Market-Linked Growth with Life Cover Benefits

Enter OTP

An OTP has been sent to your mobile number

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Request Registered

Thank You for submitting the response, will get back with you.

Complaint Registered

. Please use this ID for all future communications regarding this concern.Request Registered

Thank You for submitting the response, will get back with you.

Request Registered

Thank You for submitting the response, will get back with you.

Table Of Content:

ULI is a plan that includes dual investment and life insurance benefits. ULIP full form is Unit Linked Insurance Plan.

Investing in the best ULIP can help you achieve long-term wealth creation and life coverage. It is the best investment option to meet your financial goals. Buy ULIP from Canara HSBC Life Insurance to get life cover, multiple portfolio management options, flexible premium paying options, tax benefits, and a wide array of other benefits.

Key Takeaways

|

What is a ULIP Plan?

A ULIP is an insurance product that provides you with the double benefit of investment to achieve long-term wealth creation goal, and a life cover to secure your family’s future if there is an unfortunate event. The premium paid for ULIP is divided into two parts. One part of the premium is used for your life cover and the remaining sum is invested in the fund of your choice. In ULIP plans, you can invest your money in equity, debt or a combination of both funds depending on your risk appetite. The returns on the investment depend upon the performance of the funds.

How Does a ULIP Investment Plan Work?

A ULIP has a predetermined death benefit, which is paid to the nominee in case of an unfortunate event. In addition, if the policyholder survives the term of the ULIP, they receive the maturity value of the ULIP, which is the amount generated by the ULIP investments in equity and debt funds.

While the maturity benefit is subject to market-linked risks, the insurance cover under a ULIP remains fixed. Like any other insurance policy, you need to pay a premium for a unit-linked insurance plan. In ULIP, the insurance company deducts a portion of the premium towards life cover, and the rest is invested in a number of qualified funds. Afterwards, you get returns based on the performance of the funds you opted for. There are several investment options, such as debt funds, equity funds, hybrid funds, etc., for you to choose from.

The total investment is then divided into 'units' with unique face values, and every investor is allocated 'Units' based on their investment amount.

A Unit Linked Insurance Plan is a one-stop option for those looking for a long-term investment instrument that offers both transparency and flexibility. Also, it’s a perfect choice for those looking for a cost-effective way to enter the investment market. ULIPs come with a range of fund options that help meet the policyholder's investment needs. In addition, here are a few more reasons that show the need to buy a ULIP scheme:

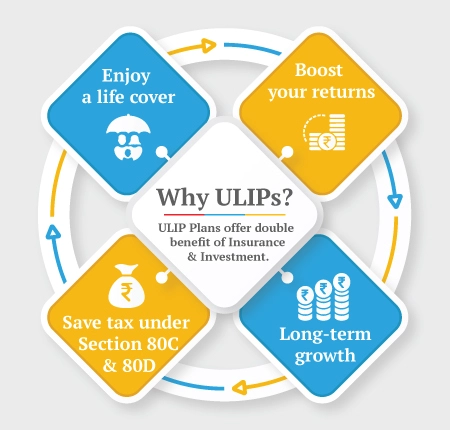

- To Avail Tax Benefits: If you are looking for an investment instrument that helps you save on taxes, then a ULIP can be suitable for you. You can enjoy tax benefits on the premiums that you pay towards the policy, as per Section 80C of the Income Tax Act. Also, death benefits paid under the plan are exempt from tax as per Section 10(10D) of the Income Tax Act. However, for policies issued on or after 1 February 2021, maturity proceeds are tax-exempt only if the aggregate annual premium of ULIP policies does not exceed ₹2.5 lakh, as per prevailing tax laws.

- To Enjoy Dual Benefits Packed in a Single Plan: It offers a dual benefit of insurance and investment in a single policy. A ULIP plan not only offers life cover that protects your family against financial difficulties but also provides multiple investment instruments that help you maximise your returns.

- Higher Returns Potential: ULIPs provide exposure to market-linked investment options through a range of fund options. This includes debt, equity, hybrid funds, and many more. You can choose any of these based on their performance and your risk appetite. You are also allowed to switch between funds based on the market outlook.

- Long-term Wealth Creation: If you want to meet your long-term financial goals, then switching to ULIP can be considered a wise long-term investment choice. It comes with a five year lock-in period, keeping you invested for a longer tenure. This accumulated money helps you meet your long-term financial goals, such as buying a house or car, children’s education, marriage, or other major financial objectives.

Features of ULIP Plans

With a ULIP, you have the flexibility to select your fund as per your risk appetite. ULIPs come with a variety of funds to choose from. Investors with a low risk appetite can invest in debt funds, while those with a high risk appetite can invest in equity funds.

- Lock-in Period: ULIPs come with a lock-in period of 5 years and may offer the potential for wealth creation when invested over a long period of time. Therefore, it can be said that the longer you stay invested in a ULIP, the more it may support your long-term investment goals.

- Premium Payment Options: You can choose a single premium (one-time lump-sum payment at policy inception), a limited premium option (payments for a fixed period with continued coverage), or a regular premium (payments made throughout the policy term).

- Liquidity: ULIPs also allow you to partially withdraw a sum when you need it after the completion of the lock-in period. Simply put, ULIP provide liquidity only after the lock-in period is over.

