Written by : Knowledge Centre Team

2025-10-02

984 Views

8 minutes read

Share

Himanshu and Shraddha Biswas got married 5 years ago. Although they had been careful with their financial needs, they lagged in planning for financial goals. Now they are parents to a 3-year-old child and seriously considering changing their investment habits for a better future for the child.

Let’s see if they can meet all their financial goals with a single ULIP investment plan.

ULIP stands for ‘unit-linked insurance plan,’ and is a versatile investment plan from life insurance companies. ULIPs allow you to invest in markets, fixed income (debt) and liquid funds as per your risk appetite.

ULIPs are the only investment option which allows you to move your funds between equity and fixed income funds without increasing your tax liability.

Also, the premiums you pay in the ULIPs help you save tax up to Rs. 1.5 lakhs under section 80C of the Income Tax Act. The maturity value or partial withdrawals from ULIPs are also tax-free under section 10(10D) provided:

So far as you keep this condition in mind while investing in ULIP, your investment returns remain tax-free.

Himanshu and Shraddha listed a number of serious financial goals for the family. After much deliberation they agreed on the following goals for being unavoidable and important:

To meet all these goals in their life they need money almost every five years.

Out of all the financial goals, retirement is one goal which should not be mixed with other goals. However, any funds left over from the savings of other goals can be added later to the retirement corpus for the family.

Since we are considering a single ULIP plan for achieving all these goals, we will need to keep the limitations of ULIP in mind:

For example, if you choose a life cover of Rs. 30 lakh, you can invest a maximum of Rs. 3 lakh a year to keep the investment entirely tax free at maturity.

Since the Biswas family has a long time of 30 years in their hands, they should choose a higher life cover. This will help them invest additional money if they have or need to later as their income and savings grow.

Although the Biswas couple plans to invest for a very long time, their financial advisor has recommended being conservative in their estimates. She recommended using an 8% p.a. rate of return on their investments and sees how many goals they can meet.

The couple can invest up to Rs. 50,000 a month towards these goals including the retirement goal. Their advisor recommends dedicating Rs. 20,000 a month towards retirement goal and the rest for others.

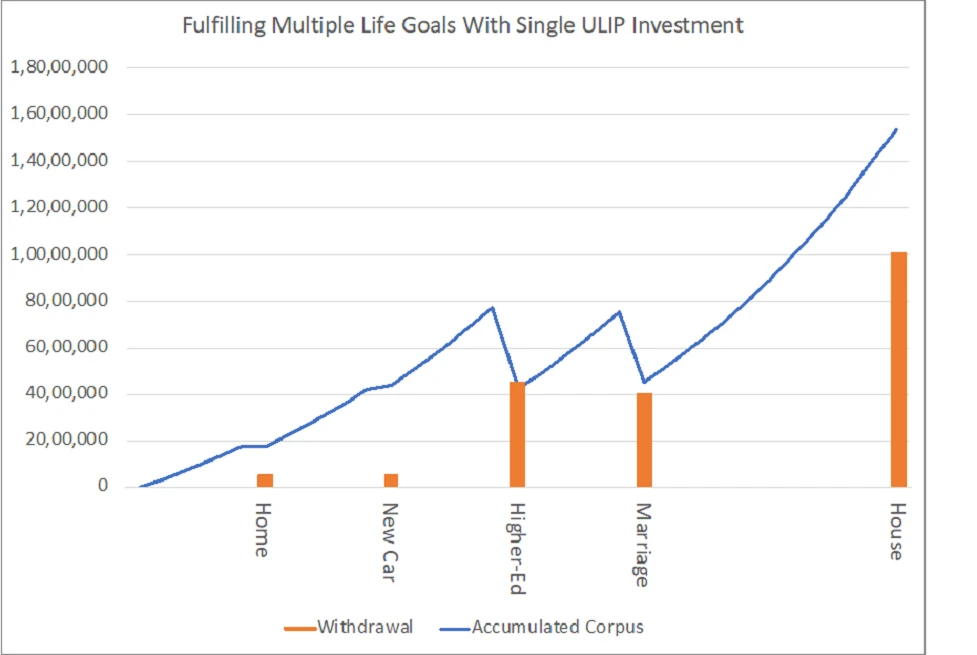

Here’s what their investment performance looks like when they keep withdrawing money to meet the goals on the way. (Figure: Investing Rs. 30,000 P.M. in one ULIP for 30 years)

Figure: Investing Rs. 30,000 P.M. in one ULIP for 30 years

At the end of the 30 years, the family will have an additional Rs. 53 lakhs, which they can use for any purpose as they deem fit.

If the Biswas invest the entire Rs. 50,000 in this same ULIP, they can also meet their retirement goal at the end of 30 years. However, retirement is one goal where you will probably not have the chance to remedy your corpus mismatch.

That’s why it is recommended that you keep the retirement savings separate from other goals. You may apply for a loan to fulfil other goals while you are still employed. But, with retirement, there is little chance of any such opportunities.

This one ULIP investment is going to be probably the most important one in your portfolio as it goes to a number of goals. Thus, you should look for features and benefits which will keep the journey smooth over a long period:

Automatic Portfolio Management Options

Automatic portfolio management options keep your engagement with the investments low and offer peace of mind while you focus on your income. Portfolio management options will offer the following advantages for your investment:

For example, ULIP plan from Canara HSBC Life, Promise4Growth Plus offers four portfolio management strategies for you to choose. You can use these strategies to:

You can choose one of these strategies to manage your long term investments in the ULIP and achieve multiple goals within the policy tenure.

Additional Benefits of Promise4Growth Plus Plan

Promise4Growth Plus also offers additional benefits, especially for long-term investors in the plan. The plan will add bonus units to your existing portfolio at regular intervals. These bonus additions are called boosters. You can avail these, provided you:

We all have multiple financial goals in life. If we consider only the important financial goals, even then we can have multiple goals that will need money every few years. Can a single ULIP investment plan fulfil these multiple obligations?

Of course, it can. However, you can club similar goals together for better results. For example, use one ULIP for the goals of your child, and another for your own. This way it is easier to keep track of the goals when they are under or over-funded.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.