Written by : Knowledge Centre Team

2026-06-01

11075 Views

15 minutes read

Share

The full form of TDS is Tax Deducted at Source. You may have experienced TDS in various forms, such as bank FDs, salary payments, and vendor payments, as TDS seems to infiltrate everywhere. Normally, TDS means an advance tax withheld by the payor from your income, whichever form it is.

So, it ends up reducing your income. Therefore, it should be an important focus when looking to save tax. However, does it mean you do not need to file an income tax return? Or can the deduction benefit you anywhere? Let’s find out.

Key Takeaways

|

TDS or Tax Deducted at Source is an income tax that is collected from certain payments like rent, salary, commission, interest, professional fees, etc. The person paying the amount should deduct TDS from such a payment.

As per the Income Tax Act, any company or a person is required to deduct tax at the source itself if the money paid exceeds the specified limit. The person who receives a payment also has a liability to pay tax on their income.

The payee will receive credits against the TDS payments, which they can claim against their actual tax liability while filing the annual ITR.

The purpose of TDS may have been to reduce the chances of tax evasion by the recipient of the income. But, for an honest taxpayer, it also brings a few benefits.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Even when you are making payments as an individual taxpayer, you need to deduct TDS on certain payments. The following are the types of payments that attract TDS:

| Category | Description | Example |

|---|---|---|

| Salary & Wages | Income received for regular employment | Salary Transfer |

| Professional Fees | Fees earned for professional services | Professional Fee |

| Consultation Fees | Fees charged for providing advice or expertise | Consultation Fee |

| Rental Income | Income received from renting property | Rent Payments |

| Commissions & Brokerage | Payments earned for facilitating transactions | Commission to agents, brokerage on deals |

| Investment Income | Earnings from invested funds | Interest on Securities & Deposits, Dividend on company shares and mutual funds |

| Winnings | Money won through games or competitions | Lottery, lucky draw and similar winnings |

| Royalty Income | Payments received for the use of intellectual property | Payment of Royalty |

| Director's Remuneration | Compensation paid to company directors | Director’s Remuneration |

| Property Sales | Income from the sale of property | Transfer of Property |

| Other Interest | Interest income not covered elsewhere | Interest on loans given to others |

TDS return is one way of minimising your taxable income. It is a return filed for tax deducted at source. The return is filed every quarter. It is done through a separate form depending on the nature of the payment.

You may make multiple payments to different parties for their services during the year. If the total payment to any one party crosses the limit specified under Sections 192 to 195 of the Indian Income Tax Act, you must deduct the applicable TDS.

Once TDS is deducted, it must be deposited every quarter along with the corresponding TDS return. The form you file will depend on the type of payment and the section under which it is covered.

TDS has to be deducted at the applicable rates only. Let us understand it through an example. Rent paid to a resident individual or HUF attracts 2% TDS when the monthly rent exceeds ₹50,000.

If you are living in a rented house and paying ₹70,000 per month, you need to deduct ₹1,400 as TDS before making the payment. You will then pay ₹68,600 to the property owner and deposit the deducted TDS amount with the CBDT in the relevant quarter.

Similarly, a firm may deduct TDS on the fees payable to a consultant for the professional services at 10%.

TDS ensures that tax is collected gradually, making it easier for the government to track and manage income tax payments. For salaried individuals, TDS is calculated based on the income slab applicable to their total earnings. The employer is responsible for deducting the TDS from the salary and depositing it with the government. The employer estimates the total expected income of the employee for the year, adjusting for bonuses, salary hikes, and submits investment proofs aimed at tax saving.

For other forms of income, such as rent, interest, or contract payments, the TDS rate is determined by the nature of the income, not the amount received. This means that different types of payments have different TDS rates as defined by the Income Tax Act.

Pro Tip: Keep track of any changes in your income, like bonuses or additional investment declarations, throughout the year to avoid a hefty TDS deduction in the final quarter. Planning ahead with tax-saving investments starting in April can help adjust TDS rates early and minimise surprises.

Remember, the person making the payment is responsible for deducting the TDS and depositing it with the government. If the payer doesn’t have the recipient’s PAN, TDS is deducted at a higher rate of 20%.