Get a Personalised ULIP Plan for Wealth Creation & Protection

Enter OTP

An OTP has been sent to your mobile number

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

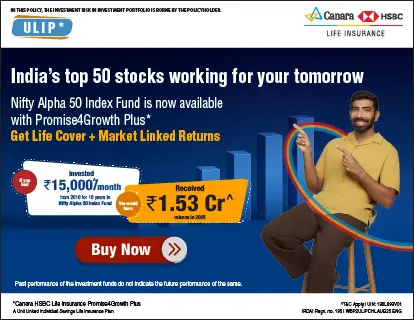

ULIP Plans Offered by Canara HSBC Life Insurance

Canara HSBC Life Insurance offers a range of ULIP plans designed to meet different investment objectives, risk appetites, and protection needs. These plans combine market-linked investment opportunities with life insurance protection while offering flexible fund options, growth enhancers, and value-added features to support long-term financial planning.

Product (UIN) | Fund Options | Growth Enhancers / Value Additions | Life Cover & Safeguard Features | Payout & Tax Advantages | CTA |

Canara HSBC Life Insurance Promise4Growth Plus (136L093V01) | 13 Fund Options | Return of Mortality Charges (RoMC) added back at maturity | Premium Funding Benefit – future premiums paid by insurer in case of death | Fund value payable at maturity; tax benefits as per prevailing laws | Check Plan Details |

Canara HSBC Life Insurance SecureInvest (136L092V01) | 12 Fund Options | Loyalty Additions from year 10 and Maturity Booster; twice the Premium Allocation and Mortality Charges added back to the fund | High life cover up to 100× annualised premium | Premiums and returns qualify for tax benefits as per the prevailing Income Tax Act, 1961 | Check Plan Details |

Canara HSBC Life Insurance Wealth Edge (136L085V03) | 10 Fund Options + 5 Portfolio Strategies | Return of Mortality Charges, Loyalty Additions, and Wealth Boosters; 0.5% of average fund value added yearly from the 6th policy year onward | Life cover up to age 100; waiver of future premiums in case of death if the fund remains invested (Premium Plus variant) | Fund value payable at maturity; tax benefits as per prevailing laws | Check Plan Details |

These ULIP plans are structured to cater to different financial priorities:

Promise4Growth Plus: Designed for investors looking to balance wealth creation with life protection, while also benefiting from flexible premium payment options and multiple fund choices.

SecureInvest: Suitable for individuals focused on long-term wealth accumulation with high life cover, supported by loyalty additions and disciplined investment structures.

Wealth Edge: Best suited for investors seeking aggressive wealth creation and flexible fund allocation, including equity-oriented strategies with long-term growth potential.

Together, these plans provide diverse fund choices, life cover options, premium flexibility, and long-term investment opportunities, helping investors align their insurance and investment needs with evolving financial goals.

Unit Linked Insurance Plans - Top Selling Plans

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.

Wealth Today, Protection Always

- Life Cover up to 100 Years

- 13 Fund Options

- Fund Switching Option

- Waiver Of Premium

Secure Your Future with Confidence

- Life Cover up to 100× Annual Premium

- 12 Fund Choices

- Automated Portfolio Strategies

- Maturity Booster

Invest Smart, Live Smart

- Flexible Premium Options

- Multiple Fund Allocations

- Systematic Withdrawals

- Premium Waiver Benefit

Benefits of a ULIP Plan

A ULIP plan offers several features that support long-term financial planning and flexibility. Some of the key benefits of a ULIP plan are explained below.

- Flexibility: ULIP plans allow you to switch to a different investment option. This can be useful if you do not have fixed financial goals or wish to rebalance your investments by shifting between funds. It provides you with greater flexibility by allowing you to control where and in what proportion your money is invested. The following features provided by ULIPs enable this flexibility:

- Fund Switching Option: Through the use of this feature, you can move your money between funds based on your investment preferences. For example, you may have invested a significant portion of your money in equity funds and now wish to transfer some of it to safer debt funds. The fund switching option allows you to do this.

- Redirection of Premium: ULIPs provide multiple fund options for investment. If you have invested in one fund earlier and no longer find it suitable, you can choose another fund, and the future premiums will be redirected to that fund.

- Partial Withdrawal Facility: This option allows you to withdraw a portion of your funds if required, subject to policy terms and the completion of the lock-in period.

- Top-up Facility: Through this feature, you can add additional funds to your existing ULIP investment without changing the policy.

- Transparency: ULIPs offer a high level of transparency. With ULIPs, you are informed about the charges associated with the policy. All charges, such as fund management charges, policy administration charges, and other applicable fees, are disclosed upfront before you buy the product.

- Tax Benefits: ULIP are efficient tax-saving instruments. The premium you pay for the policy may qualify for a tax deduction under Section 80C of the Income Tax Act, subject to applicable conditions.

- Ideal for Long-term investment goals: It is perfect for long-term investment objectives. Before investing in a ULIP plan, it is advisable to make a list of your long-term financial goals to fulfil through investing, such as funding higher education, purchasing a house, or planning major life events.

- Market-Linked Returns: The returns earned through a ULIP policy are market-linked and depend on the performance of the chosen investment funds. The premium paid is invested in different funds, which may include debt, equity, or a combination of both. Monitoring the Net Asset Value (NAV) of the funds can help track investment performance.

- Death Benefits: Since Unit Linked Insurance Plans also provide life insurance cover, they offer death benefits to the nominee. This refers to the amount paid to the nominee if the policyholder passes away during the policy term. The death benefit may vary depending on the policy structure and plan type, and is typically the higher of the sum assured, the fund value, or both.

