Written by : Knowledge Centre Team

2026-07-28

1205 Views

7 minutes read

Share

As a parent, you must have dreamed of your kids fulfilling their aspirations, such as becoming a doctor, pilot, astronaut, or sports star. Of course, these high-flying needs require a lot of effort, hard work, dedication, and most importantly, timely availability of funds. No matter how much savings you have accumulated you still need something additional to help your children accomplish their endeavours.

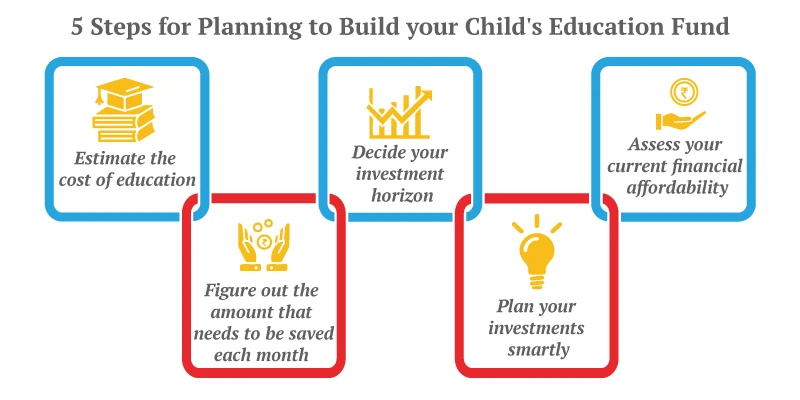

If you wish to get an adequate amount of funds necessary for the higher studies for your children, you need to channelize your savings into the right plan. Getting a child education plan is the most feasible way you can multiply your savings for the future needs of your little whiz kids.

Thus, a term insurance plan will ensure your family’s financial health, while a child plan will ensure a future for your children.

Child Education Plans are a type of life insurance plan that serves the dual motive of providing you with a life cover as well as multiplying your savings. You get a handsome maturity amount for your children’s educational needs at the end of the plan.

Hence, a child insurance plan is a kind of investment cum insurance plan that ensures financial security to fulfil your child’s long-term educational goals. You can utilize the maturity value of a child insurance plan to spend on various goals such as sending your ward abroad for higher studies, or his/her marriage.

Before we look at how child plans work we need to know the different child plan options you have. The majority of child education plans fall into three different categories given below:

This way, you can manipulate all the market speculations to your utmost financial gains. Hence, it’s a truly investor-friendly plan. Moreover, the ULIP child plan will offer you loyalty bonuses for your long-term continuation with your policy. All the gains from a ULIP plan are tax-exempt unless the annual premium goes beyond Rs 2.5 lakhs.

To understand how the child education plans work to secure the future of your children, you need to focus on the following features of your child education plan:

Undoubtedly, any child insurance plan offers you a certain maturity amount at the end of the policy. However, there is an important thing you might be missing out on. In case of your early demise, an ordinary plan will only ensure that your family receives the sum assured, and with that, the policy will stop. Now, what makes a child’s plan different from an ordinary plan is that it has a unique feature called the Premium Protection option.

This way, the Premium Protection option ensures that your policy continues even when you are not around and your child receives the much-needed funds for his/her education.

Yes, you can partially withdraw from your child insurance plan. There are different rules for partial withdrawal in different types of policies:

These are the key features that make your child insurance plan work effectively for the accomplishment of your child’s long-term goals.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.