The regulation of a 20% TDS deduction in the absence of the recipient’s PAN is governed by Section 206AA of the Income Tax Act 1961

Source: Incometax India

TDS is designed to make tax collection easier and more efficient for everyone involved. By deducting tax at the time of payment, it creates a structured system that supports taxpayers, ensures transparency, and strengthens the country's financial management. TDS offers multiple advantages for both taxpayers and the government in the following manner:

Tax Deducted at Source (TDS) acts like a pay-as-you-earn scheme for income tax. Overall, TDS can be a helpful tool for managing your tax burden and avoiding penalties. But remember, it's still crucial to understand your tax obligations and file your return accurately. Here's how it benefits you:

Any person, including an individual, HUF (Hindu Undivided Family), firm and NRIs (non-resident Indians), is required to deduct tax at source (TDS) if a payment falls under the heads of income or specific provisions outlined in the Income Tax Act, 1961.

Individuals and HUFs are generally not required to deduct TDS unless explicitly specified under the Act.

Key scenarios where TDS applies:

While Tax Deducted at Source (TDS) applies to a wide range of incomes, certain payments are exempt if they fall below prescribed limits. These exemptions are designed to ease compliance for taxpayers with smaller earnings and ensure that only substantial payments are brought under the TDS net.

For instance, interest earned on bank deposits up to a specified threshold, rent payments below a certain limit, or even cash withdrawals within the permissible ceiling, do not attract TDS. Similarly, individuals and HUFs making payments to professionals, contractors, or for goods are not required to deduct TDS if the aggregate value of the payments remains within the exemption limit.

Knowing these exemptions can help taxpayers avoid unnecessary deductions, reduce refund hassles, and plan cash flows more efficiently.