- Maturity Benefits: Apart from death benefits, ULIPs also provide maturity benefits. If the policyholder survives the policy term, they are entitled to receive the maturity value, which represents the accumulated fund value at the end of the policy tenure.

- Withdrawal Benefits: This feature allows partial withdrawals from the ULIP investment after the mandatory lock-in period ends. It can be useful in situations where funds are required during the policy term, subject to policy conditions and applicable rules.

Different Types of ULIP (Unit Linked Insurane Plans)?

Given below are the different types of ULIPs, categorised based on their investment funds and policy structure:

- Based on Funds Options: A ULIP typically offers multiple types of funds, each with a distinct investment strategy. The funds you choose within the policy are invested in various financial instruments, such as equities, bonds, and money market instruments. Here’s a breakdown of the various types of ULIP based on the funds they offer:

- Equity Funds: These are among the most common options in ULIPs that primarily invest in stocks and equity markets, providing high growth potential. Due to their focus on equities, these funds tend to be riskier compared to other types, but they offer potentially higher returns over the long term.

- Debt Funds: These are designed to provide more stable returns by investing in fixed-income instruments such as bonds, government securities, or corporate debt. Debt funds in ULIP are less volatile in comparison to the equity funds and offer lower but more predictable returns.

- Balanced Funds: These are also known as hybrid funds, and aim to strike a balance between equity and debt. These funds typically allocate a portion of the corpus to equities for growth potential and the rest to debt for stability and income. They are designed to offer a moderate level of risk and return.

- Liquid Funds: These are designed to offer a high level of liquidity and stability by investing primarily in short-term debt instruments like Treasury Bills, certificates of deposit, and commercial papers. These funds are generally suitable for individuals who want to maintain easy access to their money while earning a relatively stable return.

- Based on Purpose: ULIPs can also be categorised based on the financial objective they are designed to support. These plans are structured to help policyholders work towards specific life goals such as wealth creation, retirement planning, or securing a child’s future.

- ULIPs for Wealth Creation: These are designed for individuals looking to build long-term capital through market-linked investments. ULIPs for wealth creation typically offer multiple fund options and allow investors to grow their wealth over time while also benefiting from life insurance coverage.

- ULIPs for Retirement and Pension Planning: These are structured to help individuals build a corpus for their retirement years. These retirement ULIPs focus on long-term savings and wealth creation, with the primary goal of securing the policyholder’s financial future after retirement.

- ULIPs for Child’s Future Planning: These are specially designed to secure the future of a child, both in terms of education and financial security. Child future planning ULIPs are typically structured to accumulate a large corpus over a long investment period, providing a mix of life insurance and market-linked returns.

- ULIPs for Health: Some ULIP plans allow policyholders to add a critical illness rider to enhance the policy's protection component. Under this rider, the policyholder may receive a lump-sum benefit if diagnosed with a specified critical illness, as defined in the policy terms. While the ULIP investment remains market-linked, the rider adds an additional layer of financial protection against major medical conditions.

- Based on Premium Payment Options: ULIP plans may also differ based on how the policyholder chooses to pay the premium.

- Single Premium ULIP: In this type of ULIP, the policyholder pays a one-time lump-sum premium at the start of the policy term. The amount is then invested in the chosen funds for the entire duration of the policy.

- Limited Premium ULIP: Limited premium ULIPs require premium payments only for a specified period, while the policy benefits continue for the entire policy term.

- Regular Premium ULIP: In regular premium ULIPs, the policyholder pays premiums at regular intervals throughout the policy term, such as annually, semi-annually, or monthly.

- Based on Life Cover: The death benefit is an important component of a ULIP policy as it provides financial protection to the nominee in the event of the policyholder’s death during the policy term. Based on how the life cover is structured, ULIP plans are generally classified into two categories.

- Higher of Sum Assured or Fund Value: In this type of ULIP, the nominee receives either the sum assured or the fund value, whichever is higher, in the event of the policyholder’s death. The sum assured represents the minimum guaranteed life cover under the policy, while the fund value reflects the value of investments made in the chosen market-linked funds. Since the fund value is linked to market performance, it may fluctuate over time.

- Sum Assured plus Fund Value: In this type, the nominee receives both the sum assured and the accumulated fund value if the policyholder passes away during the policy term. Because the payout includes both components, this structure generally provides greater financial protection for dependents. As a result, premiums for these types of ULIPs are usually higher than those for the previous one. These plans may be suitable for individuals who wish to prioritise higher life cover and market-linked investment exposure.

Did You Know?

ULIP gains from policies with annual premiums above ₹2.5 lakh are taxed as capital gains, similar to equity mutual funds.

Source: Mint

How to Choose the Best ULIP Plan in India?

Selecting the right ULIP fund depends on your risk appetite, investment horizon, and financial goals. The table below highlights which types of ULIP funds may suit different investor profiles.

Investor Type | Types of ULIP Suited |

Risk-Taking Investor | If you have a high-risk appetite, then you may consider investing in equity instruments. They offer potential for higher returns, but also carry higher market risk. |

Risk-Averse Investor | If you have a low-risk appetite, then you may consider investing in debt funds, such as fixed-income bonds or government securities. They offer relatively lower returns, and the associated risks are generally lower. |

Moderate Risk Investor | If you are willing to take some risk but prefer balanced exposure, balanced or hybrid funds may be suitable, as they invest in both equities and debt, which can help moderate overall risk. |

ULIP vs Other Investment Options

Investors often compare ULIP plans with other popular investment options to understand how they differ in terms of protection, returns, flexibility, and tax treatment. The table below highlights the key differences between ULIP insurance and other investment instruments such as SIP, mutual funds, PPF, and fixed deposits.

