Written by : Knowledge Center Team

2026-07-29

1096 Views

7 minutes read

Share

You try to save the money you earn so that you can fulfil the present needs and achieve larger financial goals in future. But saving money is not enough, you need to invest the money and earn a good return on it.

It can be difficult to achieve long-term goals if you are not investing. Investing allows your money with the power of compounding so that your wealth grows with time.

ROI or return on investment is the rate of growth your invested money receives over a specific time.

For example, if you invest ₹100 and one year later receive ₹110, your money has grown 10% in one year. In other words, your ROI on ₹100 has been 10% per year.

ROI also measures the performance of the investment options.

For example, if you have two different places you can invest your savings in, ROI will help you decide quickly. Look at the ROI of both investments for the same period and you can invest for a higher rate of growth.

Thus, in the investment world ROI is a method to ascertain the profitability of your investment. You can use this metric to compare investments and choose a better one. ROI for a fixed income investment will tell you the return you can expect from the investment.

Gone are the days where you just used to have only 1-2 options to invest in. Now you have a huge range of investment products at your disposal.

Some popular investments are as follows:

Each investment has different features and thus offers different returns.

Thus, it becomes important to compare the investments so that you can choose the one which will be the best for you.

The following methods can be used to compare two investments together.

It is the simplest way to compare two investments. It helps you to determine in how much time your investment will be recovered.

For example, you have invested ₹1,00,000 and the return per year is ₹10,000 then PBP will be 1,00,000/10,000 = 10 years.

The money that you have today may not be worth as much a year later. The value of money today will be worth more than tomorrow. This is the time value of money.

Future Value= Present Value x (1+R)N

This is the extension of the concept of the time value of money. It expresses the present value of all the future cash flows that you will receive from your investment.

NPV= Rt / (1+ i)t

Where Rt is the value of cash flow at the time ‘t’ and ‘I’ is the discount rate.

This method allows you to evaluate multiple cashflows, coming in or going out, at different points in time.

It is a method in which the return is calculated excluding all the external factors, such as inflation rate, bank rate, etc.

Under this, the NPV is considered to be 0.

IRR = Ct / (1+ r)t- Co

All the above-stated methods of comparing the investments involve complexities. It can be confusing especially when you are just starting. Here is one more method which you can use.

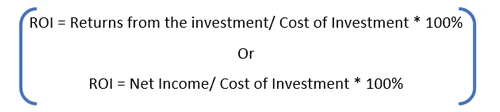

Return on Investment compares the incomes received from the investment with the cost of the investment.

Below is the formula for ROI:

Now that you know what is ROI, you must be wondering how to calculate it. Here we show you the steps you can follow to arrive at your investments Return on Investment.

Following the example, the ROI would be ₹29400/100000 * 100 = 29.4%

You don’t have to manually do these calculations. To ease your work, there are many calculators available online which can do the work for you.

For example, Canara HSBC Life insurance company has a Power of Compounding Calculator.

Enter details such as:

The site will show you in the graphical form your return.

Here we provide you ROI examples of two of the most common investments

Click here to use - Investment Calculator

Ajay buys a ULIP to get the benefits of both investment and insurance.

Bank FD is seen as the safest form of investment. In a Bank FD, you put lump sum money in your account for a fixed duration. At the end of the FD, you receive your original sum with the interest compounded.

For example, suppose the rate offered by the bank on Fixed Deposit is 6% per annum.

So if you invest ₹100, after one year you will receive ₹105.52.

Using these ROI estimation ways, you can now evaluate different investment options before investing. However, do keep in mind that most of these investments are bound to the market scenarios as well. Thus, looking only at ROI is akin to looking only at one side of the coin.

Better have a look at the market conditions as well before concluding.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.