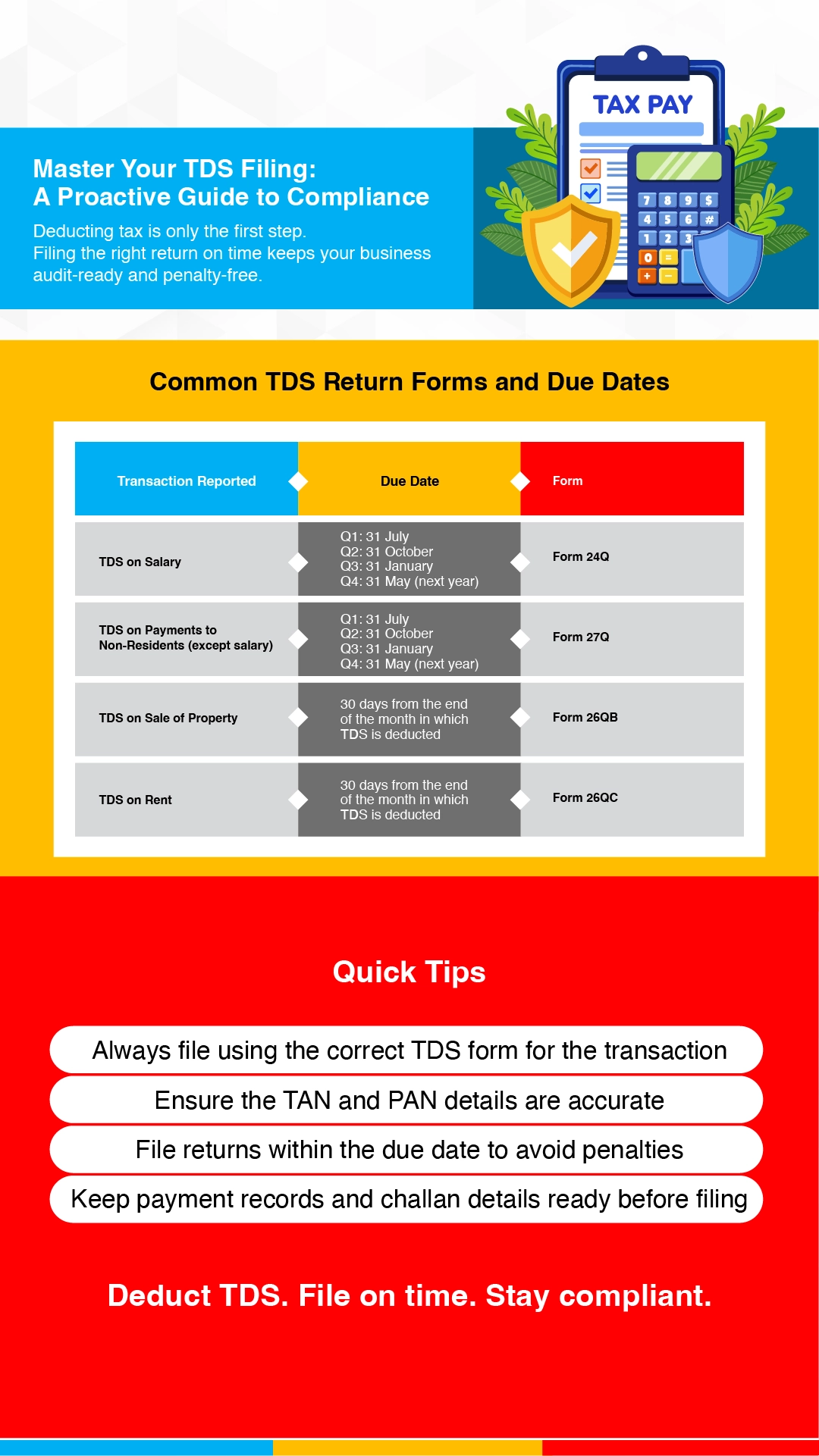

You will need to use the appropriate form based on the type of payment on which TDS has been deducted. Corporations and payers paying NRIs usually need to file TDS returns every quarter.

Other payments will require a TDS return within a stipulated time as per the table below:

| Transactions reported in the return | Due date | Form |

|---|---|---|

| TDS on Salary | Q1: 31st July Q2: 31st October Q3: 31st January Q4: 31st May of Next Year | Form 24Q |

| TDS on all payments made to non-residents except salaries | Q1: 31st July Q2: 31st October Q3: 31st January Q4: 31st May of Next Year | Form 27Q |

| TDS on the sale of property | 30 days from the end of the month in which TDS is deducted | Form 26QB |

| TDS on rent | 30 days from the end of the month in which TDS is deducted | Form 26QC |

In order to file a TDS online, you will need a TAN or Tax Deduction & Collection Account Number to file a TDS return. Follow the process below to file your TDS return online:

While filing TDS, you also need the payee's PAN and bank account details. If the payee’s PAN is linked with Aadhaar, you can upload your returns using the Electronic Verification Code (EVC).

Filing a TDS return requires submitting specific forms to ensure compliance with tax regulations. Below is a list of the key forms involved in the TDS return filing process:

Taxpayers are required to submit TDS return forms based on different dates and quarters as mentioned below:

Quarter | Quarter Period | Form Filing Last Date |

Quarter 1 | 1st April to 30th June | 31st July |

Quarter 2 | 1st July to 30th September | 31st October |

Quarter 3 | 1st October to 31st December | 31st January |

Quarter 4 | 1st January to 31st March | 31st May |

Tax Deducted at Source (TDS) is applicable to a wide range of regular payments. Here's a quick look at the prevailing TDS rates for different payment types.

| Type of Payment | Sections | TDS Rate |

|---|---|---|

| Salaries | 192 | Applicable Slab Rates + Cess |

| Interest from Securities (Bonds & Debentures)* | 193 | 10% |

| Interest on deposits* | 194A | 10% |

| NSC Maturity Value* | 194EE | 10% |

| Sale of Mutual Fund Units back to Mutual Fund# | 112A | 20% |

| Payment for Professional Services* | 194J | 10% |

| Rent Payment by Individuals Over ₹50,000 p.m. | 194IB | 2% |

| Lottery & Other Types of Winnings | 194B | 30% |

| Payment to Resident Contractor / Sub-contractor | 194C | 1% (HUF & Individuals) 2% (Others) |

| Commission on Insurance | 194D | 5% (HUF & Individuals) 10% (Others) |

| Acquisition of immovable property | 194LA | 10% |

| Rent payments for Plant, Machinery, Furniture, etc. | 194I | 2% (Plant, Machinery & Equipment) 10% (Furniture, fixture, land and building) |

| Commission & Brokerage payments | 194H | 5% |

| Commission on the sale of lottery tickets | 194G | 10% |

Anyone deducting TDS from the payments made to another party as income should deposit the amount to the Central Government Account before the 7th of the next month.

For Example:

| TDS Deduction Month | Deposit Due Date |

|---|---|

| April | 7th May |

| May | 7th June |

| June | 7th Jul and so on |

Except for March, when you can deposit the TDS amount by 30th April.

