Written by : Knowledge Centre Team

2025-11-05

1195 Views

Share

In Indian households, especially among the middle class, breadwinners find it essential to have a term insurance plan to secure their family's future against the uncertainties of life. For a relatively low premium over a customisable period, term insurance plan holders can provide their family with a predefined sum in case of an untimely demise.

But towards the end of the day, only we know our family best – many policyholders worry about how their family may spend the money they leave behind. If not managed wisely, a large lump-sum death benefit can be exhausted quickly and leaving them with less security than they began. This potential misappropriation of the death benefit is a cause of concern for many policyholders. Many companies have started to roll out staggered payout systems where the family cannot access all the saved money in one go. Let’s explore these options.

Key Takeaways

|

A term insurance plan is one of the simplest and most affordable ways to protect your loved ones financially. If something unfortunate happens to you during the policy term, your family receives a fixed amount of money, known as the death benefit. Unlike other insurance plans, term plans don’t come with any savings or investment benefits. They’re purely meant to offer support when your family needs it most. You choose the duration, how much coverage you want, and how you’d like the money to be given to your family, either all at once or in smaller amounts over time. It’s a plan built around your priorities and how you want to care for your family, even when you’re not around.

Many banks offer life insurance payouts as lump sums. The assured sum is ₹1 Crore; the family will be given that large sum of money in one go. In cases where the term insurance plan offered a lump-sum amount of money immediately after the policyholder's untimely demise, the family may splurge on the funeral or on other exorbitant goods and services, leading to financial instability.

If the concerned nominee for the lump sum money is not good at finances or wastes all of it in a short period, the whole idea of securing your family’s future is defeated.. This is one of the main reasons why companies are offering varied payout options in their term insurance plan: to help families manage the death benefit more efficiently and avoid financial missteps.

The option to go for staggered payouts allows term insurance plan holders to choose how much money their nominated family member would get and when. In some instances, a certain percentage of the full amount is given upfront, followed by small sums paid as monthly instalments over the next several years, sometimes extending two decades or more.

This option ensures that the family has immediate access to some funds for urgent needs, while also securing a steady monthly income to help them manage day-to-day expenses over time.

Most companies that offer a term insurance plan provide staggered payouts in multiple combinations that you can choose from:

The nominee receives a high proportion of the sum assured as an immediate death benefit, followed by a monthly income paid from the remaining sum. The initial sum can be anywhere from half the guaranteed amount to 75% of it. The remaining will be paid according to how much is left and will be small financial assistance to the family (unless they store the immediate death benefit sum in a thrifty manner)

The assured death benefit lump sum is half the overall amount, and the rest is paid in monthly instalments. This strikes a perfect balance between lump-sum and staggered payouts and is arguably the best option for those who are unsure of their family's financial planning skills. The initial payout can cover immediate expenses, such as funerals or impending weddings, in the case of an untimely death. Simultaneously, the rest can be delivered to the nominee as a monthly income for their upkeep.

Lastly, there are total staggered payouts, where the monthly income increases by 10%-20% every year. This is beneficial for many reasons – if your nominee is a child who will eventually grow to be a college student, there will be a need for an increase in the monthly allowance. Increments in monthly instalments also take into account possible inflation – the money we pay today, in 2025, may not be enough to cover the needs of someone in the future, which is why increments are highly recommended for those going for a long-term insurance plan.

Now that you are aware of the various ways in which the banks offer to provide your nominees or your family with financial support, you must pick a combination. Here are a few things to consider while you are pondering it.

Judge things from an overall return perspective. After considering the inflation and devaluation of the currency, you may find it ideal to go for an incremental plan, especially if you have children and if your term insurance plan goes beyond a decade after your death.

At the same time, it is also possible to invest in a lump sum. If you are not the sole breadwinner of the family, and your partner/spouse works and earns a steady income, your family may not have to rely on your death benefit to lead a good life. If that is the case, you can arrange for a lump sum death benefit and advise your family to invest a large amount of money in a bank. Inflation will then work in your favour and provide excellent returns over the years once it gains interest.

Consider your family's financial literacy – if you think your family will find it difficult to manoeuvre around bank jargon. In case you are afraid, they may not understand the complicated procedures and paperwork, and a lump sum investment might not be for you. On the other hand, if they are entirely unfamiliar with the bank system and you are sure that they will use the large death benefit funds frugally, you can trust them with it. Ultimately, no one knows your family as you do.

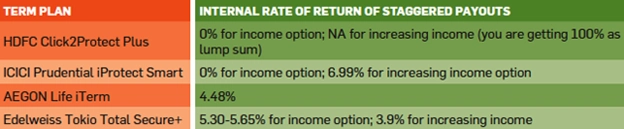

A family that is not familiar with technology and, by extension, scams that use technological literacy may fall prey to con artists. Combined with financial illiteracy, there is always a possibility that their lack of tech-savviness can lead to the loss of the death benefit fund. If you intend to have your family invest the insurance money after your untimely demise, make sure you walk them through the process and warn them against potential scammers.Understanding the Internal Rate of Return (IRR) When comparing lump-sum and monthly payouts, it help

When comparing lump-sum and monthly payouts, it helps to look at the Internal Rate of Return (IRR), a measure of how efficiently the money works for your family over time.

Consider the Internal Rate of Return – much like the choice between limited pay term insurance plans and ordinary insurance plans, we must consider the overall savings we can make from choosing between both options. As in the limited plans, there is no significant difference between the internal rate of return in a lump-sum or a staggered payment.

The usual internal rate of return is below 7% and can go as low as 4%. These modest returns are usually tax-free, which makes them more appealing than returns from Fixed Deposits (FDs), where interest income would require you to pay tax.

The premium to be paid every month is significantly higher for the staggered incremental option. If you are not in a position where you can pay off your premiums in a disciplined manner, and if there is the slightest chance that you may miss a premium, it may be better for you to go for an ordinary lump sum term insurance plan. From a pure returns perspective, the staggered instalment option is far less convenient than a standard lump sum plan.

That being said, there are other ways to maximise return, even in the case of the lump sum amount. Other than fixed deposit rates, you can use a combination of systematic withdrawal plans, post-office monthly income schemes, credit cards, recurring transfer, debit funds, and more to get a high internal rate of return.

The pros and cons are more or less equally balanced. While a steady income in the form of monthly instalments can ensure that your family is steadily provided for, the lump sum can offer long-term returns if invested in the right manner. The lump-sum option may also help settle any liabilities and provide a quick source of money in health emergencies, expensive occasions like weddings, etc.

To make the right decision, it is paramount that you talk to your bank of choice and get to know more about all the options available to you – they may offer you a fresh perspective that you may not have thought about before. For extra reassurance, you can even ask your peers or an accountant for a second and third opinion.

If an expert in financial matters knows your family well enough to suggest the best option for you, that would be perfect. You can also look into your family members' history with large sums of money or coach them before the expiry of the term insurance plan so that they will be able to either invest the money right or carefully use the monthly increments.

The term insurance plan you choose, and the consequences of that decision, will outlive you. Contact a bank that offers you the package that you and your family need - Canara HSBC Life Insurance can provide you with an excellent term insurance plan that will secure your family's future, letting you live the rest of your life assured that they will be taken care of.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.