Written by : Knowledge Center Team

2025-12-16

1116 Views

7 minutes read

Share

Retirement is an inevitable phaseof life. There comes a time when you want to call it quits and just enjoy the fruits of all the hard work you did. Post your retirement, you don’t have to worry about getting up on time and deciding which work you have to do today. Instead, now you decide which destination you want to go to and enjoy. Which journey do you want to embark upon?

You finally have ample time to take up the hobbies you have neglected due to work, or even start a new one. You can finally visit a place that you have always wanted to visit, read a book that you haven’t, or just chill and spend some quality time with your grandchildren.

But though now you have time to do all these things, do you have the resources? Another limitation of retiring is that now your corpus cannot change. Are your finances enough that you can enjoy these things? Do you have the right retirement and pension plan? This is a challenge that everyone faces.

Here are five important signs that can tell that you are not financially ok to retire.

Key Takeaways

|

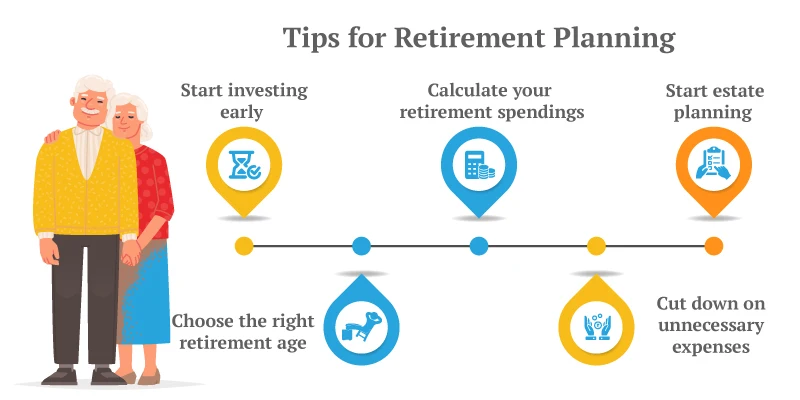

The basic mantra of leading a good post-retirement life is to save enough that you don’t need to struggle afterwards. But if your savings are not enough to get you through, then you have to wait a little bit more to finally retire.

The best way to keep track of your retirement savings is to use a retirement calculator every once in a while. The calculator will give you the estimated retirement corpus or the monthly savings amount you need to maintain to achieve your retirement corpus.

Having a good retirement corpus is vital for your life. Savings play a huge role in building your retirement corpus. So you must have a perfect savings plan that makes you enough to lead a stress-free life.

So you should work for a few more years. Along with working, you should also change your habits and try to save more so that your retirement corpus increases.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Retiring without a specific plan in your mind is maybe not the best idea. As said above, after retirement, you only have a fixed amount of money with you. You need to have a long-term view of whether you can sustain this corpus or not. You need to know how much money will be enough for you. Though it is not an easy task, doing this will surely help you.

You need to ask yourself some questions, such as whether your goals are fulfilled and whether your savings are enough that you can stop working. After this, you need to create a proper budget.

The importance of a proper retirement plan cannot be underestimated. To make a successful post-retirement plan, you need to start estimating the income as well as the expenses you may have. Though it is extremely difficult to know what you will be spending your money on after retirement, still having a rough figure in your mind will certainly help you build a basic plan.

If you have taken out any loans and there is still time to pay them off, then you may consider these two options:

Work for some more years till the debt has been paid

Pay the loan in a lump sum

Paying off loans before retiring will save you the burden of monthly payments later. Paying off all debts before retiring will also help in keeping your long-term finances untouched. You wouldn’t want your monthly payments to keep eating into your savings, money that could otherwise be used to meet essential expenses

If you don’t want to work more and then you can also pay your loans up-front, provided you have enough money saved with you.

There are a few major financial goals that you would certainly like to achieve in your life. Buying a house, marrying your child off are some of the major goals to look forward to. You would not want to retire before these major goals are fulfilled.

You should also provide for big expenses such as buying a new car or repairing your home in your retirement corpus. If possible, try to see these through while you can still work. Thus, it will reduce the amount you plan to use for your daily needs. That is why you should start financial planning and budgeting.

Post-retirement income is roughly 50 per cent of your last salary. Having expenses as much as income will pose trouble after retirement. To tackle this, the golden rule of managing finances should be followed. Spend less than you earn. Though it is obvious, it is very hard to follow.

Two things can be done to manage this situation

Lower your daily expenses

Build your corpus

One example that could certainly curb your expenses is moving to a lower-tier city. Many people move to a different city after retirement to save costs. Moving to a new city which has lower costs will help you in two ways:

Lower daily expenses

Lower homeownership cost vs the present house

Besides, if you don’t want to sell, then you could let it out for rent and have another source of passive income. Having this kind of income is a huge plus.

| Sign | What It Means | What You Can Do |

|---|---|---|

1. Savings Are Low | You haven’t saved enough to sustain your retirement lifestyle. | Use a retirement calculator to track how much more you need. Rework your budget and savings plan. |

2. No Post-Retirement Plan | You lack a financial roadmap for how to manage income, expenses, and goals after retirement. | Estimate your future expenses, set clear goals, and plan for emergencies. Consider guaranteed income sources like annuity or pension plans. |

3. Ongoing Loans | Unpaid home, personal, or car loans can strain your limited retirement corpus. | Repay major loans before retirement. Avoid drawing from savings to meet EMIs. |

4. Pending Financial Goals | Milestones like your child’s education or marriage are still unfunded. | Try to meet these goals while still working. Avoid dipping into your retirement fund for these obligations. |

5. High Daily Expenses | Your current cost of living may be too high to manage post-retirement, especially if it matches or exceeds your income. | Consider downsizing, moving to a lower-cost city, or creating passive income sources like renting out property or investing in retirement-oriented plans. |

Having robust life insurance and retirement plans in place can eliminate most of these obstacles:

Life Insurance (like Term or Endowment Plans): Ensures your family remains financially stable in your absence and helps meet long-term goals.

Retirement Plans (like Pension or Annuity Plans): Guarantee a steady income stream even after you stop working.

At Canara HSBC Life Insurance, our retirement solutions are built with flexibility, guaranteed income options, and tax-saving benefits, so you can retire not just early, but confidently.

Retirement without planning is like driving a car without a destination in mind, that is, aimless. Therefore, it is crucial to have a well-defined financial plan in place that targets a stress-free retirement. Make sure you have a good savings by your side, and all your goals are laid out. Look for a good life insurance plan that will not only help you save but will provide you with a good sum of money once you retire.

At Canara HSBC Life Insurance, we understand that retirement is not just a phase but a reward for years of hard work. That’s why our retirement plans are designed to help you enjoy financial freedom and live life on your terms. With flexible options, guaranteed lifelong income, and tax benefits, our plans ensure that you step into your golden years with confidence, dignity, and security.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.