Meet our Advisor

Meet our Advisor

Enter OTP

An OTP has been sent to your mobile number

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Request Registered

Thank You for submitting the response, will get back with you.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

About Wealth Edge

In this policy the investment risk in investment portfolio will be borne by the policyholder

UIN 136L085V04

Canara HSBC Life Insurance Wealth Edge, a Unit Linked Individual Savings Life Insurance Plan, designed as per your needs. This plan recognizes the importance of your life goals and helps you fulfil them along with the added shield of life insurance to protect you and your family against any uncertainties in the future. It empowers you to deliver the promises you have made to your near and dear ones.

Plan Options

Depending upon your financial need, you can select your plan option (any ONE) from the following available options under this product.

Invest Plus

- Why Buy

- Benefits

- Other Benefits

- How it Works

- Age Criteria

- Police Term And Premium Payment Term

- Sum Assured Multiple

- Premium Payment Details

Why Buy

- Build your wealth over the years by investing a premium regularly in investment funds of your choice.

- Multiple Plan Options to choose from: ‘Invest Plus’, ‘Premium Plus’ or ‘Life Plus’.

- Recurring income with Systematic Withdrawal Option (SWO) / Milestone Withdrawal Option (MWO).

- Return of Mortality Charges, Loyalty Addition and Wealth Boosters to enhance your fund value.

- Flexibility with the option to alter your premiums, premium payment term, policy term and sum assured.

- Avail Tax Benefits.

Download Forms

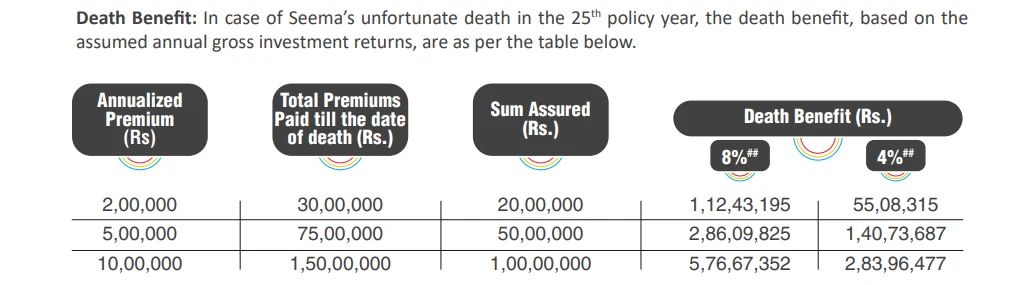

Death Benefit

Higher of:

- Sum Assured less partial withdrawals/ withdrawals under MWO / withdrawals under SWO, if any, in the preceding two years, or

- Fund Value as on date of intimation of death claim, or

- 105% of all Premiums paid up to the date of death

Maturity Benefit:

- Fund Value as on the date of maturity

Choice of Portfolio Management Strategies

1. Systematic Transfer Option (STO):

Reduces risks associated with lumpsum investing by investing in the equity market in a systematic manner. Entire Premium will be invested in the Liquid Fund and then systematically transferred on a monthly basis into an Equity Fund.

2. Return Protector Option (RPO):

Protects investment gains from future market volatility. Automatic transfer of investment gains from Equity Fund to Debt Fund.

3. Auto Funds Rebalancing (AFR):

Helps in maintaining investments in a specific proportion across different Unit Linked Funds, irrespective of market movements. After every 3 months, the investments are automatically rebalanced in in various Unit Linked Funds to the allocation proportions chosen by you.

4. Safety Switch Option (SSO):

The funds are systematically moved to a relatively low risk Liquid Fund in the last four policy years to avoid market movements and safeguard the funds near policy maturity

5. Loss Protector Strategy (LPO):

Protect investments in case of a market down turn. In case of a downturn in market investment is transferred from high risk to low risk funds, thus reducing the risk.

Choice of Funds

Choose from a range of 11 Unit Linked Funds to cater to your investment needs. You can choose to allocate your Premiums to any, all or a combination of the Unit Linked Funds as per your risk preference.

- Emerging Leaders Equity Fund

- India Multi-Cap Equity Fund

- Equity II Fund

- Growth Plus Fund

- Balanced Plus Fund

- Large Cap Advantage Fund

- Debt Fund

- Liquid Fund

- Midcap Momentum Growth Index Fund

- India Manufacturing Fund

- NextGen Consumption Fund

Additions in the Fund

Loyalty Additions":

Regular loyalty additions at the end of the each Policy Year, starting from the 6th Policy Year onwards till the end of chosen Policy Term equal to 0.5% of the average Fund Values of the last 12 monthly Policy anniversaries.