Investment Option | Life Cover | Lock-in | Returns Type | Tax Benefit | Flexibility |

ULIP | Yes, includes life insurance cover along with investment | 5-year mandatory lock-in period | Market-linked returns depending on fund performance | Premiums may qualify for deduction under Section 80C; maturity benefits may be tax-exempt under Section 10(10D), subject to applicable conditions | Allows fund switching, partial withdrawals after lock-in, and top-up investments |

No life cover | No mandatory lock-in (except ELSS funds) | Market-linked returns based on mutual fund performance | Tax benefits only if invested in ELSS funds under Section 80C | High flexibility with the option to start, stop, or modify SIP contributions | |

Mutual Funds | No life cover | Generally, no lock-in, except ELSS funds with a 3-year lock-in | Market-linked returns depending on fund type and market performance | ELSS funds qualify for Section 80C tax deduction; other funds taxed as per capital gains rules | Flexible investment options with the ability to redeem units anytime (subject to exit load) |

PPF (Public Provident Fund) | No life cover | 15 year lock-in period with limited withdrawal options | Government-backed fixed interest rate declared periodically | Eligible for tax deduction under Section 80C with tax-free maturity under the EEE regime | Limited flexibility with restricted withdrawal and contribution limits |

Fixed Deposit (FD) | No life cover | Tenure-based lock-in depending on the deposit period | Fixed and predetermined interest rate | Tax-saving FDs qualify for Section 80C deduction with a five year lock-in | Limited flexibility; premature withdrawal may attract penalties |

ULIP Returns: How to Calculate and Maximise

The returns of ULIP plans are usually calculated in two ways which are listed below:

Absolute Returns:

Absolute returns calculate the percentage increase in the ULIP investment value. It’s essentially the difference between the current value of your investment and its value when you initially purchased the units, adjusted for any expenses like management and administrative charges.

Absolute Return = [(Current value − Purchase value) / Purchase value] × 100

For example, if you purchased your ULIP units for ₹450 and the value increased to ₹650 after one year, your absolute return would be:

Absolute Return = [(650 − 450) / 450] × 100 = 44.4%

This method works best for short-term investments where you're looking to see how much your investment has grown over a specific time frame.

CAGR (Compound Annual Growth Rate):

CAGR provides a more accurate measure of long-term growth, as it shows the annualised return over a set number of years. Unlike absolute returns, which give you a snapshot of growth, CAGR accounts for growth over multiple years and smooths out fluctuations, calculating the consistent growth rate your investment would have achieved annually to reach its current value.

CAGR = {[(Current value / Value at the time of purchase) ^ (1 / Number of years)] − 1} × 100

For instance, if your ULIP investment was worth ₹250 when purchased and its value grew to ₹350 over five years, the CAGR would be:

CAGR = [(350 / 250)^(1/5) − 1] × 100 ≈ 6.96%

CAGR is particularly useful for evaluating investments over longer periods as it reflects the annualised growth rate, helping you compare the performance of your ULIP investment with other investment options.

Tips to Maximise the Potential of Your ULIP Returns:

While returns can be measured using methods such as absolute returns and CAGR, investors can also take certain steps to optimise their ULIP investments over time.

Choose Funds Based on Risk Appetite: Select equity, debt, or balanced funds based on your risk tolerance and financial goals

Stay Invested for the Long Term: Remaining invested beyond the 5-year lock-in period may help your investment benefit from long-term market growth

Use the Fund Switching Option: ULIPs allow you to switch between funds based on market conditions or changing financial priorities

Consider Top-Up Investments: The top-up facility allows you to add additional funds to your ULIP policy when you have surplus savings

ULIP Tax Benefits

Claiming tax benefits for your Unit Linked Insurance Plans (ULIP) is relatively straightforward, but it is essential to understand the key sections under the Income Tax Act that apply to ULIPs.

Under Section 80C, the premiums paid towards your ULIP are eligible for a tax deduction of up to ₹1.5 lakh per year, helping reduce your taxable income.

The tax treatment of ULIP maturity proceeds depends on the date of policy issuance and the premium amount. For ULIP policies issued before 1 February 2021, the maturity proceeds are generally tax-exempt under Section 10(10D), irrespective of the premium amount. However, for ULIPs issued on or after 1 February 2021, the maturity amount may be taxable under the head “Capital Gains” if the aggregate annual premium exceeds ₹2.5 lakh, as per prevailing tax provisions.

It is important to note that death benefits received by the nominee are fully exempt from tax under Section 10(10D).

If a ULIP policy is withdrawn or surrendered before the completion of the mandatory five-year lock-in period, the proceeds may become taxable under the head “Income from Other Sources”, and any tax deduction previously claimed under Section 80C may also be reversed and added back to taxable income in that year.

To claim these benefits, ensure you maintain all relevant documents, such as premium receipts and policy details. When filing your tax returns, you’ll need to declare the premium paid under Section 80C, and the maturity or death benefits under Section 10(10D) may be treated as tax-exempt, subject to applicable conditions. If you surrender your policy, ensure it meets the criteria for tax-free treatment, especially if the lock-in period is over. Consulting a tax professional is always a good idea to ensure that you maximise the tax-saving potential from your ULIP investment.

ULIP Fees and Charges

Before investing in a Unit Linked Insurance Plan, you must know about the charges that you may have to pay throughout the policy term. The structure and applicability of charges may differ from one insurer to another, but here are some of the most common ULIP charges and fees.

