Written by : Knowledge Centre Team

2025-12-12

6907 Views

15 minutes read

Share

Savings have been a habitual thing for Indian investors. Hundreds of investments in India try to channel these savings to the greater good. Much like the investors themselves and their unique financial needs, the investments in India also branch into various types.

Each of these saving and investment plans carries returns and risks, which are directly proportional to each other. In other words, the higher the risk involved, the better the chances of returns. When discussing investment options in India, we can broadly categorise the available types of investments into two categories: financial and non-financial.

On one hand, fixed-income products, such as Public Provident Fund (PPF) and Bank Fixed Deposits (FDs). To help you build an investment plan that matches your risk profile and investment needs with its potential to gain profitable returns, here is an insight into the different types of investment options in India.

So, if you are looking for the best investment options in India, you simply need to match the benefits of the investment plan with your needs.

Key Takeaways

|

As the name suggests, investment plans are financial instruments which help you create sustainable wealth for your future needs. There are various investment plans available nowadays that enable you to invest your savings systematically into different money-market products and help achieve your financial goals. These investment plans offer the much-desired advantage of creating wealth through disciplined, long-term investments. Some of the most popular investment options today are:

Unit Linked Insurance Plans (ULIPs)

Public Provident Funds (PPF)

Monthly Income Plans

Senior Citizen Savings Scheme (SCSS)

Tax-saving Fixed Deposits

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

You can classify investments in India into several categories based on their risk profile, investment tenure and taxability. The following are the 12 most popular types of investment options in India:

Coupon / Interest Payments

Capital gains/losse

Unlike equity stocks, bonds have limited tenure. Firms may also issue debentures with a conversion option to equity stocks for the investors. Bonds and debenture investments in India are low to high-risk investments.

You can access the investment risk of a bond issue through its credit rating. The least risky bond issues will have a rating of ‘AAA’, while ‘BBB’ and ‘C’ will be higher risk.

Real estate investments will offer a return on your investment in the following two ways:

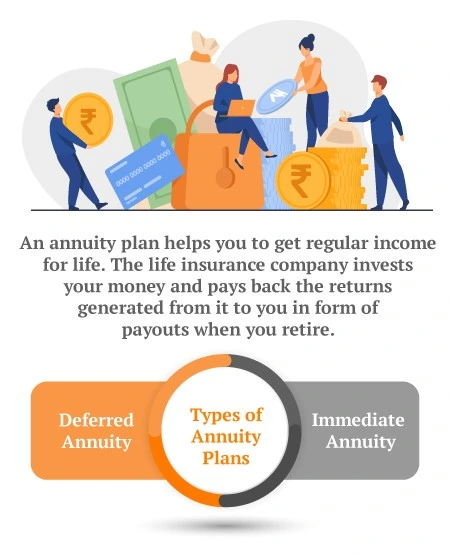

An immediate Annuity is the best investment plan in India to start a regular income within one month of investment. However, if you want to start the income after a few years, you can invest in deferred annuity options.

Deferred annuities provide a growth period for your corpus or regular investments before drawing income.

While bank investment options in India are full of fixed income and safe investments, they also offer investments in alternative assets. Bank’s customised portfolio management services let you participate and grow your wealth with a portfolio of equity, debt, real estate and commodity investments.

Other than these, you can also invest in commodities like gold and silver, and investment trusts. However, these investments require big-ticket inflows and offer lower liquidity. On the other hand, some of the most liquid, i.e., easy to sell, investments in India include liquid funds and savings accounts.

Being a salaried individual or even as a self-employed businessperson, you must realise that you cannot achieve your life goals by relying on your savings alone. Instead, it would help if you found ways to maximise your savings and build wealth that meets your and your family’s needs. To do this, you must invest these savings in an investment plan that helps you avail of high returns but with minimal or no risk involved.

On the other hand, if you choose not to invest, you may miss out on various opportunities to maximise your wealth-building potential and financial worth. If you invest your money wisely and on time, you can easily make significant gains throughout the investment tenure.

To choose the right investment plan for yourself, you need to consider the following points -

Also Read: Direct Investment

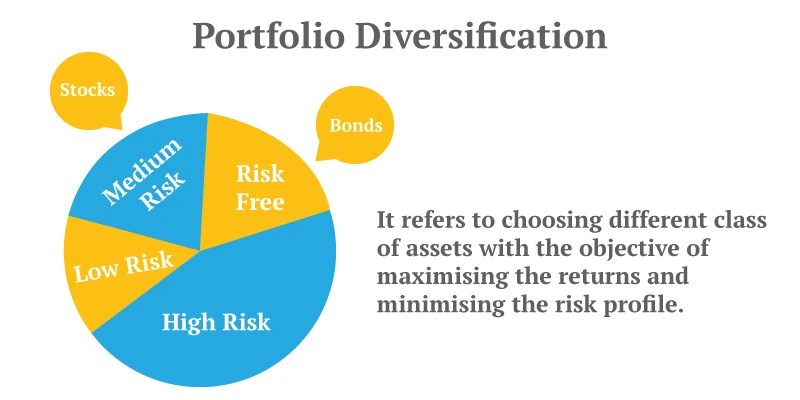

Each investment instrument carries a distinctive risk profile and potential for return generation. For each of these plans, their associated risk of investment can be described as the probability of the plan performing either below expectations or experiencing an irreparable loss of value.

Based on the risk associated, we can broadly classify different investment plans into three categories:

Different types of investments in India offer different risk, return and maturity (liquidity) features. For the best results, you should check for the following eight factors while choosing different investment options:

Every investor has different goals, risk tolerance, and timelines. That’s why it’s important to choose investment options that align with your needs and offer the right balance between risk and returns. Whether you prefer the stability of traditional savings schemes or the growth potential of market-linked instruments, there’s a wide range of choices available today.

If you're looking for a plan that combines long-term growth with life cover, Unit Linked Insurance Plans by Canara HSBC Life Insurance can be a well-rounded option. These plans give you the flexibility to invest in equity, debt, or balanced funds, while also ensuring financial security for your loved ones.

In the end, a mix of informed choices and disciplined investing is what helps turn today’s savings into tomorrow’s financial confidence.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.