Written by : Knowledge Center Team

2025-11-11

1188 Views

7 minutes read

Share

Your little whiz kids must be having certain dreams in their lives, such as becoming a lawyer, choreographer, actor, or athlete. Unquestionably, such high-flying goals require a great deal of effort, lots of dedication, commitment and above all, adequacy of funds at the right time.

It can’t be negated that cut-throat competition and inflation together have posed a tough challenge in child’s education as well.

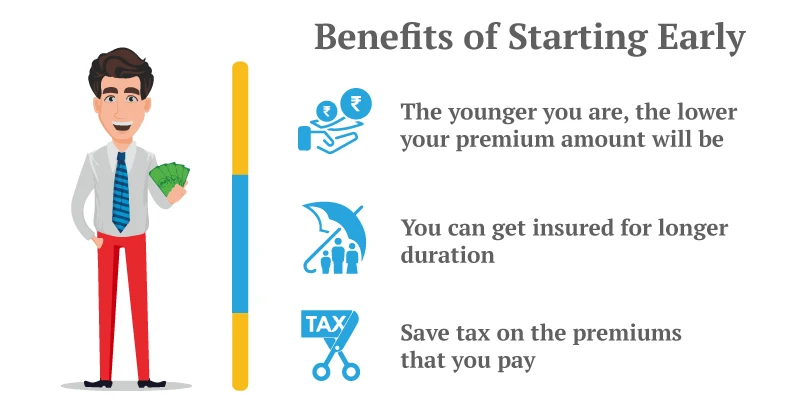

Now, the question is, ‘how do you build enough corpus for the long-term education goals of your child?’

This is where the SMART approach comes into play. Follow the SMART money mantras to build a safe future for your child.

SMART money mantras refer to a series of steps that will help you automate wealth building. You can turn your income into savings, savings into investment and investments into wealth using the SMART model of goal planning.

SMART is an acronym for

The SMART approach introduces you to these fundamental ‘golden rules of financial management. It motivates you to start saving now so that you get more time for your money to grow at a compounding rate. Eventually, you will attain ultimate financial independence to fulfil your goals.

Here are the 5 SMART Money Mantras of financial planning, explained in detail:

However, with plans like child insurance ULIPs, you can automate monitoring. These plans offer automatic portfolio strategies to help you manage your investment according to market performance.

So, your money continues to work in your favour even when you are not looking.

Following this ratio in your monthly budget will allow you to maximize your savings. Regular savings is important if you want to achieve bigger financial goals in life.

Few ULIPs offer systematic withdrawal options after the lock-in period. Money-back plans return the invested money every few years with maturity value coming back with the bonuses. Thus, these plans can help you fulfil regular or annual financial needs.

For instance, you can avail of the deduction on bonus amount at the policy-end under section 10(10d) of Income Tax Act, in addition to the 80c deduction in your child insurance plan.

A child insurance plan is one of the best saving plans for your child’s important milestones in life. A good child plan will ensure that your savings and efforts bear fruits and support your child’s ambitions financially as per your plan.

Here are the important benefits and features of a child insurance plan which also support the SMART approach:

A good child’s future plan has a unique feature called the Premium Protection option. Canara HSBC Life Insurance Guaranteed Savings Plan comes with this feature.

In case of your untimely demise:

So, while you need to invest regularly as per policy rules while you are alive, the policy investment continues even after your death. This way, your child education plan will continue till the end.

Child ULIPs offer the option of partial withdrawal from the policy after the lock-in period. Other plans have their unique features to allow you to use the corpus before maturity:

This way, a child plan allows you to “reap benefits” as per your own preferred method.

This is unique that comes in a ULIP Child plan. Here, you can choose your ideal portfolio ratio among the equity, debt, mutual funds and hybrid-fund avenues. Moreover, you can realign your portfolio using the unique auto-rebalancing strategy. This way, you will be able to use all the market speculations to your utmost financial gains. No doubt, you will be able to “monitor your growth regularly” in a very easy way.

Keeping the 5 golden money mantras of financial planning, you can build adequate wealth to support your child’s dreams. Child plans are a perfect tool to accomplish this easily.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.