Wealth Boosters:

| At the end of | Wealth Booster (as a percentage of the average Fund Value of the last 60 monthly Policy Anniversaries) |

|---|---|

| 10th Policy Year | 2.90% |

| 15th Policy Year and thereafter at the end of every 5 Policy Years | 1.50% |

Return of Mortality Charges:

Total of all the Mortality Charges deducted during the Policy Term will be added to the Fund Value at the maturity date.

Product Flexibilities

Change in Premium Payment Term:

Flexibility to change your Premium Payment Term to align it with your changing financial situation.

Increase or Decrease of Sum Assured:

Option to alter your Sum Assured based on your protection needs.

Option to increase Policy Term:

Flexibility to change your Policy Term to align it with your changing horizon.

Settlement Option:

Option to receive your maturity benefit through Settlement Option in installments as per the frequency chosen, over a maximum period of 5 years.

Option to reduce premium:

You can choose to reduce your premium basis your financial needs.

| Eligibility Criteria | Minimum | Maximum |

|---|---|---|

| Age at entry | 0 years | 70 years |

| Maturity Age | 18 years | 80 years |

For Single Pay

| SA Cover Multiple | Age at Entry (in years) | PT (in years) |

|---|---|---|

| 10x | 0 to 38 | 5 to 20 |

| 10x | 39 to 44 | 5 to 10 |

| 10x | 45 to 47 | 5 |

| 1.25x | Less than 50 | 5 to 30 |

| 1.1x | 50 to 70 | 5 to 30 |

For Limited Pay

| Age at Entry (in years) | PPT (in years) | PT (in years) |

|---|---|---|

| 0 – 55 | 5/7/10/15/20/25 | 10 to 30 |

| 56 – 60 | 7/10/15 | 10 to 20 |

| 56 – 60 | 5 | 10 to 15 |

| 61– 65 | 7/10/15 | 10 to 15 |

For Regular Pay

| Age at Entry (in years) | PPT (in years) | PT (in years) |

|---|---|---|

| 0 – 70 | Same as PT | 10 to 30 |

Minimum

Age at Entry (in years)- less than 50: For Limited Pay / Regular Pay - 7 times the Annualized Premium

For Single Pay – 1.25 times the Single Premium

Age at Entry (in years) - 50 – 70: For Limited Pay / Regular Pay - 5 times the Annualized Premium

For Single Pay – 1.10 times the Single Premium

Maximum

| Age at Entry (in years) | Limited Pay | Regular Pay | Single Pay | |

|---|---|---|---|---|

| PT <=20 years | PT > 20 years | |||

| 0-30 | 40 | 40 | 40 | 10 |

| 31-40 | 25 | 20 | 40 | 10 |

| 41-45 | 20 | 15 | 30 | 10 |

| 46-47 | 15 | 10 | 20 | 10 |

| 47+ | 10 | 10 | 10 | 1.25 |

Premium Payment Details

| Premium Payment Mode | Minimum (Rs.) | Maximum (Rs.) |

|---|---|---|

| Annual | 1,25,000 per year | No Limit |

| Semi-Annual | 75,000 per half year | No Limit |

| Quarterly | 43,750 per quarter | No Limit |

| Monthly | 16,667 per month | No Limit |

| Single Premium | 1,25,000 | No Limit |

Premium Plus

- why Buy

- Benefits

- Other Benefits

- How it Works

- Age Criteria

- Policy Term and Premium Payment Term

- Sum Assured Multiple

- Premium Payment Details

Why Buy

- Build your wealth over the years by investing a premium regularly in investment funds of your choice.

- Multiple Plan Options to choose from: ‘Invest Plus’, ‘Premium Plus’ or ‘Life Plus’.

- Recurring income with Systematic Withdrawal Option (SWO) / Milestone Withdrawal Option (MWO).

- Return of Mortality Charges, Loyalty Addition and Wealth Boosters to enhance your fund value.

- Flexibility with the option to alter your premiums, premium payment term, policy term and sum assured.

- Avail Tax Benefits.

Download Forms

Death Benefit

Higher of:

1. Sum Assured, or

2. 105% of total premiums paid up to the date of death.

The future premiums are waived, future premiums are funded by the Company and the Fund Value is payable at maturity.

Maturity Benefit

Fund Value as on the date of maturity.

Choice of Portfolio Management Strategies

1. Systematic Transfer Option (STO):

Reduces risks associated with lumpsum investing by investing in the equity market in a systematic manner. Entire Premium will be invested in the Liquid Fund and then systematically transferred on a monthly basis into an Equity Fund.

2. Return Protector Option (RPO):

Protects investment gains from future market volatility. Automatic transfer of investment gains from Equity Fund to Debt Fund.

3. Auto Funds Rebalancing (AFR):

Helps in maintaining investments in a specific proportion across different Unit Linked Funds, irrespective of market movements. After every 3 months, the investments are automatically rebalanced in in various Unit Linked Funds to the allocation proportions chosen by you.

