Written by : Knowledge Centre Team

2026-07-28

912 Views

8 minutes read

Share

Among the most life-changing events in any individual’s life is the arrival of a child, or becoming a parent. Suddenly, you are responsible for a new member in your family and you have to provide entirely for their upbringing. It simply means that you are not only responsible for yourself, but also for the child, who, in turn, is completely dependent upon you. But a key aspect in having a child is the requirement and planning of finances. In fact with the manifold financial expenses in raising a child, you should save for your child, or have a viable child plan, right at the stage where you are planning for the child.

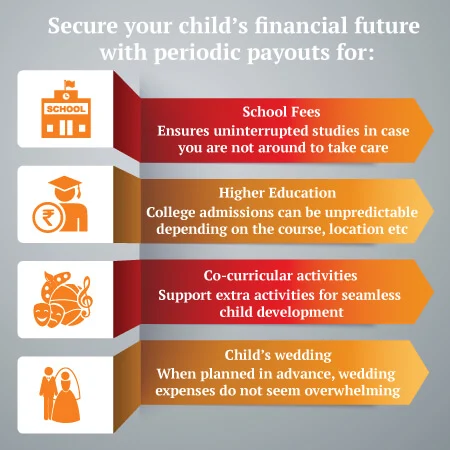

Cost involved in raising a child: According to estimates, the cost involved in raising children - from their infancy to becoming an adult - are quite high for an average family. While as an infant there is the cost of medicines and vaccines are unavoidable, once the child goes to school, you have to incur the cost of education and other related expenses. Once the child is a teenager, there is an increase in lifestyle expenses, and the question of the cost of higher education looms large. Meeting the cost of child’s life-stage goals such as marriage also becomes a financial goal for a parent

To save for your child’s future is a crucial financial goal for any parent. Many parents remain in a fix about the suitable investment avenues or child plans. But market experts suggest conducting a thorough research and step-by-step planning for zeroing in on a viable investment instrument. It is precisely at this stage that a child based ULIPcan help you tide over the problem of getting the requisite finances for your child’s future. A ULIP is an investment cum life insurance plan, providing the dual benefits of market-linked returns and protection of life cover. A ULIP child plan can help you meet a wide slew of financial requirements, from the cost of higher education to meeting the child’s life-stage goals, like marriage.

Other benefits of ULIP child plan: Here is a list of other benefits that you get from a child based ULIP:

Thus, if you are planning for a child, then start planning for its future by investing in child plans ULIPs. You must conduct a thorough market research before selecting to invest in a ULIP. Apart from the Promise4Growth Plus ULIP, a good option to consider investing in is the Guaranteed Savings Plan which provides an option to customize your savings horizon to suit your important financial goals, among other benefits.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.