Premium Allocation ChargesThis is a fixed percentage that is reduced from the premium at a higher rate in the policy's early years. This fee is charged by the insurance company before the policy is issued. This includes charges such as initial and renewal expenses, medical expenses, etc |

Policy Administration ChargesInsurance companies impose policy administration charges that are deducted periodically, often on a monthly basis. Such charges are imposed for managing the administration of your policy. |

Fund Management ChargesAs the name suggests, fund management charges are imposed for managing your funds and investment portfolio. |

Partial Withdrawal ChargesULIP allows partial withdrawals of funds, allowing investors to withdraw money partially after the lock-in period. However, such withdrawals may attract certain charges depending on the policy conditions. |

Mortality ChargesThese charges depend upon a number of factors such as age, the amount of sum assured, and other underwriting charges. For instance, if you are buying a policy at the age of 25, then your mortality charge will be lower because the life expectancy of a 25-year-old is higher than that of a 50-year old. This is deducted periodically, usually on a monthly basis. |

Switching ChargesMoving your investments from one fund to another is called switching in ULIP. It allows investors to switch between funds each year based on their performance and risk appetite. However, depending on the insurance company’s charging structure, each switch may attract certain charges after the free switch limit is exhausted. |

Rider Charges:These types of charges are levied on additional riders. For example, if you want to opt for a critical illness rider, you will have to pay an additional premium or a rider charge. |

Surrender Charges:These charges will be imposed if you decide to discontinue your ULIP policy within the mandatory lock-in period of five years. No charges apply after the lock-in period has been completed. Surrender charges are levied on the total value of the fund as per the policy terms. |

How to Manage Your ULIP Investment?

Unit Linked Insurance Plan(ULIP) is a long-term investment instrument that helps you achieve financial goals in a structured manner. However, to make the most out of your Unit Linked Insurance Plan, you need to learn how to manage it wisely. You need to ensure that your returns are balanced across different asset classes so that any loss caused by one asset class may be offset by another, thereby minimising the overall risk of your investments. Here are some tips that will help you manage ULIP effectively

- Balance Between Equity-Debt Portfolio: ULIP plans allow you to switch between different asset classes. Each asset has different characteristics, such as equity funds, which are ideal for investors who are comfortable with taking risks. It happens to be riskier than other funds but offers higher returns. On the other hand, debt funds generally carry lower risk but may offer relatively lower returns. They are often suitable for investors who are risk-averse. Thus, you need to balance the investment portfolio between equity and debt funds.

- Stay Updated With the Market: It is advisable to keep yourself updated with the market trends and economic conditions, as this will help you make more informed investment decisions. For example, if you have invested in equity fundsmarket conditions change, making the equity market appear overvalued, you may consider switching to other fund options, such as debt funds. You may reallocate later based on the market trends.

- Understand Life Stage Needs: Choosing between equity and debt funds mainly depends on your life stage needs and financial priorities. Thus, a policyholder needs to understand their evolving financial needs, as investors may become more risk-averse over time. Therefore, you may consider gradually shifting from equity funds to relatively stable debt funds as you get older.

Overall, ULIP is a market-linked insurance plan. Keeping market fluctuations in mind, you need to manage them effectively to reduce risk and achieve higher returns.

How to Choose the Best ULIP Plan?

Choosing the right ULIP plan requires evaluating your financial goals, risk appetite, investment horizon, and life cover needs to ensure the plan aligns with your long-term financial strategy.

- Choose the Fund Option That Aligns With Your Goal: ULIP policies provide you with the flexibility in choosing the funds you want. It will be better if you choose the fund options that can help you reach your goal effectively. Investing in equity can grow your funds higher in the long term but it also has a high risk involved. Whereas debt funds are safer and less reactive to market changes, but returns are safer, lesser. So, it is necessary to identify the goal first and then choose the fund accordingly.

- Choose a Suitable Life Insurance Cover Amount: Other than providing the opportunity of investment, ULIP provides you with life coverage as well. This helps in securing your family in case something happens to you. So, in this regard, you must choose a life cover that will be sufficient for your family to achieve their goals.

- Stay for as Long as You Can Under Your ULIP: ULIP are a long-term investment plan. So, it can give you the best results when you stay invested longer. This is why ULIP have a lock-in period of 5 years. The longer you stay in the policy, the more time you are giving your investments to grow. This will allow you to create huge wealth due to compounded returns.

- Maximum Tax Saving Benefits of ULIP: ULIP plans provide you with tax benefits. There are deductions as per the Income Tax Act 1961available under various sections if you have invested in ULIP. These involve:

- A deduction of up to ₹ 1.5 Lakh is available on the premium that is paid towards the policy under section 80C

- Also, the maturity, as well as the death benefits received, are tax-free under section 10(10)D

Things to Keep in Mind Before Investing in a ULIP Plan

Before investing in a ULIP plan, it is important to evaluate certain factors to ensure that the policy aligns with your financial goals and risk profile.

- Risk Appetite: You must know your risk appetite before investing in a ULIP. This plan offers a wide range of funds to choose from based on your needs and risk appetite. Those who are reluctant to take risks can allocate a larger portion of their investment in debt funds, while those who are comfortable taking risks can go for equities

- Charges in your ULIP: This investment cum insurance plan comes with a set of charges. Thus, before purchasing the policy, you need to understand the following charges:

- Mortality/Morbidity charges

- Policy Administration charges

- Fund Management charges

- Premium Allocation charges

- Flexibility: ULIP offers you the flexibility to switch between the funds. When buying a ULIP, you must consider the cost and ease of switching, as well as complimentary switches during the policy period.

