Written by : Knowledge Centre Team

2026-07-28

8348 Views

17 minutes read

Share

Planning for your future often involves a mix of life goals like buying a house, getting married, ensuring a great future for your child and visiting a new country. These are the "life goals" or milestones you strive to achieve.

While these goals require focused financial planning, one smart way to make the most of your money is to invest in tax-saving instruments that help you reduce your liability while growing your wealth. Tax-saving investments are not a life goal, but they can help you reduce taxes, which can help you save more for your goals.

These are the investments that are eligible for deductions u/s 80C of the Income Tax Act 1961. ULIPs and Equity-Linked Saving Schemes (ELSS) are some of the most popular tax-saving options available in the market. But which one should you choose?

Let’s break it down to help you decide.

Key Takeaways

|

An Equity Linked Saving Scheme, or simply ELSS, is a type of mutual fund that invests a major proportion of the funds in equity and related schemes. ELSS has at least 80% of the fund invested in equity-related securities, while some of the contributions are in fixed investments.

This is the only type of mutual fund that is eligible for deductions u/s 80C. ELSS has a short lock-in period of just 3 years. Since the equity contribution is very high, it is a more risky investment, but at the same time it has the potential to earn you great returns and help fulfil your goals.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

You can invest in ELSS if your risk appetite is high enough, i.e., you can tolerate an investment with high volatility and have a goal that has a timeline of 3 or more years. Thus, you can look to achieve your medium-term goal with your ELSS.

These can be the following:

The longer you hold your ELSS scheme, the better are the chances of you getting higher returns.

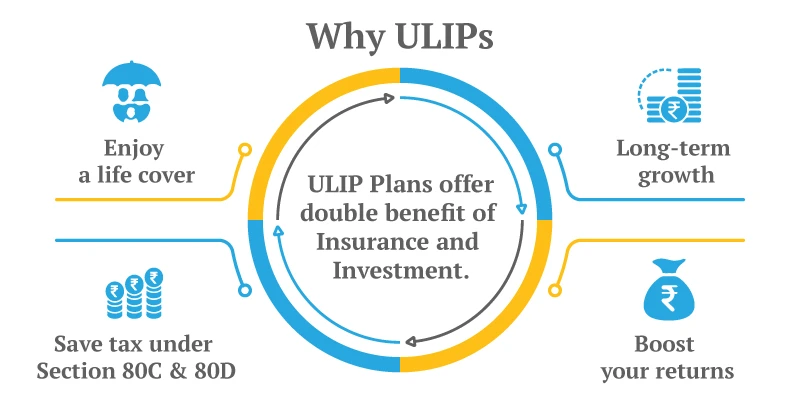

A Unit Linked Insurance Plan is a life insurance variant that also offers you an opportunity to invest in the market. With ULIP plans, you get both insurance and investment in a single product. It offers tax benefits under Section 80C for premium payments and Section 10(10D) for maturity/death benefits on fulfilment of certain conditions.

ULIPs have a lock-in period of 5 years. During this period you cannot make any withdrawals, and if you do, you will lose a lot of money.

The ULIP plan is perfect to cater to your long-term goals, which have a timeline of at least 5-10 years or more. The longer you stay in ULIP, the more time you will allow your investments to grow and help you create a good corpus.

ULIP plans can help you achieve the following goals:-

We have now seen that both these investment options have some similarities. These can both help you save taxes and are linked with the market. But despite these points, they also have a lot of differences.

Let us look at the difference between ELSS and ULIP with the help of a table:

Features | ELSS | ULIP |

Investment Portfolio | An ELSS fund has a minimum of 65% of equity stocks. Generally, ELSS funds have 80-85% of equity, | In a ULIP, you are given full freedom to decide how much of your money will be invested and in which fund. Thus, you can choose to invest in the following equity and debt as per your preference:

|

Lock-In Period | ELSS have a lockin period of 3 years | ULIP plans have a lockin period of 5 years |

Tax savings | ELSS is eligible for deduction of up to ₹1.5 lakhs u/s 80C | Tax deductions of up to ₹1.5 lakhs u/s 80C available. Tax-exemption also available on maturity/death amount u/s 10(10)D |

Tax on Maturity/ Withdrawals | LTCG tax @ 10% if the gains exceed ₹1 lakh. | Returns can be taxable if the premium you pay exceeds ₹ 2.5 lakhs per year. |

Charges | ELSS funds involve charges such as exit-load, management charges. | ULIPs involve charges such as:

|

Expense Ratio | It has a low expense ratio in the range of 0.5% to 1.5% | Charges are capped at 1.35% |

Life Cover | No life cover is present | Life cover is provided in ULIPs. The death benefit is payable to the family at the time of your death |

Bonuses | Not present | Bonuses present in certain policies such as:

|

Flexibility in Investment | You can either invest in a lump sum or through SIP | Freedom to choose your mode of premium payment and the duration |

Withdrawals | After 3 years | After 5 years |

Switching | Not allowed | Fund switching is allowed |

Choose ELSS if you:

Are looking for a high-return, market-linked tax-saving investment

Have short- to medium-term financial goals

Want the shortest lock-in among 80C instruments

Choose ULIP if you:

Want investment + insurance in one product

Are building a long-term retirement or child education corpus

Seek tax-free maturity proceeds with flexible fund management

Both ULIPs and ELSS have their sets of advantages and shortcomings. They can help you at different times. This is a great option if you are willing to take risks and want to save taxes. ELSS are more transparent and involve fewer expenses. Thus ELSS can be considered if you want an out-an-out investment option that can help in achieving shortly to medium-term objectives

ULIPs on the other hand offer tax-benefit, both in premium payment as well as maturity/death benefit. It includes a life cover that ensures your family remains financially protected even after you are not with them.

When choosing a long-term financial product like a ULIP, the reliability and track record of the insurance provider matter just as much as the product itself. Canara HSBC Life Insurance is one such trusted name that offers numerous life insurance, savings and investment plans. Our ULIP plans with features like multiple fund options, flexible premium payments, partial withdrawals, and transparent charges, empowers policyholders to grow their wealth while enjoying life cover and tax benefits.

So, whether you opt for ELSS, ULIP, or a strategic mix of both, the secret lies in starting early, investing consistently, and aligning your choices with your life goals.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.