Written by : Knowledge Centre Team

2025-11-13

884 Views

6 minutes read

Share

A child insurance plan is a good investment to make sure your child achieves your goal. The moment you have a child, you start planning for his future. You want nothing but the best for your child. One of the ways to ensure a stable future for your child is to offer a good education.

However, premier institutions at times have a higher cost, and the only way to meet these costs is to save as your child grows up. Child insurance plans are one of the strong investment options for your child’s goals. With child education plans you have two options of investment:

Both options offer adequate investment tenure. However, the child plan with an aggressive investment option lets you stop investments once your goal has been achieved.

For example, if you aimed to build a corpus of Rs 50 lakhs when your newborn child reaches 20 years of age, you have 20 years to build it. However, if your investments happen to achieve this within just 15 years, you can stop further investments.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

This way, you can direct your savings to other financial goals while your child’s future goal is secured.

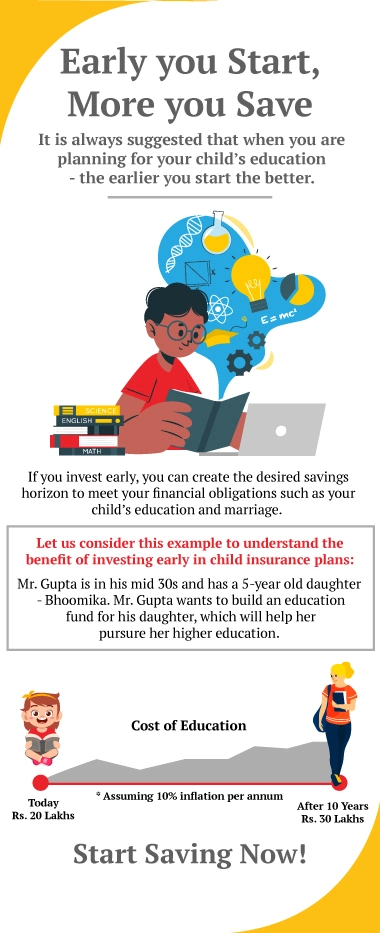

Planning for a goal takes some effort. Even if you plan and think that you will get through with the plan, life may have other plans.

Suppose you have bought a child education plan for your little one. What will happen if you die unexpectedly and the policy still has time to mature? In this case, will your family be able to pay your premiums?

Will the death benefit that your family will receive be enough at the time your child attains the higher education age.

To tackle problems like these, you should consider the policies which offer the Waiver of premium rider option.

As the work of every rider, Waiver of Premium rider also enhances your existing policy’s scope. If you have opted for this rider, then the company will take care of the remaining premiums if you die during the policy term.

The investment portfolio of the policy continues even after your death, with the planned remaining investments as if you are still alive.

Thus, this rider ensures that your child will have the corpus you had planned upon maturity even after you are not there.

When you buy a child insurance policy, you are given an option to choose riders. While most of the insurance companies have this as an add-on to the policy, some have it included with the policy itself.

Let's consider an example to understand the working of this rider.

Ranveer takes a policy for his little girl when she turned 6. He took the policy for 15 years so that when his child turns 21 and starts his higher education, he would have enough funds to cover it.

However, Ranveer loses his life in an accident. At the time of his death policy still had five years’ premium due.

Since he had opted for a waiver of premium rider, the remaining premiums were waived off for the family.

Now the insurance company will take care of them. The policy will continue and his child will receive maturity benefits when he turns 21.

The waiver of premium has the following benefits

Child plans from Canara HSBC Life Insurance, such as promise4growth plus, offer this rider.

Both these plans have Premium Funding Benefit. Here the company will itself pay the premiums that remain to be paid after your demise and that too in the same premium payment mode.

Additionally, both plans offer diversified investment options for your child’s future.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.