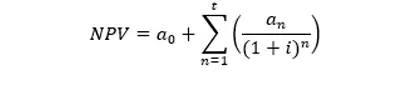

Alternatives to NPV

NPV estimates the value of your project relative to another project (or investment) with similar value. However, NPV is not an all-pervasive method of investment evaluation.

Some alternative methods to NPV are:

Payback Period:

The payback method is a viable alternative to NPV and calculates how long it will take for you to recover your money. The formula is simple to remember and calculate. You need the initial investment and the net annual cash flow to calculate the payback period.

The formula for calculating the payback period is:

Payback Period = (Initial Investment / Average Annual Cash Inflow)

The payback method helps quickly evaluate projects and reduce the risk of losses. A project with a short payback period is efficient and improves liquidity. It implies that the project is less risky and more helpful for small enterprises with limited resources. A shorter payback period also reduces the risk of losses from economic changes.

Internal Rate of Return (IRR):

The IRR is the discount rate at which the NPV of all cash flows from a project or investment becomes zero. In other words, it is the break-even rate of return. The IRR method is used to evaluate and compare projects of different time horizons based on their projected rates of return.

For example, when comparing the projected profitability of a 3-year and a 10-year project. NPV calculates the total amount of money you will make in an investment, factoring in the time value of money. In IRR, you calculate the annual rate of return that you would earn. A higher IRR relative to the cost of capital generally indicates a more attractive investment.

The formula for calculating IRR is:

0 = NPV = Σ Ct / (1 + IRR)t − C0

Where:

Ct = net cash inflow during period t

C0 = total initial investment cost

t = number of time periods