4. Safety Switch Option (SSO):

The funds are systematically moved to a relatively low risk Liquid Fund in the last four policy years to avoid market movements and safeguard the funds near policy maturity.

5. Loss Protector Strategy (LPO):

Protect investments in case of a market down turn. In case of a downturn in market investment is transferred from high risk to low risk funds, thus reducing the risk.

Choice of Funds

Choose from a range of 11 Unit Linked Funds to cater to your investment needs. You can choose to allocate your Premiums to any, all or a combination of the Unit Linked Funds as per your risk preference.

- Emerging Leaders Equity Fund

- India Multi-Cap Equity Fund

- Equity II Fund

- Growth Plus Fund

- Balanced Plus Fund

- Large Cap Advantage Fund

- Debt Fund

- Liquid Fund

- Midcap Momentum Growth Index Fund

- India Manufacturing Fund

- NextGen Consumption Fund

Additions in the Fund

Loyalty Additions:

Regular loyalty additions at the end of the each Policy Year, starting from the 6th Policy Year onwards till the end of chosen Policy Term equal to 0.5% of the average Fund Values of the last 12 monthly Policy anniversaries.

Wealth Boosters:

| At the end of | Wealth Booster (as a percentage of the average Fund Value of the last 60 monthly Policy Anniversaries) |

|---|---|

| 10th Policy Year | 2.90% |

| 15th Policy Year and thereafter at the end of every 5 Policy Years | 1.50% |

Return of Mortality Charges:

Total of all the Mortality Charges deducted during the Policy Term will be added to the Fund Value at the maturity date.

Product Flexibilities

Change in Premium Payment Term:

Flexibility to change your Premium Payment Term to align it with your changing financial situation.

Increase or Decrease of Sum Assured:

Option to alter your Sum Assured based on your protection needs.

Option to increase Policy Term:

Flexibility to change your Policy Term to align it with your changing horizon.

Settlement Option:

Option to receive your maturity benefit through Settlement Option in installments as per the frequency chosen, over a maximum period of 5 years.

Option to reduce premium:

You can choose to reduce your premium basis your financial needs.

| Eligibility Criteria | Minimum | Maximum |

|---|---|---|

| Age at entry | 18 years | 50 years |

| Maturity Age | 28 years | 80 years |

For Limited Pay

| Age at Entry (in years) | PPT (in years) | PT (in years) |

|---|---|---|

| 18 – 50 | 10 /15 / 20 / 25 | 15 to 30 |

| 18 – 50 | 5 / 7 | 10 to 15 |

For Regular Pay

| Age at Entry (in years) | PPT (in years) | PT (in years) |

|---|---|---|

| 18 – 50 | Same as PT | 10 to 30 |

Minimum

Age at Entry (in years)- less than 50 : 7 times the Annualized Premium

Age at Entry (in years) - 50 : 5 times the Annualized Premium

Maximum

| Age at Entry (in years) | Limited Pay | Regular Pay | |

|---|---|---|---|

| PT <=20 years | PT > 20 years | ||

| 0-30 | 40 | 40 | 40 |

| 31-40 | 25 | 20 | 40 |

| 41-45 | 20 | 15 | 30 |

| 46-47 | 15 | 10 | 20 |

| 47+ | 10 | 10 | 10 |

Premium Payment Details

| Premium Payment Mode | Minimum (Rs.) | Maximum (Rs.) |

|---|---|---|

| Annual | 1,25,000 per year | No Limit |

| Semi-Annual | 75,000 per half year | No Limit |

| Quarterly | 43,750 per quarter | No Limit |

| Monthly | 16,667 per month | No Limit |

Life Plus

- Why Buy

- Benefits

- Other Benefits

- How it Works

- Age Criteria

- Policy Term and Premium Payment Term

- Sum Assured Multiple

- Premium Payment Details

Why Buy

- Build your wealth over the years by investing a premium regularly in investment funds of your choice.

- Multiple Plan Options to choose from: ‘Invest Plus’, ‘Premium Plus’ or ‘Life Plus’.

- Recurring income with Systematic Withdrawal Option (SWO) / Milestone Withdrawal Option (MWO).

- Return of Mortality Charges, Loyalty Addition and Wealth Boosters to enhance your fund value.

- Flexibility with the option to alter your premiums, premium payment term, policy term and sum assured.

- Avail Tax Benefits.

Download Forms

Death Benefit:

Higher of:

1. Sum Assured less partial withdrawals/ withdrawals under MWO / withdrawals under SWO, if any, in the preceding two years, or

2. Fund Value as on date of intimation of death claim, or

3. 105% of all Premiums paid up to the date of death

Maturity Benefit:

Fund Value as on the date of maturity.

