Written by : Knowledge Centre Team

2026-07-29

902 Views

Share

Whether you have just received your first salary cheque or started a family, you always have plenty of aspirations and goals in life. No matter how organised you are with the money somehow your goals always beat your income. However, that is only until you define your goals, make savings plans and have ways to work towards it.

So the first thing about beating, or more appropriately, meeting your goals is that your need to organise your goals. Organising is only the first step of planning, so let’s not confuse this as planning financial goals.

Before you can plan, you need to sort out the goals into the ones which need planning and the ones which don’t. You can also refer to these goals as ‘long-term goals’ and ‘short-term goals’ and then prioritise before you start planning.

You can plan all the goals in your urgent important matrix, except the kitchen expenses. The best way to manage kitchen expenses is to follow a monthly budget. However, for the rest of the goals, you can plan, save and invest money.

Most important of the three types of goals you can plan for are the long-term goals. Thus, this is where most of your planning efforts will go.

Which goals occupy your mind when you think of long-term goals; i.e. goals which are not urgent but important in your life? Here are a few which you can commonly find relevant:

Of all the goals you can add to the list, the retirement goal remains an exception to the investment planning strategy. Thus, we should try to keep the retirement planning separate from other goals.

Before we get into the use of ULIPs, you should have a clear understanding of your financial goal. The simplest way to develop a clear vision for your goal is to define them in the following terms:

For example, if you are defining the higher education goal for your child, it could be defined as – Accumulate ₹50 lakh in 15 years, with present allocation at ₹1 lakh.

Once you have defined your goal, you can start customizing a ULIP investment plan as per your needs. ULIPs have a lot of features you can use to your advantage while saving for your long-term goals:

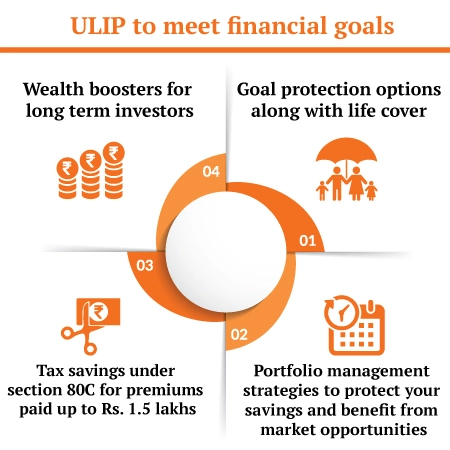

ULIPs are excellent long-term investment plans, as the longer you stay invested, the more benefits the offer. Wealth boosters especially benefit investors who stick with the plan for longer than five years.

The insurer will allocate bonus units to your portfolio every few years, provided:

Thus, to maximize your benefit from ULIP investment, you can use a single ULIP investment plan to meet multiple goals as well.

For example, your child’s education goal is 15 years away, while the marriage goal would be 20 years away. You can add your wealth-building goal to the same plan and continue investing for another 10 years.

Just remember that ULIPs have a lock-in period of five years. So, better not add a goal that is less than five years away to the ULIP investment plan.

If you want to invest in equity markets but do not feel confident if you can benefit from it, ULIPs have the perfect solution for you. Invest 4G ULIP plan from Canara HSBC Life, offers four different portfolio strategies to help you with your equity investment.

These strategies offer you the following advantages:

With Invest 4G plan you can choose at least two strategies to keep your intervention low in the investment plan.

Few goals like your child’s higher-education are too important for their future to be left to chance. For such goals, ULIP like Invest 4G plan provides additional protection. In case of your unfortunate demise before completing the goal, the insurer will:

This feature ensures that your child receives the money which you planned to provide for his/her higher education.

ULIP is a life insurance plan and thus any premium you pay is eligible for deduction under section 80C up to the limits (current. Rs 1.5 lakhs). Also, any pay-out or withdrawal from the fund is exempt from tax under section 10(10)D.

But these exemptions are subject to the following conditions: The annual premium (investment) should be less than 10% of the life cover sum assured

Thus, while starting your new ULIP investment plan, you should ensure that the life cover in the policy is slightly higher than 10 times of your annual investment. This way, you can even deposit additional money in the future when possible, without incurring any tax liabilities.

The retirement plan takes precedence over all other financial goals. Whether you are married, have kids of your own or not, retirement is one goal you must prepare for. You can use ULIPs to achieve your retirement goal as well.

However, you should take care of the following when it comes to retirement goal:

While traditional retirement solutions like NPS and PPF will allow incremental investments, ULIPs can boost your retirement corpus unlike any other. Plus, ULIP will also provide much-needed retirement safety to your spouse as well, in case anything happens to you.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.