Written by : Knowledge Centre Team

2026-07-23

1214 Views

8 minutes read

Share

In today’s world, having an insurance policy is a suitable way to protect the future of your loved ones. A term life insurance plan is one of the most popular ways in which people protect their dependents and their family in today’s age.

Buying term life insurance can help you protect your financial future. However, making the wrong choice from the myriad of options available can also cause great damage to your long-term financial goals. Given that the life insurance penetration rate in India remains one of the lowest, 2.74%, it is assumed that many Indians still have several queries about buying a term insurance policy.

These doubts are perfectly reasonable and necessary before you make any purchase. In this article, we attempt to answer some of the most frequently asked questions and doubts people raise regarding term insurance policies. Purchase your term plan now!

Key Takeaways

|

Buying term insurance is a key financial decision, and asking the right questions ensures you get the right cover. It helps you understand policy terms, claim processes, and what is truly included in your plan. Many overlook crucial details, such as exclusions, premium variations, or benefit options.

Asking questions clears confusion and avoids future surprises. It also builds trust in the insurer and boosts your confidence in the policy. Whether it is about payout options or medical tests, clarity leads to better choices. Being curious today can protect your family from uncertainty tomorrow.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Choosing the right term insurance policy requires clarity and a thorough understanding. The following are the top 10 questions you must ask before purchasing term insurance, and save yourself from confusion later:

It is a common practice to plan premium payments far ahead in the future, so it is no surprise that this is a very pressing query that many customers have. A fluctuating term premium amount can cause many complications in the planning and achievement of long-term financial goals. It may even jeopardise the financial stability of a family.

Fortunately, the premium amount of an ordinary term insurance policy should remain the same throughout its duration. It does not fluctuate unless specifically mentioned otherwise in a clause at the time of the purchase. Of course, it is a different case if the policyholder develops a disability/lifestyle disease later on in their life, in which case most insurance providers retain the capacity to increase their premium amount.

Here are 14 reasons you might be paying a higher premium:

Customers who tend to develop addictions should think twice before purchasing a term insurance policy. This is because habits like frequent smoking or drinking allow insurers to move the policyholder’s case into what is called a different risk pool. Moreover, the policyholder’s life now remains endangered due to their lifestyle disorder. In such cases, insurance companies reserve the right to impose higher premiums, or in extreme cases, complete cancellation of the plan.

To prevent the decline of the death benefit claim by the dependent in the case of unfortunate death, it is well-advised that policyholders divulge any information about such bad habits to the company well in advance.

While this depends largely on the company’s rules, habits like smoking or drinking that have detrimental effects on a person’s life expectancy do impact the cost of a term life insurance policy and the price of each premium payment.

Some insurance companies require clients to disclose at the time of purchase whether they have any life-threatening habits. While other companies will accept policyholders who have refrained from such a lifestyle for a few years before the purchase. It is recommended that you go through your preferred insurance provider’s policy rules before going ahead.

Usually, yes. Regardless of how the policyholder unfortunately passed away, term insurers are liable to pay the dependents the assured sum. However, you can boost your existing term life insurance plan by paying for additional riders that include accidental death, permanent disability, or critical illness. This will ensure that the nominee gets additional money other than the sum assured upon the policyholder’s death.

Yes, provided that the policyholder has informed his insurer that he has moved to a non-Indian residence. In such cases, the policyholder is required to update any changes in personal information. This includes the phone number and address.

However, keep in mind that the insurer can defer the death benefit if the policyholder unfortunately passes away in a country that is considered to be high-risk. This may include countries that experience a high rate of terrorism and violence against them. For other countries, term insurance policies are usually valid.

Insurers are not liable to pay any sum assured if the policyholder outlives the maturity of the term insurance policy. This usually upsets people, which is why it is important to ask such questions before the purchase of a plan.

However, many insurance providers allow you to upgrade your policy using a conversion privilege, which allows you to trade in the old policy for a new one. It is highly advised to pick a policy that offers a premium rise and the capacity to pay for additional liabilities like your children’s education, house rent, etc.

Transparency is everything in the world of banking, which is why you should always declare that you possess multiple policies before signing up for a new one. This is especially true if it is from another company. It is paramount that the person making the claims submits the death certificate to the company that has the longest-running policy under the deceased individual’s name.

The companies should also be informed of the same, along with the acknowledgement from the first company that the settler approached.

This depends on what kind of claim it is. An early claim, when the policyholder untimely passes away after purchasing the term insurance, requires a thorough investigation due to a higher cost for the insurer. However, if it is an ordinary claim where the policyholder has paid off his premiums for more than a decade, the company will relent and settle the claim without an in-depth investigation.

Yes, if the policyholder unfortunately passes away due to terrorist attacks, natural calamities like earthquakes or tsunamis, etc. During such times, the insurer is not liable to pay the nominee the sum assured. Such claims do get settled at times, thanks to the interference of the Insurance Regulatory and Development Authority. It is always well-advised to go through such terms and conditions before the purchase.

Yes, they can be provided if they have documents that prove that they are not a liability. This includes age/address proof that they currently reside in India. Such documents can be sent to the insurer remotely when you purchase online term plans in India, and the necessary medical reports can be completed when the individual makes their next visit to the country.

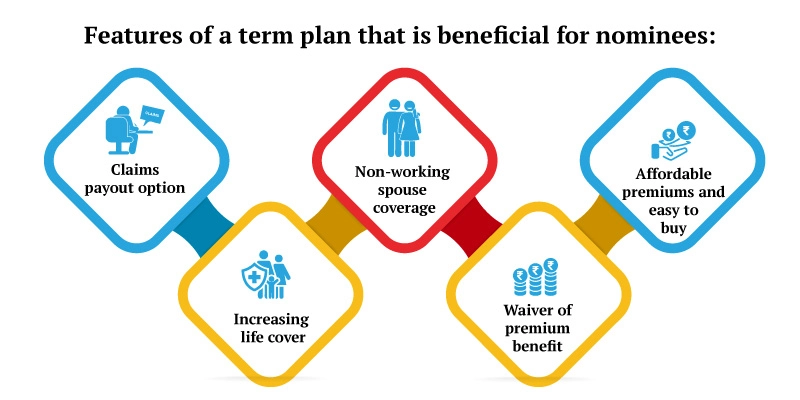

When you are looking for the best term life insurance, you will find several options, one of which will be the iSelect Smart360 Term Plan by Canara HSBC Life Insurance. This term plan offers the following benefits:

The return of premium ensures that the nominee will receive every penny you invest in the plan.

An increasing sum assured, which guarantees better returns on investment.

An option to cover your partner as well, negating the need to purchase a secondary plan.

Limited premium payment option, which allows you to plan your long-term financial goals with better precision.

Purchasing a term insurance plan is essential for completing your financial portfolio and can provide a basic safeguard for the future of your loved ones. It will help you ensure the financial stability of your family after your time. However, before choosing the best term life insurance plan, it is necessary to ask the right questions.

At Canara HSBC Life Insurance, we therefore keep our support channels available most of the time. Whether you wish to connect online or offline, we have both options available. Reach out in case of any queries right away.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.