- Premium Payment Option: ULIP offers three payment options: single, limited, and regular. Therefore, compare and choose a plan that you are comfortable with.

Common Mistakes When Buying a ULIP

ULIPs are popular financial instruments that offer a flexible and tax-efficient way to build wealth. However, they can be complex and often lead to mistakes that affect returns or policy effectiveness. To maximise the benefits of a ULIP, it’s important to be aware of the common pitfalls listed below and avoid them when making your purchase.

- Not Understanding the Cost Structure: ULIP usually comes with various charges such as premium allocation charges, fund management fees, mortality charges, and administration charges. Failing to factor these in can lead to unexpected deductions from your investment returns. Always ask for a detailed breakdown of these charges and evaluate how they might affect your investment's overall growth.

- Ignoring the Lock-In Period: ULIP typically comes with a lock-in period of five years, meaning you cannot withdraw your investment or make major changes during this time. Many investors overlook this aspect and may want to withdraw or make changes before the lock-in period ends, which could incur penalties or reduce the overall returns. Be sure you are ready for a long-term commitment before opting for a ULIP.

- Overlooking the Fund Options and Risk Profile: Not all ULIP are the same, and each policy offers a variety of investment options, ranging from equity to debt and balanced funds. A common mistake is investing in a fund that doesn't align with your risk tolerance or financial goals.

- Focusing Too Much on Short-Term Performance: ULIP are long-term financial products, and their performance needs to be evaluated over several years rather than in the short term. Many investors make the mistake of monitoring the short-term fluctuations in the Net Asset Value (NAV) and making hasty decisions based on market movements. ULIP are designed to deliver long-term growth, and reacting to short-term market conditions can lead to missed growth opportunities.

- Forgetting About the Switching Charges: Many ULIP allow policyholders to switch between funds (equity, debt, or balanced), but frequent switching can attract charges. While switching can be a good strategy during market fluctuations, overdoing it can lead to unnecessary costs. Evaluate the switching charges and try to limit the number of changes to maintain your investment's cost-effectiveness.

How to Choose the Right Life Cover in a ULIP Plan?

Selecting the appropriate life cover in a ULIP plan is important to ensure that your family’s financial needs and long-term goals are adequately protected. The table below highlights key factors that can help determine the suitable life cover amount.

Factors To Decide | Example |

Current Income | At the current income level of ₹5 lakh per annum, you may consider opting for a life cover that provides coverage of around ₹1 crore |

Age | If your age is between 20 and 30 years, buy a life insurance cover of around 15 times your annual income, while if you are between 45 and 55 years, a life insurance cover of around 10 times your annual income can be considered |

Financial Liability | Ensure your life insurance is sufficient to cover your financial liabilities, such as outstanding debts, mortgages, and education loans |

Inflation Rate | In 15 years, at a 7% inflation rate, the value of ₹1 crore may reduce significantly, equivalent to about ₹33 lakh in present terms |

Life Goals | Identify your long-term financial goals, such as your child’s education, marriage, or maintaining your family’s lifestyle while deciding on your life insurance coverage |

Riders Available With ULIP Plans?

ULIP offers a range of additional riders that can be added to your policy to enhance its coverage and benefits. These riders are supplementary benefits that allow you to customise your ULIP plan according to your specific needs and financial goals. Here's an overview of the most common riders available with ULIP:

- Accidental Death Benefit Rider: This rider provides an additional sum assured in case of the policyholder’s death due to an accident. It enhances the death benefit and helps provide additional financial support to the nominee if the death occurs in unforeseen circumstances. The accidental dealth benefit rider is especially valuable for individuals who are at higher risk due to their occupation or lifestyle.

- Critical Illness Rider: A critical illness rider provides a lump sum benefit if the policyholder is diagnosed with a major illness such as cancer, heart attack, stroke, or kidney failure, among others as specified in the policy terms. This rider helps manage medical expenses related to treatment and can be a crucial addition for individuals looking to strengthen their financial protection against serious health conditions.

- Waiver of Premium Rider: In case of disability or critical illness, this rider waives the future premiums on the ULIP, ensuring that the policy remains active even if the policyholder is unable to pay premiums due to unforeseen circumstances. This rider guarantees that coverage and benefits will continue uninterrupted, even during financial hardships resulting from illness or injury.

- Income Benefit Rider: This rider provides a regular income support to the policyholder’s family/nominee in case of their untimely death. Instead of only a lump sum payout, the beneficiary receives periodic monthly payments, which can be beneficial for families looking for ongoing financial support.

- Total and Permanent Disability Rider: This rider ensures that if the policyholder becomes totally and permanently disabled, the insurance company will provide a financial benefit, which may be in the form of a lump sum payout or periodic income depending on the policy terms. The disability benefit helps policyholders maintain financial stability and support their families in case of a life-altering disability.

ULIP Myths: Demystified

There are several misconceptions surrounding ULIP plans. Understanding the facts behind these myths can help investors make more informed decisions about ULIP investments.

Myth 1: ULIP are Costly

ULIP plans had a heavy charge structure around 2008. However, the IRDAI intervened introduced regulatory changes, the cost of ULIP has reduced significantly over the years. If you are refraining from investing in ULIP due to the high cost, you don’t have to worry now.

Myth 2: ULIP is a Risky Investment Option

Under ULIP, investors are allowed to choose funds based on their risk appetite. ULIP come with several fund options, such as debt and liquid funds for low-risk investors, while equity funds for high and moderate risk investors.