Choice of Portfolio Management Strategies

1. Systematic Transfer Option (STO):

Reduces risks associated with lumpsum investing by investing in the equity market in a systematic manner. Entire Premium will be invested in the Liquid Fund and then systematically transferred on a monthly basis into an Equity Fund.

2. Return Protector Option (RPO):

Protects investment gains from future market volatility. Automatic transfer of investment gains from Equity Fund to Debt Fund.

3. Auto Funds Rebalancing (AFR):

Helps in maintaining investments in a specific proportion across different Unit Linked Funds, irrespective of market movements. After every 3 months, the investments are automatically rebalanced in in various Unit Linked Funds to the allocation proportions chosen by you.

4. Safety Switch Option (SSO):

The funds are systematically moved to a relatively low risk Liquid Fund in the last four policy years to avoid market movements and safeguard the funds near policy maturity.

5. Loss Protector Strategy (LPO):

Protect investments in case of a market down turn. In case of a downturn in market investment is transferred from high risk to low risk funds, thus reducing the risk.

Choice of Funds:

Choose from a range of 11 Unit Linked Funds to cater to your investment needs. You can choose to allocate your Premiums to any, all or a combination of the Unit Linked Funds as per your risk preference.

- Emerging Leaders Equity Fund

- India Multi-Cap Equity Fund

- Equity II Fund

- Growth Plus Fund

- Balanced Plus Fund

- Large Cap Advantage Fund

- Debt Fund

- Liquid Fund

- Midcap Momentum Growth Index Fund

- India Manufacturing Fund

- NextGen Consumption Fund

Additions in the Fund

Loyalty Additions:

Regular loyalty additions at the end of the each Policy Year, starting from the 6th Policy Year onwards till the end of chosen Policy Term equal to 0.5% of the average Fund Values of the last 12 monthly Policy anniversaries.

Wealth Boosters:

| At the end of | Wealth Booster (as a percentage of the average Fund Value of the last 60 monthly Policy Anniversaries) |

|---|---|

| 10th Policy Year | 2.90% |

| 15th Policy Year and thereafter at the end of every 5 Policy Years | 1.50% |

Return of Mortality Charges:

Total of all the Mortality Charges deducted during the Policy Term will be added to the Fund Value at the maturity date.

Product Flexibilities

Change in Premium Payment Term:

Flexibility to change your Premium Payment Term to align it with your changing financial situation.

Increase or Decrease of Sum Assured:

Option to alter your Sum Assured based on your protection needs.

Option to increase Policy Term:

Flexibility to change your Policy Term to align it with your changing horizon.

Settlement Option:

Option to receive your maturity benefit through Settlement Option in installments as per the frequency chosen, over a maximum period of 5 years.

Option to reduce premium:

You can choose to reduce your premium basis your financial needs.

Age Criteria

| Eligibility Criteria | Minimum | Maximum |

|---|---|---|

| Age at entry | 18 years | 70 years |

| Maturity Age | Up till age 100 years |

| For Limited Pay | ||

|---|---|---|

| Age at Entry (in years) | PPT (in years) | PPT (in years) |

| 18 – 70 | 10 /15 / 20 / 25 | 100 – Age at entry |

| For Regular Pay | ||

|---|---|---|

| Age at Entry (in years) | PPT (in years) | PPT (in years) |

| 18 – 70 | Same as PT | 100 – Age at entry |

Minimum:

Age at Entry (in years)- less than 50 : 7 times the Annualized Premium

Age at Entry (in years) - 50 to 70 : 5 times the Annualized Premium

Maximum:

| Age at Entry (in years) | Limited Pay | Regular Pay |

|---|---|---|

| 0-30 | 40 | 40 |

| 31-40 | 25 | 40 |

| 41-45 | 20 | 30 |

| 46-47 | 15 | 20 |

| 47+ | 10 | 10 |

Premium Payment Details:

| Premium Payment Mode | Minimum (Rs.) | Maximum (Rs.) |

|---|---|---|

| Annual | 1,25,000 per year | No Limit |

| Semi-Annual | 75,000 per half year | No Limit |

| Quarterly | 43,750 per quarter | No Limit |

| Monthly | 16,667 per month | No Limit |

Popular Search

- What is ULIP?

- ULIP Tax Benefit

- ULIP Full Form

- ULIP Vs Term Insurance

- Best ULIP Plans

- Best ULIP Plan For Child

- Allocation Charges In ULIP

- ULIP Returns In 15 Years

- Difference Between ULIP and Mutual Fund

- ULIP Vs SIP

- Mortality Charges In ULIP

- What is NAV?

- How ULIP Works?

- Tips to Buy ULIPs

- ULIP Calculator

- Power of Compounding Calculator

- ULIP Tax Benefits in India