Written by : Knowledge Centre Team

2026-07-28

1261 Views

5 minutes read

Share

There is a saying that remains relevant even in today’s fast-moving and modern world. The arrival of a newborn in any family brings an abundance of love, warmth, and happiness. More importantly, it also introduces a deep sense of responsibility. It changes your perspective, encourages greater seriousness, and helps you focus better on the future.

After all, this little life depends on you for every step forward. Whether it is learning to walk, speak, or understand the world, your child looks up to you for support, care, and guidance. Each moment becomes a milestone, and your role as a parent becomes more meaningful than ever. The joy is unmatched, but so is the responsibility that comes with it.

These early stages of a child’s life set the foundation for everything ahead, which makes your involvement not just important but truly life-shaping. Let us move forward to understand these responsibilities for a newborn baby and where an insurance policy enters the picture.

Key Takeaways

|

A parent’s role is to shower love and affection on the child, besides providing for the necessities for the overall well-being of the child. Whilst it is understandable that these responsibilities exist, there are financial duties as well. Therefore, proper financial planning is required to ensure that your child leads a reasonably comfortable life.

For example, a newborn baby will need a comfortable place where they can be cared for. Nutritious baby food, hygiene, and round-the-clock support are what is essential at this stage. As the child grows, you will have to account for expenses on bicycles, toys, sports items, and so on.

Needless to say, education and quality schooling will form a good chunk of the expenses (and probably your income) in the initial 10-15 years. During this phase, you would also mostly be building your career, and your income would see a modest growth year on year.

Children are more aspirational than ever because of the advent of technology and the shrinking of geographical barriers. Dreaming of studying in a different city, state, country, or even continent is no longer a distant dream. Applications can be made at the click of a button, interviews can be done online, or even in several Indian cities.

With stiff competition for the best jobs, post-graduation is the minimum any aspirational student aims for. Studying for top undergraduate and postgraduate programs in technology or management may require a total budget in the range of ₹30 lakh to ₹50 lakh.

You will certainly not want to restrict your child from applying to a program or university of his/her choice. Planning early could help build a corpus by the time the child is old enough to set foot inside a university.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Apart from constant attention, efforts, supervision, and planning, what is also essential is building a financial cover to protect against risks. Until now, your term insurance plan, such as iSelect Smart360 Term Plan by Canara HSBC Life Insurance, would have offered a sum assured that could take care of your loved ones. But what now?

Now that you have a new member in the family. Insurance policies, like iSelect Smart360 Term Plan by Canara HSBC Life Insurance, give you the flexibility to increase the sum assured at different life stages and milestones in life. With this plan, you can increase the sum assured at different stages of life, including marriage, the birth of a child, and/or on the purchase of a house. On the birth of a child, 25% or the required percentage of the sum assured can be increased, thus giving an additional safety net and peace of mind.

Click Here to use Term Insurance Calculator

A child needs constant attention, supervision, and guidance even as they grow up from being a toddler to an adolescent ready to take on the world. What else is also needed is solid financial support throughout this journey until they become financially independent. They have an excellent career track record and bright prospects ahead, but what about life’s what-ifs?

Your planning should also factor in life’s uncertainties and ensure your insurance policy for the newborn remains unaffected under any circumstances. Term insurance is helpful to provide financial protection at affordable, economical premiums. Now your child’s future will be secure and unaffected even during unfortunate times. Here are a few advantages of buying a term insurance as a children’s savings plan:

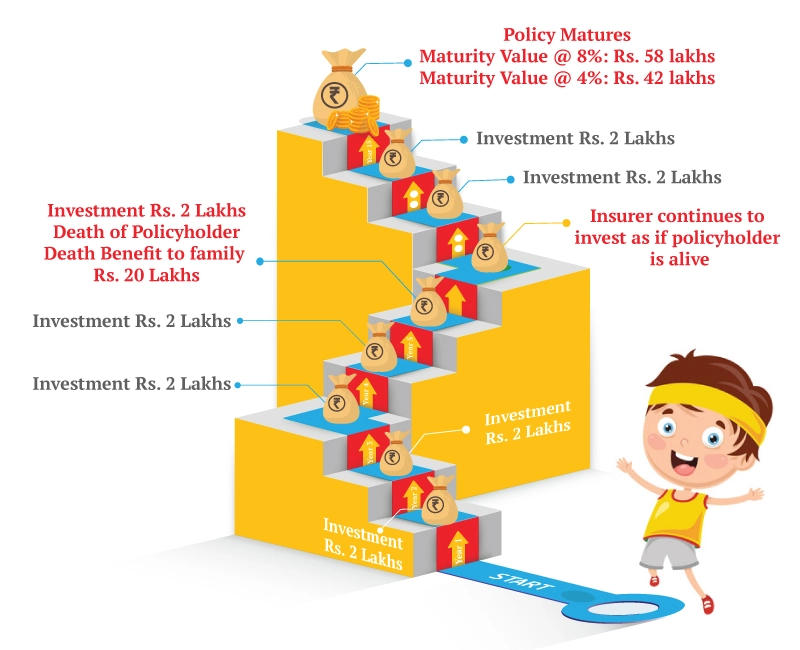

You may invest in any of these if you are risk-averse and are happy with modest returns. If you are starting early and are aspiring to build wealth, derive the benefit of these investment plans. All of these plans offer tax-exempt maturity values and tax deductions of up to ₹1.5 lakh on annual investment.

A child plan has one unique feature over others, as it also protects a child’s goal from the policyholder’s untimely demise. Finally, your child receives the maturity proceeds once the policy term is over to meet his/her goals.

Planning for the child’s future is quite essential, and starting early gives you both peace of mind and better returns on investment. A smart financial plan begins with the right life insurance that protects your child’s dreams, even during unfortunate times. Such savings plans offer the security and flexibility needed to safeguard your child’s milestones, both expected and unforeseen. It is always wise to start early and plan with care.

At Canara HSBC Life Insurance, we offer tailored solutions to meet your requirements. Plans such as iSelect Smart360 Term Plan, iSelect Guaranteed Future Plus, etc., by Canara HSBC Life Insurance, meet these needs. These plans are designed to help you build a strong foundation for your child’s future with consistent investment and insurance benefits.

Secure your child’s future today with the right mix of protection and growth opportunities.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.