Myth 3: Lock-in Period of 3 years

Earlier, the lock-in period for ULIP was three years. However, after 2010, IRDAI revised the guidelines, extending the lock-in period to five years. Now, ULIPs have a mandatory lock-in period of five years.

Myth 4: ULIP Does not Offer Flexibility

ULIP plans offer considerable flexibility to the investors. It provides the flexibility to switch between funds based changing market conditions or risk appetite. It also gives you the flexibility to partially withdraw money from your accumulated Fund Value before the policy matures.

Myth 5: Not a Good Option

ULIP plans combine life insurance protection with market-linked investments, making them a possible option for individuals looking to address both protection and long-term investment needs.

Myth 6: ULIP Provide Low Returns

ULIP plans offer the highest returns compared to other investment options if you choose wisely. It is one of the best investment options if you want to gain higher returns to fulfil your long-term goals.

Myth 7: ULIPs are Restrictive

This is not entirely accurate. There are no restrictions on exiting the ULIP plan. You can discontinue a ULIP at any time. If you decide to exit from the ULIP after the lock-in period, you can do so without paying any charges. However, surrender charges apply if you decide to exit before the lock-in period is over; you will be required to pay surrender charges.

Myth 8: Health and Accident Cover is not Provided in ULIP

This statement is also misleading. Apart from providing you with the dual benefits of investment and insurance in a single plan, ULIP also offers riders. You can receive additional protections, such as accidental death benefit or waiver of premium in the form of riders. ULIP also provides a partial withdrawal facility that can help you in times of emergency.

Unit Linked Insurance Plan Frequently Asked Questions

ULIP full form is Unit Linked Insurance Plan. It is a type of life insurance product that combines investment and insurance benefits in a single policy. A portion of the premium provides life cover, while the remaining amount is invested in market-linked funds such as equity, debt, or balanced funds, depending on the policyholder’s risk appetite.

A ULIP policy is a Unit Linked Insurance Plan that combines life insurance coverage with market-linked investment opportunities. In a ULIP policy, a portion of the premium provides life cover, while the remaining amount is invested in different funds such as equity, debt, or balanced funds, depending on the policyholder’s risk appetite and financial goals. The returns from the investment component depend on the performance of the selected funds in the market.

ULIP plans include certain charges for managing the policy and investments. Common charges include premium allocation charges, fund management charges, mortality charges, policy administration charges, and switching charges. However, some plans such as Canara HSBC Life Insurance Promise4Growth Plus have zero premium allocation charges, which can help maximise the invested amount. These charges are disclosed upfront and regulated by IRDAI guidelines.

The best ULIP plan in India depends on your investment goals, risk appetite, and protection needs. Some of the notable ULIP plans offered by Canara HSBC Life Insurance include:

Canara HSBC Life Insurance Promise4Growth Plus: Designed for investors seeking flexible portfolio management and balanced wealth creation with life protection

Canara HSBC Life Insurance SecureInvest: Suitable for individuals looking for high life cover with loyalty additions and long-term wealth accumulation benefits

Canara HSBC Life Insurance Wealth Edge: Ideal for investors aiming for equity-driven wealth creation with multiple fund options, portfolio strategies, and long-term growth enhancers

Each of these ULIP plans combines life insurance coverage with market-linked investment options, helping policyholders work towards long-term financial goals while maintaining insurance protection.

In order to understand ULIP NAV, you first need to understand how ULIPs work. In ULIP insurance plans, a portion of the premium from different investors is accumulated to create a single investment corpus. This money is invested in several different market instruments. To properly allocate returns among all investors, the fund manager divides the Net Asset Value (NAV) into small units with a specific face value. NAV is the per-market share value of a fund. To better understand the definition of NAV, take a look at the formula below -

Net Asset Value (NAV) = [Assets - (Liabilities + Expenses)] / Outstanding Units

The main difference between ULIP, SIP, and mutual funds is that ULIP (Unit Linked Insurance Plan) combines life insurance coverage with market-linked investment, whereas SIP and mutual funds are primarily investment-focused instruments. In SIP, (Systematic Investment Plan), investors contribute a fixed amount at regular intervals into a mutual fund scheme. This disciplined investment approach helps manage market volatility and supports long-term wealth creation.

mutual fund is an investment vehicle that pools money from multiple investors and invests it in equities, debt, or other securities, depending on the fund type. Mutual funds do not provide life insurance coverage.

ULIP, on the other hand, allows you to invest in market-linked funds such as equity, debt, or balanced funds while also providing life insurance protection. This makes ULIP suitable for individuals looking to combine investment growth with financial protection for their family.

