Written by : Knowledge Centre Team

2025-10-02

2916 Views

8 minutes read

Share

And before we dive into these amazing concepts let’s recall a few old age wisdom nuggets which hold even in modern times:

Retirement may feel like a distant milestone, especially when you're busy building your career or managing family responsibilities. However, the truth is that your future comfort depends on the choices you make today. And the sooner you start planning, the more freedom and peace of mind you’ll enjoy later in life.

Key Takeaways

|

You don’t need to be a financial expert to secure your golden years. What you do need is a firm grasp of a few timeless principles, concepts that are easy to understand and powerful enough to guide your retirement journey from your first paycheck to your last.

And before we dive into these concepts, let’s recall a few old-age wisdom nuggets that still hold true:

Retirement is ultimately just another financial goal. Like any other goal, it’s about managing your expenses and increasing your savings to make the most of your income.

These principles will recur throughout the retirement concepts outlined below.

Nowadays, ‘early retirement’ is quite a buzzword among Gen-Y. However, what does early retirement mean?

If retiring, for you, means relying solely on your savings to sustain your lifestyle, you may soon face challenges for the following reasons:

Thus, early retirement should mean that you will start working on something closer to your heart. Starting a business enterprise and making it profitable has been one of the popular early retirement plans.

Use plans which will do both of the above automatically for you, a few examples are, Tier-I account of New Pension Scheme, pension plans from life insurers, and online ULIP plans.

Best online ULIP plans have the features to allow you to not only invest in good equity funds but also, manage your portfolio with proven strategies. ULIPs from Canara HSBC Life can easily double up as your tax-free retirement plan in India.

For example, you receive an increment of 10% on your annual income. First, before heading to the party, increase all your investments by at least 10%.

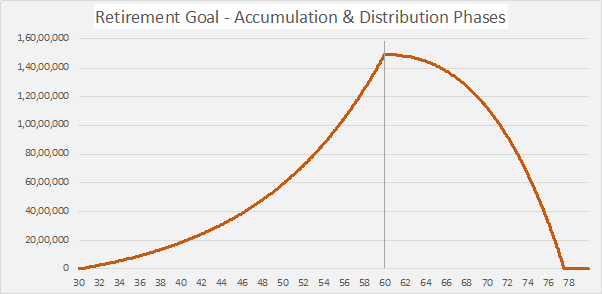

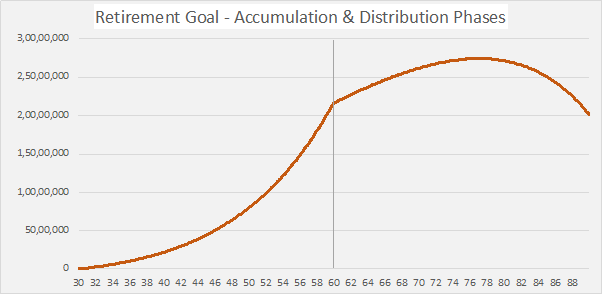

In the first chart of the accumulation and distribution phase, we maintained a monthly investment of ₹10,000 for the entire period. The result was that the corpus did not even last for the next 20 years.

However, if you increase your savings by just ₹500 a month each year, you get enough corpus to last more than 30 years. Not only that, but you can also leave a significant legacy for your children.

Withdrawals are the same in both estimates and are growing at the same rate each year.

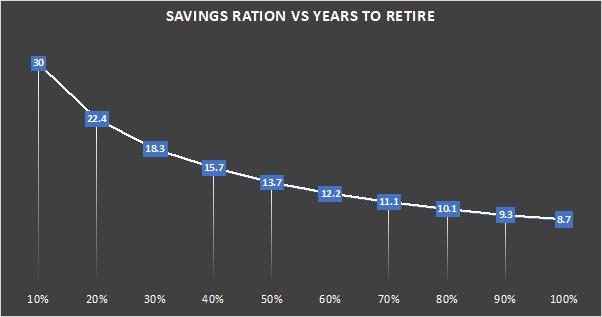

For example, if you are earning ₹1 lakh a month, and save 10% of your income towards retirement, you can replicate the same income within 30 years.

Similarly, Image 3 gives you more years to retirement based on other savings ratios. The rate of return of the investment plays a role in these estimates, and we have assumed 8% p.a. ROI for our calculation.

You have known that ‘the more you save, the faster you will achieve your financial goal,’ but this image should solidify your knowledge into a firm belief with numbers.

PS, if you save 90% of your income, you can have enough money to replicate the same within the next 10 years.

You figure out which are the possible major expenses post-retirement and you take measures to minimise them. For now, these could be the most common major expenses on most post-retirement budgeting sheets:

So, taking care of your health will possibly resolve at least two of these. However, you should also keep the senior citizen health insurance handy, just in case the uninvited concern knocks on your door. For home maintenance, moving to a more manageable property could be recommended. But, there could be so many more solutions.

Now that we've explored the five key concepts of retirement planning, one important question remains: When should you actually begin your retirement journey? Let us find out.

The short answer? As early as possible. The best time to start planning for retirement is with your first job or first steady income. The earlier you begin, the more powerful your money becomes, thanks to the compounding effect.

Ideal Ages and Milestones to Begin

Let’s look at a simple example:

Assuming a 10% annual return:

Why the gap? Because compounding rewards time more than amount. The earlier you start, the more your money multiplies, without extra effort.

If early retirement is your goal, say at 50 or even 45, you’ll have fewer working years to save and more non-working years to fund. This means:

Starting in your early 20s or as soon as possible helps build that cushion, giving you options later, such as retiring, switching careers, travelling, or simply slowing down without financial anxiety.

A retirement planning calculator is a simple tool that gives you an idea of the corpus you can accumulate with a regular monthly investment for your golden years.

The above calculation and illustration of figures are indicative only and not on actual basis.

While starting early gives you a strong head start, staying consistent over the long haul is what truly builds a secure retirement. After all, even the best-laid plans can fall apart without the right mindset and discipline. That’s where behavioural habits bridge the gap between intention and action.

Retirement planning is not a one-time decision but a lifelong habit. Here are a few practical ways to stay on track:

These small habits can make a big difference over the decades.

Retirement is a stage of life that requires deliberate planning, disciplined execution, and consistent care. Through this guide, we’ve uncovered the core concepts that can help anyone, regardless of income or financial background, take control of their retirement journey.

From understanding how early retirement affects your savings to tackling inflation and aligning your savings with your income growth, these concepts are more than just financial advice; they’re building blocks for a future you can look forward to.

But knowledge alone isn’t enough. The key lies in starting early, staying consistent, and being mindful of how you approach money over time. With simple habits like automating your savings, avoiding emotional investing, and reviewing your plan annually, you can set yourself up for a retirement that’s not just financially secure but also fulfilling and stress-free.

Remember, the best retirement plan is one that’s rooted in clarity, discipline, and action. To make that journey easier, retirement solutions from Canara HSBC Life Insurance offer tailored plans designed to help you build a reliable income stream and secure the lifestyle you envision. Start where you are, use what you have, and build steadily, because when the time comes to retire, your future self will thank you for the steps you took today.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.