Written by : Knowledge Centre Team

2025-11-13

1885 Views

6 minutes read

Share

Do you want to be wealthy? Obviously, who doesn’t? But it only makes sense if your wealth multiplies only stay in the family. In fact, the question most people long to ask is how to ensure that? While it may seem a far off priority to pass on sufficient wealth onto your children, Unit-linked Insurance Plans can help.

So, if you have a wealth goal, it’s not a destination you want to visit as a tourist, but as a resident. A lot of the wisdom is already there in traditional methods of saving, spending only on important needs, etc. Following this wisdom in modern times, however, will be a challenge.

But if you set your goal right, priorities will start to fall in order. Wealth goals are like that once you set your sights on it and create a practical and realistic plan for it. With a wealth goal, you have two objectives - Generate wealth and Preserve the wealth.

Both objectives need a slightly different approach. While generating wealth is a high-involvement activity, preservation should ideally be passive. Meaning, while you put a lot of effort into generating wealth, preservation should be almost automatic.

This is where wealth insurance plan comes into the picture.

The word ‘insurance’ signifies preservation, and preservation ultimately leads to long-term prosperity or presence of wealth in the family. More specifically, wealth insurance will mean the safety of wealth from all of the following:

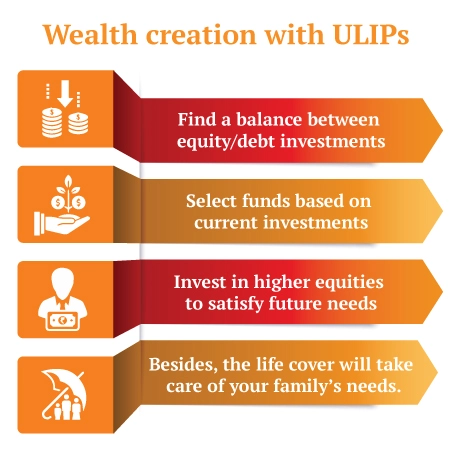

Unit linked insurance plans are unique and versatile investment option from life insurance companies. ULIPs provide you with dual benefits of wealth generation and preservation, due to their unique combination of insurance and investment options.

A ULIP investment plan can offer you all the options we have listed for wealth preservation. In fact, ULIP can fulfil both wealth generation and preservation goals for you.

ULIPs give you a tax-efficient avenue for investing in equity markets and ways to automate your portfolio management. Here are a few unique investment options which help you generate wealth and preserve it:

With ULIP plan you can secure the premiums as well, which the insurer will fulfil in case of your early demise. The investments will continue as you planned even after your demise and your family will receive the accumulated money at the time of maturity.

Canara HSBC Life’s Promise4Growth Plus plan can cover your premiums in case of your death within the policy tenure. For example, if you committed to investing Rs. 2 lakhs a year for 30 years in the Promise4Growth Plus plan, and unfortunate pass away in the 15th year of the policy:

Thus, a ULIP plan like Promise4Growth Plus can fulfil all five of your wealth generation and preservation needs. The best part is that you can fulfil both objectives of your wealth goal without a continuous involvement in the plan.

Once you automate the investment and portfolio management you can simply focus on your family and profession. The plan will work in the background to generate returns and preserve them as per the decided strategy.

The money you invest in ULIPs helps you save tax under section 80C of the Income Tax Act. Any withdrawals and maturity proceeds from ULIPs are also exempt from tax. However, you will need to ensure that you don’t invest more than 10% of the life cover in a year.

For example, if your life cover in the ULIP is Rs. 30 lakh, you should not invest more than Rs. 300,000 in any policy year. If you do the additional investment will become taxable at the time of maturity.

When it comes to wealth generation nothing is more important than time. It is the only factor you can control in the investment equation. Time compounds your wealth, the more time your money gets in the investment the more it compounds.

So, make sure to give your wealth goal as much time as possible unhindered for the best results.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.