Basis | ULIP | Traditional Plans |

Meaning | A financial product that gives you the benefits of both investment and insurance in a single plan | A type of plan that is characterised by guaranteed returns and lower investment risk |

Funds | You can choose to invest in both equity and debt based on your risk appetite | The funds involved are mostly debt |

Charges | Includes various charges such as premium allocation, fund management, and surrender charges | Usually involves relatively fewer charges |

Transparency | Offers higher transparency, with disclosure of charges and the ability to track fund performance | Lower transparency with limited visibility into investment performance |

Lock-in period | 5-years mandatory lock-in period | Generally no lock-in period, though withdrawals may depend on policy terms |

Withdrawal | Partial withdrawals are allowed after the lock-in period | Withdrawals are generally restricted before maturity |

Switching | Allows switching between funds based on investment preference | Fund switching is typically not allowed |

The following are the benefits of Unit Linked Investment Plan:

Tax Benefits: ULIP plans may help reduce tax liability, as premiums paid towards the policy may qualify for deductions under Section 80C of the Income Tax Act, subject to applicable conditions

Long-term Growth: One of the major benefits of buying a ULIP plan is that it supports long-term investment goals. ULIP plans come with a lock-in period of five years, which encourages long-term investing

Dual Benefits: ULIP plans not only offer life insurance coverage but also provide market-linked investment options. These include equity funds, debt funds, or balanced funds, allowing investors to choose funds based on their risk appetite and financial goals

Flexibility: ULIPs offer flexibility to switch between different funds based on changing risk appetite or market conditions. Investors may also choose multiple funds and different investment strategies

Partial Withdrawal Option: ULIP plans allow partial withdrawals in case of financial needs or emergencies, after the completion of the mandatory lock-in period

If you want to enjoy the combined benefits of life insurance, market-linked investment, and potential tax advantages, you may consider investing in a ULIP plan. ULIPs combine protection and investment within a single policy, helping individuals work towards long-term financial goals.

In a ULIP, the premium paid towards the policy is generally divided into two components, life insurance coverage and market-linked investment. Therefore, an individual investing in such a plan may benefit from investment growth potential while also receiving life insurance protection.

ULIPs are life insurance products that also offer investment opportunities. Like other market-linked investment options, there is no guaranteed return in a ULIP. If you are comfortable taking higher risks and want to potentially earn higher returns, then you may consider opting for equity funds.

Generally, the minimum lock-in period for a ULIP is five consecutive policy years. During this time period, if the policyholder discontinues or surrenders the policy, then they will not receive any payouts immediately. Withdrawals are only allowed after the completion of the lock-in period. In addition to this, if you surrender your policy before the lock-in period ends, then you will have to pay surrender charges as well. Also, it is advisable to remain invested even after the completion of the five-year lock-in period, because if you stay invested for a longer duration, it may help you achieve better long-term benefits

ULIP is considered a suitable investment option if you are looking for long-term wealth creation. It could be buying your own house, a new car, going on a long vacation, or your child’s higher education or marriage. ULIP plans can help you work towards long-term financial goals. Moreover, ULIPs come with a lock-in period of five years, which keeps you invested for a longer period and encourages long-term investing. The lock-in period is calculated from the date when the policy is issued.

The right time to invest in a the ULIP is as early as possible, especially when you begin planning your long-term financial goals. Starting early allows your investment more time to benefit from market growth and compounding, while also helping you secure life insurance protection for a longer duration.

At the time of maturity of a ULIP policy, you will receive the fund value based on the prevailing NAV. The fund value is calculated by multiplying the total number of units held under the policy by the Net Asset Value (NAV).

Fund Value = Total units of the policy × NAV (Net Asset Value)

If the payment of premiums for a ULIP policy is discontinued during the lock-in period, the policy may move to a discontinued policy status, and the fund value after applicable charges may be transferred to a discontinued policy fund. The proceeds are generally payable after the completion of the lock-in period, as per policy terms.

If the premium payment is discontinued after the lock-in period, the policyholder may have options such as continuing the policy with the existing fund value or surrendering the policy, depending on the policy conditions.

A ULIP plan is a combination of investment and insurance. Thus, one must ideally hold this plan for a duration of at least 10 years to maximise the potential investment benefits. An early exit may affect the overall investment outcome. ULIPs have a lock-in period of five years. Thus, you may surrender your policy before the completion of 5 years, but proceeds will generally be payable only after the five-year lock-in period,.

Investing in a ULIP may involve market-linked risks, as the returns depend on the performance of the underlying funds. The level of risk in a ULIP largely depends on the investment option you choose. If you are not comfortable with sharp market movements, then choosing lower-risk options such as debt funds may be suitable. For people with a higher risk appetite, equity funds may offer higher growth potential, while risk-averse investors may prefer debt-oriented funds.

Yes, ULIP do offer tax benefits. Under the Income Tax Act, 1961, the premium paid towards ULIP is allowed a tax deduction of up to ₹1.5 lakh under section 80C, subject to applicable conditions. In addition, the maturity and death benefits may be tax-exempt under Section 10(10D), as per prevailing tax laws.

You can withdraw from a ULIP after the completion of the initial lock-in period, which is generally 5 years. Some plans allow a limited number of free withdrawals after which charges may apply, while certain plans may offer unlimited withdrawals as per policy terms.

If you want to withdraw before the lock-in period, the policy may be discontinued, and the proceeds will typically be payable only after the completion of the five-year lock-in period, subject to applicable policy charges.

Yes, you can cancel/surrender your ULIP plan. However, if the policy is surrendered before the completion of the lock-in period, discontinuance charges may apply. Surrendering the policy will also terminate the life cover provided under the plan. Therefore, it is generally advisable to evaluate the policy terms carefully before discontinuing the plan.

Popular Search

- What is ULIP?

- ULIP Tax Benefit

- ULIP Full Form

- ULIP Vs Term Insurance

- Best ULIP Plans

- Best ULIP Plan For Child

- Allocation Charges In ULIP

- ULIP Returns In 15 Years

- Difference Between ULIP and Mutual Fund

- ULIP Vs SIP

- Mortality Charges In ULIP

- What is NAV?

- How ULIP Works?

- Tips to Buy ULIPs

- ULIP Calculator

- Power of Compounding Calculator

- ULIP Tax Benefits in India