Written by : Knowledge Centre Team

2026-01-29

3898 Views

6 minutes read

Share

If you are in your 30s, it is natural for you to feel safe about your retirement years. However, imagine your life without your salary income for a few months, and you will feel the pressure building up.

Before you can retire, you need to build a corpus large enough to provide you with a regular income. That’s where annuities come in. By investing your retirement corpus in an immediate annuity plan, you can convert your savings into a guaranteed stream of income. It’s a way to ensure that even as you step back from work, your money doesn’t stop working for you.

Key Takeaways

|

An immediate annuity is a financial agreement between you and an insurance company, where you invest a lump sum and start receiving regular payouts almost right away. These payments are fixed and continue for a set period or even for the rest of your life, providing a steady income stream after retirement. It helps turn your retirement savings into a predictable monthly income. Immediate annuities are especially useful for those looking to secure their post-retirement lifestyle without worrying about market fluctuations

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

There are two types of annuity plans:

As you come close to retirement, other long-term goals are complete. You tend to slow down. Being a retired person, you stop investing and start consuming what you have saved and invested in the past. A regular income is needed to spend happy retirement years.

Below are some of the reasons you need to have a regular income:

Below are the benefits of investing in an immediate annuity plan:

There are different types of immediate annuity plans available in the market. You must know how to select the best annuity plan for yourself. Below are parameters that will help you choose the right annuity plan:

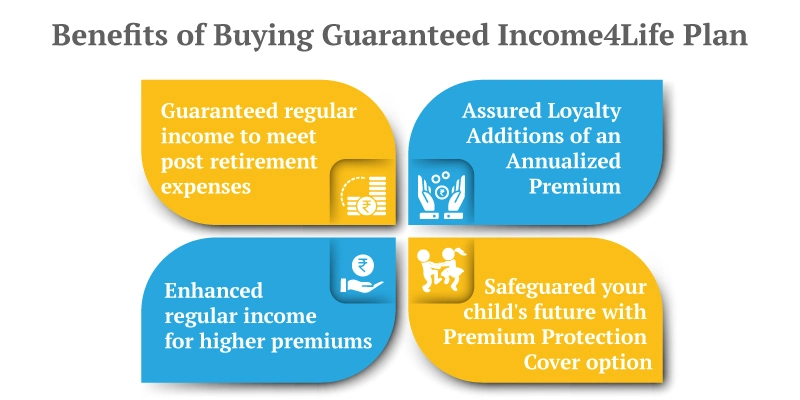

In the Pension4Life Plan by Canara HSBC Life Insurance, there are seven different options for you, and five of them are immediate annuity plans. With an immediate annuity plan, one continues to receive payments till the death of the last survivor. There are death benefits as well. Upon your death, the purchase price (value of your investment corpus) is given to your beneficiary.

This plan offers additional benefits and options such as:

Return of invested money on the diagnosis of critical illness or accidental total and permanent disability, or death

Joint life annuity with return of purchase price on the death of the second annuity holder

You work hard all your life to secure your after-retirement life. You want to live a stress-free life, and for that, you need a regular income. Annuities are a perfect solution for you as they help you create a regular income from the wealth you have accumulated over the years.

You can enjoy the second inning with your loved ones without worrying about the market fluctuation. Immediate annuities from life insurance providers offer a safe and reliable way to convert your wealth into income.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.