Written by : Knowledge Centre Team

2026-06-23

1894 Views

8 minutes read

Share

When you think of investments and savings, you start exploring various plans that offer you various benefits for saving your money. Some of the best savings and investment options include life insurance plans. However, as you go deeper with your financial research, you might get confused between ULIPs (Unit Linked Insurance Plans) and the SIP (Systematic Investment Plans).

Also Read - What is SIP?

If you are someone who has not heard of these terms yet, then don't worry. We will discuss the difference between the two, covering the very basics to make it easier for you. With this knowledge, a new investor and someone who has done basic research about financial investments can find themselves at ease.

Now, first things first, let's take a look at what exactly ULIP and SIP mean.

Key Takeaways

|

Unit Linked Insurance Plans, or ULIPs, are financial investment tools that provide the benefits of both insurance and investment when you invest in them. While providing you with a cover with the insurance plan, it allows you to invest in bonds and stocks.

This way, returns from ULIPs are market-linked with the security of an insurance cover. Apart from wealth creation, you can develop an investment discipline with ULIPs. ULIPs are a good option for long-term financial goals.

Also Read - What is ULIP?

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

A Systematic Investment Plan or SIP is a systematic way to channelise your investment. Through SIP, you invest on a monthly, quarterly, or yearly basis in mutual funds. It is a long-term investment tool with a planned approach. You can have wealth creation over a certain period.

With SIP, you should have a long-term financial or life goal for which you can plan the savings. The benefit of SIP is that you can start your investment with as low as ₹ 500. So, even if you are a student or someone who has just started earning, SIP is an option.

Having discussed the basics of both ULIP and SIP, it is time to take a look at their differences.

Parameter | ULIP | SIP |

Policy Type | Benefits of both life insurance and investment | Only investment benefits |

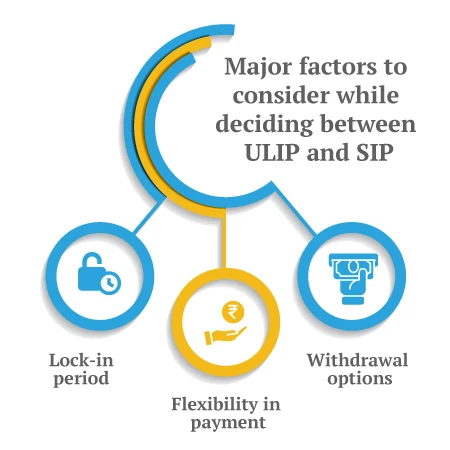

Lock-in Period | 5 Years | 3 Years (for Equity Linked Savings Scheme (ELSS) mutual fund) |

Tax Benefits | Tax-related benefits can be availed on the premium paid towards the policy and maturity proceeds under Section 80C and 10(10D) of the Income Tax Act | Tax benefits are not applicable in SIP, however, exemptions are applicable only on the Equity Linked Savings Scheme (ELSS) up to the maximum limit of ₹.1.5 lakh |

Withdrawal Options | Partial withdrawals after the lock-in period are over | Invested capital can be withdrawn; however, for ELSS, withdrawals can be made after a lock-in period of 3 years |

Flexibility | Flexibility in terms of deciding what portion would go for life insurance cover and what would go for investment | Flexibility in terms of increasing or decreasing the invested capital for long-term gain |

Additional Benefits | Loyalty benefits, along with the issuance of additional fund units after the completion of the lock-in period | There are no such additional benefits |

Death Benefits | Benefits are paid to the beneficiary in case of the unfortunate demise of the insured person | No death benefits are available |

Fund Management Charges | 1.35% | 2.50% |

Switching Option | Free switching options between funds (up to a limited number) in a year | Freedom to make switches between the funds |

Regulator | IRDAI | SEBI |

Choosing between ULIP and SIP might be confusing..If you have a long-term financial goal where you need a planned approach, then SIP comes with a logical option. However, if you are also looking for an insurance cover alongside your investment, then ULIPs are the best option. Before making a call between the two, you must check the parameters based on which we made the comparison above.

The importance of each feature varies from person to person. Some investors may prioritise switching options or lock-in period, whereas others may focus more on death benefits or additional advantages.

After looking at the comparison between SIP and ULIP, the next logical step is to determine which one to invest in. Simply, the choice depends on your financial goals and plans. However, taking a look technically and in terms of financial management, ULIPs are a nice option.. You get a life insurance cover as a first thing. Further, there is an option to earn market-linked returns. With SIP, you don't get dual benefits.

Thus, with ULIPs, you don't have to buy two financial products separately for insurance and investment. However, if you are not thinking of insurance much and flexible with buying two separate financial products, then SIP is also a good option. Another benefit of SIP is that it's a new investor's go-to tool, as you can start with a bare minimum amount as well.

There are several ULIPs offered by Canara HSBC Life Insurance. You can consider the following:

You can consider the Promise4Growth Plan by Canara HSBC Life Insurance. It is a smart ULIP that blends life cover with the flexibility of market-linked investments. It offers three plan variants: Promise4Wealth, Promise4Care, and Promise4Life, to match your financial goals and life stage. You can choose your premium term, policy duration, and fund allocation from a pool of nine funds, including a mid-cap growth index fund. The plan ensures flexibility in investment and coverage, with features like return of mortality charges and low fees.

Both ULIP and SIP serve unique financial purposes. If you're looking for a dual benefit of life insurance and market-linked returns, ULIPs like Promise4Growth, or Alpha Wealth by Canara HSBC Life Insurance, offer flexibility, long-term value, and protection. On the other hand, if you're focused purely on investment with a small start, SIPs are beginner-friendly. Your decision should align with your financial goals, risk appetite, and need for insurance cover alongside investment growth.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.