Written by : Knowledge Centre Team

2025-11-02

979 Views

8 minutes read

Share

There is no rocket science behind building wealth. All you need to do is to understand the power of compounding. Your regular savings plans can gradually multiply into a sizeable corpus due to the compounding interest applying to them. Various practical investment approaches can help you grow your wealth. One of them is recurring investments strategies.

A recurring investment is a type of activity where you can invest a fixed amount of money into a particular investment plan. Investment plans which allow recurring investments also help you build wealth at your own pace.

A recurring investment strategy has many benefits. Some of the prominent benefits include:

Rupee cost averaging is the key benefit of any recurring investment strategy. This benefit is more useful in the case of high-risk or volatile investments like equity stocks or funds.

Rupee cost averaging refers to the resulting average purchase price as you continue to invest the same amount at different fund NAVs. As you receive fewer units at higher rates and more at lower rates, your overall average cost comes down.

Your aim is to eventually get the average cost of your fund units lower than the average price (NAV) of the fund. This way even in a level market, your portfolio will remain profitable.

Also, you can avoid the complex or even impossible duty of trying to figure out the exact best time to invest.

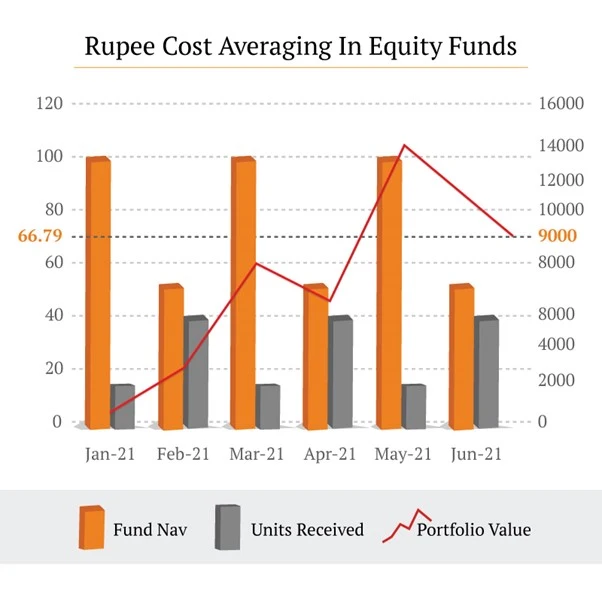

Rupee cost averaging works best in volatile investment plans like equity funds. For example, have a look at the table below:

If you invest in an equity fund through SIPs here’s how your unit allocation will work:

| Month | SIP Amount (₹) | Fund NAV | Units Received | Portfolio Value |

|---|---|---|---|---|

| Jan-20 | 2,000 | 100 | 20 | 2000 |

| Feb-20 | 2,000 | 50 | 40 | 3000 |

| Mar-20 | 2,000 | 100 | 20 | 8000 |

| Apr-20 | 2,000 | 50 | 40 | 6000 |

| May-20 | 2,000 | 100 | 20 | 14000 |

| Jun-20 | 2,000 | 50 | 40 | 9000 |

| Total | 12,000 | 180 |

The average NAV of the Fund in the past six months: Rs 75

The average NAV of portfolio: Rs. 66.67

Thus, the average cost of the portfolio goes below the market average. This gap will continue to increase as you continue the SIP into the fund.

Rupee cost averaging ensures that your portfolio value keeps increasing even when the market remains stagnant.

ULIPs have features to allow recurring investment for every investor. Whether you want to invest monthly, quarterly or annually, if you invest in ULIP you have the option of a recurring investment strategy. Here’s how:

For example, if you can only invest once a year, the systematic transfer will ensure that your funds are allocated to equity funds as SIP.

Under this option, your entire annual premium will be allocated first to a liquid fund in the policy. Afterwards, the units in the liquid funds will be systematically transferred to the equity funds you chose. The transfer occurs every month over the next 12 months. Thus, about 1/12th of your annual allocation to equity fund will be invested in the equity fund, same as a monthly SIP.

Your Fund Value available in the Liquid Fund at the start of every month shall be transferred to the 'Target STO Fund' by cancelling Liquid Fund units and purchasing units in the 'Target STO Fund'. This will continue till the availability of your Liquid fund units.

These are some of the ways how a ULIP can work as one of the best recurring investment strategies.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.