Written by : Knowledge Centre Team

2026-02-03

1114 Views

8 minutes read

Share

Retirement planning in India has evolved. What worked a decade ago, real estate, FDs, gold, EPF and a regular insurance plan may no longer be enough. However, rising life expectancy and healthcare costs, and lower returns from traditional instruments to generate wealth, retirement is reshaping how we plan for life after work.

The average life expectancy in India is now around 73.4 years, and with access to good healthcare, you can easily live up to 80 years of age. If you retire at the age of 60, your savings need to last at least 20 years, often more.

Key Takeaways

|

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Whether you want to retire early or wait till 60 years of age, it’s up to you. But then, it also depends on your financial goals and liabilities. Most millennials today want to retire at the age of 50. In that case, you must have substantial retirement savings that can sustain you and help you lead a comfortable retirement life for the next 30 years,; assuming that you live up to 80 years.

Here are some key factors to consider while deciding on your retirement age:

Choosing the right age is the first and most important step because it determines how long you have to save and how long your savings need to last.

Once you decide on your retirement age, you need to arrive at a figure that accurately estimates your retirement corpus. To do that, you must estimate your life expectancy based on your age, medical condition, family history and other factors.

The table below is a ready reckoner for estimating your average life expectancy based on your current age, according to World Life Expectancy.

Current Age | Estimated Remaining Life Expectancy | Expected Age at Death |

0 (during the birth) | ~72.5 years total life span | - |

30 | +~45 more years ≈ 75 total | ~75 |

50 | +~25 more years ≈ 75 total | ~75 |

60 | +~15 more years ≈ 75 total | ~75 |

According to the table, if you are a 30-year-old, your average life expectancy is 75 years. Therefore, if you have decided to retire at the age of 50, you need to have enough retirement savings to last you at least 25 years post-retirement. This will help you calculate the size of your retirement corpus.

Calculating the correct retirement corpus is the moment of truth in retirement planning. You have to keep many factors in mind, and there are chances of miscalculation. Of course, you cannot reach the exact amount, but you should be able to reach a ballpark figure.

To avoid any shortfall in reaching your ideal retirement fund size, you need to keep a few factors in mind, such as inflation, current age, medical condition, current liabilities, retirement age and current monthly expenses.

The best way to calculate your ideal retirement corpus is to take your current monthly expenses and multiply them by your retirement age, while keeping an average inflation rate in mind.

For example, if your current age is 30 years and monthly expenses are ₹50,000, it will rise to ₹1,06,000 per month by the time you reach the age of 50, assuming that the inflation rate will remain at 4.6%. Therefore, if you want to retire at the age of 50, you need to save for another 30 years. According to the calculation, you need to have a retirement corpus of more than ₹3 crore to meet your monthly expenses for 30 years (₹.1,06,000 x 30 years).

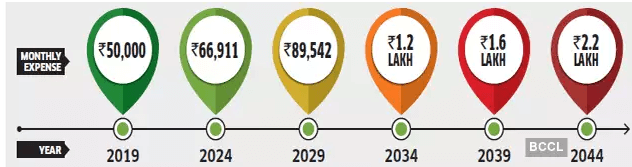

This table demonstrates how your current monthly expense can multiply over time due to inflation. Assuming a steady 4.6% annual inflation rate, here’s how ₹50,000 in 2025 grows across the years:

This clearly highlights why retirement planning must account for inflation. What seems adequate today may fall short tomorrow. To maintain your current lifestyle post-retirement, your corpus must grow enough to match these rising costs.

Once you retire, you will still need regular income to meet your monthly expenses. Therefore, it is a must to invest in a pension plan or annuity plan post retirement. To achieve your ideal retirement savings goal, you need to start saving early and choose the right investment instrument.

Unit-linked insurance plans (ULIPs) allow you to have a robust retirement plan as they provides the triple benefit of insurance protection, wealth generation and tax savings. It is vital to remember that there are a few factors that can erode your retirement fund; that is, inflation and tax. Therefore, when you start retirement planning, choose an investment tool that provides inflation-beating returns and gets you maximum tax benefits.

ULIPs have consistently provided returns in the range of 9-12% and they are the most tax-effective investment instruments available in India. Start investing for a comfortable retirement life with ULIP options by Canara HSBC Life Insurance.

Retirement planning might seem overwhelming at first, but breaking it down into simple steps can make a big difference. Knowing when you want to retire, estimating how long your savings need to last, and accounting for rising costs, these are all crucial. The earlier you start, the easier it gets to build a comfortable, stress-free life after work. A little planning today can go a long way in shaping the life you want tomorrow.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.