Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Key Takeaways

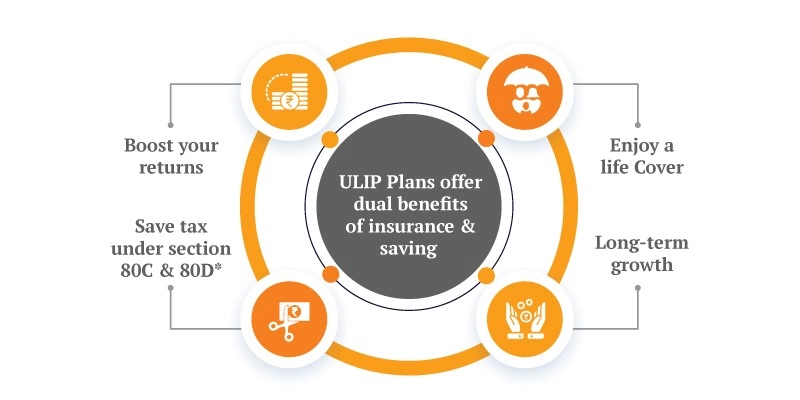

A Unit Linked Insurance Plan (ULIP) offers both insurance and investment benefits

Investing in a ULIP online provides greater flexibility, transparency, and tax benefits under Section 80C and Section 10(10D)

ULIPs are ideal for long-term wealth creation with tax benefits

ULIPs allow fund switching, enabling investors to adapt to market conditions

Depending on their own needs, investors can choose the proportions of the instrument they want to invest in

Unit Linked Insurance Plans (ULIPs) are popular investment instruments for individuals looking to secure their and their family’s future in every way possible. Starting from acting as an insurance cover for the policyholder to providing substantial returns as an investment instrument, ULIP benefits make it the ideal solution to a whole range of financial problems.

The advantages of ULIP stem from the flexibility it offers investors. Additionally, ULIP tax benefits propel its popularity, with individuals looking to save on taxes and create a larger corpus to meet their future goals, both in the long term and in the short term. Canara HSBC Life Insurance offers enormous flexibility to customers through customizable plans that allow them to opt for benefits most suited to their requirements.

Get a Personalised ULIP Plan for Wealth Creation & Protection

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Read on to learn more about the advantages of ULIPs:

Death Benefit: One primary perk of opting for a ULIP is the death benefit that is accessible to dependents upon death ofthe policyholder. The death benefit ensures that the policyholder’s dependents have access to financial security and can sustain their regular lifestyle, even in the absence of the policyholder.

Meeting Financial Goals: Both short-term and long-term financial goals require the setting up of a corpus. With a ULIP, policyholders can aim to grow their corpus substantially and meet these goals. For instance, with education costs rising by the day, a ULIP can be set up to start building a corpus to meet the child’s higher education goals, even when the child is very young. ULIP benefits can also extend to saving up for short-term goals such as taking a family vacation to an exotic location far away.

Income Tax Benefits: Income tax benefits are a consideration while opting for investment instruments, and ULIP tax benefits make it the foremost choice for such investors. Under the Income Tax Act, both Section 80C and Section 10(10D) offer tax benefits on ULIPs. ULIP tax benefits come into play when individuals pay premiums, when returns are withdrawn from the fund, and when the fund matures.

Flexibility: Investment and insurance are two financial pillars for all individuals looking to protect their financial health and ensure long term financial success. As a result, ULIPs serve as the perfect instrument for such persons. While investing in ULIPs, a portion of the premium paid goes towards ensuring the insurance cover while the rest is invested into investment instruments. ULIPs guarantee flexibility by letting policyholders decide how much of the investment should go towards insuring themselves and how much of it should go towards building their corpus. Additionally, investors can decide the proportions of the instrument they choose to invest in based on their individual requirements. For instance, those looking for low-risk instruments can choose to invest a higher amount towards debt or government securities that do not pose much risk. On the other hand, investors looking for higher returns can choose to invest in market instruments such as equities, which offer significantly higher returns but are also influenced by market forces. Instruments dependent on market forces are affected by factors such as political or economic instability and a range of other causes. With a ULIP, investors can easily switch between funds based on existing market conditions and their own predetermined goals.

Inculcates the Habit of Savings: By investing in a ULIP, individuals can inculcate the disciplined habit of saving regularly, which can prove hugely beneficial over the course of their lives. Saving regularly ensures that there is always financial capital to fall back upon, especially during times of financial emergencies.

Did You Know?

Any profits and gains from the redemption of ULIPs that are not excluded under section 10(D) will, therefore, be subject to capital gains tax.

Source: ET

When Should You Invest in a ULIP?

Investment in a ULIP at the right time can significantly impact your financial growth and security. Whether you are starting your career, planning a family, or planning retirement, ULIPs can match your long-term objectives.

Ideal Time Frame for Maximum Returns:

ULIPs are best for long-term investments. A duration of 10-15 years makes your money grow and compound consistently, overcoming short-term market volatilities. The sooner you begin, the more chances your wealth will grow. Also, ULIPs provide a facility for fund-switching, whereby you can adjust your investment pattern according to market conditions and investment objectives. ULIPs work best as a long-term investment (10-15 years), allowing your money to grow steadily while minimising market volatility risks.

ULIPs for Different Life Stages (Young Professionals, Parents, Retirees)

One of the key benefits of ULIPs is that they provide flexible investment plans to suit various phases of life. If you are a young professional, a family man, or a pre-retirement planner, ULIPs can secure your future and give you insurance coverage.

Young Professionals:

Wealth creation at a younger age through high-growth equity fund investments.

Take advantage of longer compounding periods to maximise returns.

Enjoy tax-saving benefits while planning for long-term goals like buying a house or starting a business.

Parents:

Secure your child's future with a balanced ULIP investment, securing a combination of growth and stability.

Utilise ULIPs for planning educational costs, wedding expenses, and other milestones.

Life cover ensures financial security for your family members, even during unexpected situations.

Retirees:

Choose low-risk debt funds for guaranteed fixed and stable returns.

Utilise ULIPs as a planning instrument for retirement with tax-free withdrawal.

Risk vs. Reward: Who Should Consider ULIPs?

ULIPs suit various investors depending on their risk tolerance and investment objectives.

Here are some of the common types of investors:

Aggressive Investors: Investors who can take more risk for potentially higher return can choose equity-based ULIPs.

Moderate Investors: Balanced growth with a combination of risk and stability is what you seek; you can go in for hybrid funds in ULIPs.

Conservative Investors: If the protection of capital is your concern, investing in debt funds under a ULIP guarantees steady but stable growth.

Conclusion

Whether you are risk-averse or not, ULIPs give you the freedom to change funds, enabling you to adjust to market volatility and shifting financial needs. A ULIP suits those who want a combination of insurance, investment, and tax relief benefits. If you have moderate to high risk tolerance and wish to create long-term wealth, a ULIP is an apt choice.

With Canara HSBC Life Insurance, you can choose from a range of ULIP plans tailored to your financial goals, ensuring a secure and prosperous future.

Glossary

Premium: The amount that is to be paid periodically to keep the policy active.

Corpus: The total accumulated amount in your ULIP investment over time.

ULIPs: A tax-saving investment combining insurance and market returns.

Compounding: Reinvestment of returns for exponential growth

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.