The deducting party issues TDS certificates to the taxpayers. It is an official document that states your tax has been successfully deducted at source. Depending on the type of payment, TDS certificates can be issued in the following forms:

| TDS Deducted on | Form & Frequency | Due Date |

|---|---|---|

| Salary Payments | Form 16, issued annually | Before 31st May of the Assessment Year |

| Non-Salary Payments (interest, vendor payment, consultancy fees, etc.) | Form 16A is issued quarterly | Within 15 days of the due date |

| Sale of Property | Form 16B is issued with every transaction | Within 15 days of the due date |

| Rent Payments | Form 16C is issued with every transaction | Within 15 days of the due date |

Form 16 and Form 16A are tax credit statements that reflect the TDS from an individual’s or a company’s income. Form 26AS, on the other hand, is a consolidated tax statement generated by the Income Tax Department, showing TDS details for an individual or company.

The party deducting the TDS can issue a TDS certificate in the applicable Form 16. The deducted TDS amount is reflected in Form 26AS as Tax Credits for the payee (person receiving the amount after the TDS deduction).

If you want to claim a TDS return you will need to file your ITR for the Assessment Year (AY). The applicable credits are adjusted out of your tax payable for the AY. If eligible for a refund, the same will be processed and credited to your bank account within six months.

In case the deducted TDS amount does not show up on your Form 26AS, you will need to submit the TDS certificate received from the deductors.

Once TDS is deducted from your income, a series of steps is taken to ensure the amount is remitted to the government and correctly reflected in your tax records. Understanding this flow helps you track your tax credit and stay compliant during return filing. After TDS is deducted from your income, here's what happens:

After deducting TDS, the payer must complete several legally mandated steps. These actions ensure your tax is deposited on time and accurately recorded in the government system. Here's a look at your role as a TDS payer:

As the recipient of income, you must review the TDS details shared with you and make sure they match your actual income. Doing this ensures your tax return reflects the correct information and helps you avoid errors or delays in your refund. The following are your responsibilities as a recipient:

Thus, don’t miss filing your personal ITR, especially after TDS on any of your income.

The TDS deduction depends on the payment amounts. If you are salaried, your TDS amount is estimated on your salary and can change if there is a change in the salary amount. Similarly, TDS deductions can change under the following situations:

Overall, your TDS deduction should not be less than your total tax liability at the end of the year.

CBDT may levy a penalty for delays in submitting your TDS return or statements in the following manner:

The updates regarding TDS continue to evolve to help improve compliance and ease the tax collection process. Listed below are some of the key compliances:

Tax Deducted at Source (TDS) is not just a compliance requirement; it’s an important tool that makes tax collection smoother for the government while helping taxpayers manage their liabilities in smaller, regular portions. Understanding how TDS works, its applicable rates, exemptions, and filing obligations ensures you avoid penalties and claim rightful refunds.

While TDS may feel like a deduction from your earnings, it ultimately reduces your year-end tax burden, prevents last-minute financial stress, and promotes transparency in the tax system. Staying updated with the latest TDS rules and filing your Income Tax Return (ITR) on time is the key to making the most of these deductions.

In short, think of TDS as advanced tax planning rather than a burden; it not only keeps you compliant but also helps you stay financially prepared and secure.

The full form of TDS is Tax Deducted at Source. It is a way of collecting advance tax on income-related transfers to individuals and other tax-paying entities.

TDS on salary is deducted on applicable slab rates. You can choose to pay TDS as per the new tax regime or stick to the old tax regime where you can also claim tax-saving investments. Rebates under section 87A are available under both tax regimes.

A TDS challan is generated when you file your TDS return. The challan helps you deposit the TDS amount under the correct classification code when you deposit the money into the Central Government account.

Yes, PAN is necessary for TDS payments. Without PAN you may face higher TDS rates.

Usually, PAN is needed for almost all TDS transactions. In case you cannot submit PAN immediately you can apply for a PAN and submit the application number in the meantime. In a few cases, like interest payments by banks, not furnishing PAN or the application number will attract a higher TDS rate of 20%.

Different incomes attract different TDS rates, such as 10% on professional fees, 2% on technical services, and 5% on rent from individuals, depending on applicable tax provisions.

A TDS challan is a government payment slip used to deposit the deducted tax. You fill it online, provide relevant details, and pay through net banking or authorised channels to complete the deposit.

You can claim TDS credit by checking Form 26AS or AIS for accuracy, then reporting the deducted amount on your tax return so the credit is applied to your final tax liability.

Failure to understand when to deduct TDS or deposit it on time can lead to interest, penalties, disallowance of expenses, and possible legal consequences affecting the deductor’s compliance record.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.