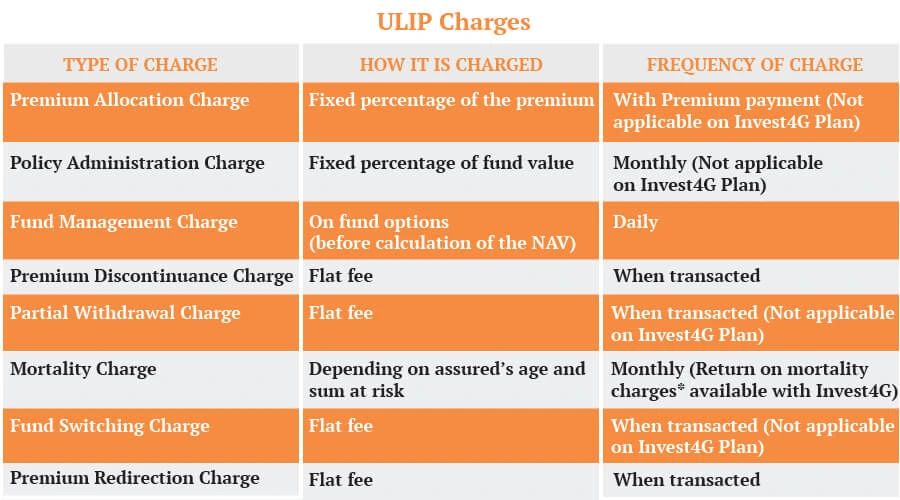

- Premium Allocation Charge: A charge deducted from the premium before the remaining amount is invested in ULIP funds

- Fund Management Charge: A fee charged by the insurer for managing the investment funds in a ULIP

- Mortality Charge: The charge deducted to provide life insurance coverage under a ULIP

- Partial Withdrawal: Withdrawal of a portion of the ULIP fund value after the applicable lock-in period, subject to policy terms

- Net Asset Value (NAV): The per-unit value of a ULIP fund after deducting applicable fund management charges

Written by : Knowledge Centre Team

2026-07-30

1023 Views

6 minutes read

Share