Written by : Knowledge Centre Team

2026-01-28

1297 Views

8 minutes read

Share

Retirement is a long-term goal. It is not a one-time decision. A lot of thought has to be given to the decision of retiring. It is to achieve the milestone of retirement that you work hard and try to accumulate wealth.

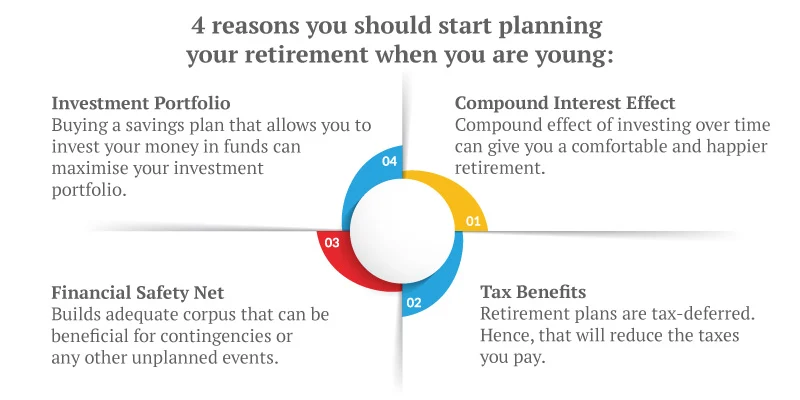

Thus, planning for retirement becomes an essential part of your work life. It has to be done more thoughtfully if you are planning to retire early. However, before you do the planning part, let’s take a closer look at the pros and cons of early retirement.

Key Takeaways

|

Early retirement, unlike other financial goals in life, is a choice with associated advantages and disadvantages. Why would you want to retire early? And why you shouldn’t? Knowing answers to both questions will help you decide with a little more clarity:

Now that we have taken a look at the advantages of retiring early, this is not always the case. Early retirement has its fair share of challenges as well.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Now, the golden question, ‘how do we overcome these challenges?’

Many worry about outliving their savings or being unprepared for unexpected expenses like health emergencies when they retire early. Well, the ground reality is that the earlier you plan to retire, the more you need to plan every financial move. You must ensure that your money lasts longer, grows steadily, and is protected from risks such as inflation or taxes.

The following are some practical ways to prepare for and overcome the hurdles of early retirement:

The maturity amounts you receive are also tax-free under u/s 10(10) D of the Income Tax Act 1961. In addition to the maturity amount, the sum assured received by the family in case of the policyholder’s unfortunate demise is also tax-exempt. This means that they are not required to pay any taxes on this amount.

There are different tax-saving plans. When it comes to ULIPs (unit-linked insurance plans), their three-fold benefits can fulfill your dream of building an early retirement corpus. Here’s what they offer:

Early retirement is a rewarding goal, but it demands careful planning, consistent saving, and informed investment. You need to choose options that offer good returns, allow flexible access, and also help you manage risk over time. In fact, you must also ensure whether or not they include deductions u/s 80C and 10(10)D of the Income Tax Act.

With features such as wealth boosters, fund switching, partial withdrawal, tax-saving, and auto-rebalancing, savings plans by Canara HSBC Life Insurance offer the flexibility and growth needed to build a strong early retirement corpus. Start your savings with Canara HSBC Life Insurance to plan for an early retirement with confidence today.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.