Written by : Knowledge Centre Team

2026-07-29

1110 Views

7 minutes read

Share

As a parent, one of the most important obligations is to fulfil the educational goals of your child, so they can go on their way to fulfil their aspirations. Although you can invest in any of the several long-term investment options available, child plans could still be the best investment plan for your child’s future.

Your children are the biggest hope of your life. One of the most fulfilling goals of your life is to see your children accomplish their aspirations. With education costs soaring due to high inflation, funding higher studies is becoming increasingly challenging. To ensure a safe future for your child, start investing early and consistently invest in the best child insurance plan for a long period.

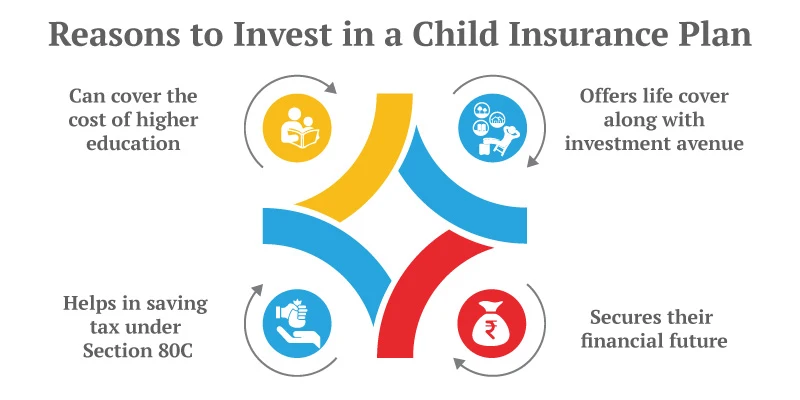

Key Takeaways

|

When it comes to providing for the higher studies of your children, you need your life’s savings to work harder. The best child insurance plans can provide you with the much-needed financial assistance for your children’s education and other goals:

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

There are 3 broad categories of a child's education plan:

Canara HSBC Life Insurance Promise4Growth Plus is one such lucrative plan that offers complete freedom to investors to allocate the funds in various portfolios. Additionally, it offers three cover options for different life stages of your child.

Child insurance plans work in a very systematic way to serve the dual goals of giving you a life cover as well as providing you with a certain maturity amount for your child’s goals.

Canara HSBC Money Back Advantage Plan comes with a policy term of 16 years and a premium payment term of 10 years. It offers regular payouts of 15% of the total sum assured, at the end of the 5th, 9th & 13th policy year. Finally, at maturity of the policy, you will receive a guaranteed lump sum amount, which shall be equal to 55% of the total sum assured, along with accumulated bonuses at simple rates.

In the case of a ULIP Child Plan, you can easily opt for complete withdrawal from the policy with all your accumulated investment corpus, but only upon completion of at least 5 years of the policy term. This withdrawal shall be tax-free, offering you the flexibility to withdraw at any point in time.

Child insurance plans such as the iSelect Guaranteed Future from Canara HSBC Life Insurance offer safety to your child’s goal with multiple investment options. Even in the case of your early demise, your child’s goal will remain unaffected, as:

This way, the child education plans ensure continuity of the investment even after your untimely demise. Now, you can easily understand how a suitable child education plan is the best investment plan for your child’s future.

Preparing for your child’s future in the present era has become a necessity. With the steep rise in education costs, relying solely on savings may not be enough. A child insurance plan provides a structured way to save for long-term goals and also ensures your child’s dreams remain protected, even if life takes an unexpected turn.

Whether you opt for a guaranteed endowment plan, flexible moneyback plan, or high-growth ULIP-based Plan, choosing the right policy tailored to your needs can give you peace of mind.

Plans like those offered by Canara HSBC Life Insurance are designed to adapt to your child’s growing needs while providing essential financial security.

Start early, choose wisely, and watch your investment grow with your child.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.