Written by : Knowledge Centre Team

2025-10-01

3965 Views

8 minutes read

Share

There are different ways to look at money. You can make the most of the money you have if you understand the time value of money. The value of money is its purchasing power. What money can buy depends on the price level of the item. When the price increases, you can purchase less of it with the same money.

Key Takeaways

|

A decade back, with ₹ 10,000, you could have bought all your monthly groceries, but today for the same groceries, you may be spending ₹ 15,000. It means the value of money has been reduced. You will need even more for your monthly groceries in the coming years.

Assume you have lent ₹ 50,000 to your friend who has committed to paying you after a week. However, a week later, he calls you and informs you that he won't be able to return the money for the next three months. However, he assures you that he will return the complete sum in three months.

For a layman, the assurance may bring relief. However, if you understand the time value of money, you may not be satisfied with this response.

According to the Time Value of Money, the money you have in hand today is worth more than the same amount you will have in the future. In the above example, the worth of your loaned money is lower after three months. So even though you will receive the whole money, you are at a loss.

Since money can generate interest, the value of money is less if you receive it in the future. There are two reasons for it:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

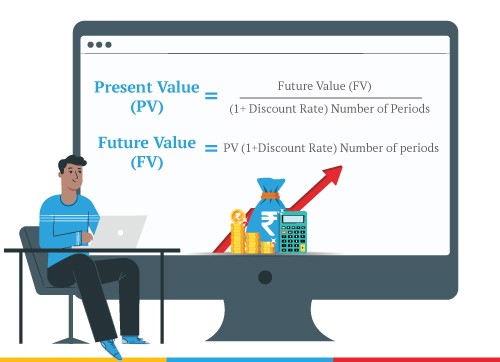

Let us closely look at what the present and future value of money means.

Example: If you invest ₹ 1 lakh in a fixed deposit at 6% interest for one year, the future value will be ₹ 1.06 lakh.

You need to understand how TVM in different instruments works. It will help you make the correct investment. Along with future value, you should also consider taxation when choosing your investments. TVM is calculated using the following formula:

FV = PV x [ 1 + (I/ N) ]^(N*T)

Here, FV is the future value, PV is the present value, N is the number of compounding years, and T is the investment tenure.

For example, If you invest ₹ 10,000 (PV) for 10 (T) years at an 8% (I) p.a. rate of interest, you will receive ₹ 21,589.25 (FV) on maturity.

Using the above formula, FV will be ₹ 161,051. Since you are taxed at 30%, your net gain will be ₹ 42,736 only.

However, the time value of money for your investments will vary based on your investment horizon, mode of investing and withdrawal. You can estimate your real return after withdrawing the money.

Mutual fund returns are taxed as capital gains only after withdrawal. So, you can easily establish the impact of taxation on your returns.

ULIP ROI is a weighted average of individual funds’ ROIs. Since ULIP returns can be completely exempt from tax, your ROI can be free from the tax effect.

Like mutual funds, you can estimate the real ULIP ROI for your portfolio at the time of withdrawal.

Based on the discussion, it is clear that you are better off if you can earn more on your investments - you can maximise TVM for your investment. Below are a few things you can do to maximise TVM for your investments:

Disclaimer: Tax benefits are subject to change in tax laws. Please consult your tax advisor.

Below are some of the best EEE investment options you can explore:

Understanding the time value of money is crucial, as it helps you recognise that the value of money today is higher than its value in the future. This awareness should guide all your financial decisions, encouraging you to maximise after-tax returns to preserve and grow the real value of your investments. To achieve this, it's important to align each investment with a specific goal and avoid premature withdrawals that can interrupt compounding. By focusing on tax-efficient instruments, you not only retain more of your earnings but also create space to explore market-linked options that help beat inflation.

As your life goals and risk tolerance evolve, regularly reviewing your portfolio ensures that your investments remain relevant and effective. Ultimately, discipline, consistency, and patience are the threads that tie together a resilient and rewarding financial journey. To support this journey, savings and investment plans from Canara HSBC Life Insurance offer a smart blend of protection and wealth-building strategies, tailored to your long-term goals.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.