insurance while accumulating long-term wealth.

Read More

Ulip

Best Retirement Plan at 30s & 40s: How to Start Early

29 June '26

2761 Views

10 minute read

Learn how to plan for retirement at 30 or 40. Explore the best retirement plans, investment strategies, and tips to secure long-term financial stability.

Read More

Ulip

ULIP Structure Explained: Funds, Charges & How It Works

29 June '26

2771 Views

10 minute read

Comprehend the structure of a ULIP. Find out about charges, fund options, life insurance, premium allocation, and how ULIPs integrate investment and insurance.

Read More

Ulip

GST on ULIP: Rates, Charges & Impact on Premiums

29 June '26

3681 Views

7 minute read

Understand how GST applies to ULIP charges, premiums, and withdrawals. Simple explanation for policyholders to know what they pay and why it matters.

Read More

Ulip

Popular Search

- What is ULIP?

- ULIP Tax Benefit

- ULIP Full Form

- ULIP Vs Term Insurance

- Best ULIP Plans

- Best ULIP Plan For Child

- Allocation Charges In ULIP

- ULIP Returns In 15 Years

- Difference Between ULIP and Mutual Fund

- ULIP Vs SIP

- Mortality Charges In ULIP

- What is NAV?

- How ULIP Works?

- Tips to Buy ULIPs

- ULIP Calculator

- Power of Compounding Calculator

- ULIP Tax Benefits in India