Written by : Knowledge Centre Team

2025-08-06

1593 Views

12 minutes read

Share

Children are full of possibilities and aspirations. As a parent, you would want to make sure they can achieve whatever they want to do. Higher education plays a major role in ensuring a brighter future for your child.

Irrespective of what stream your child has opted for, a good university and a reliable course will ensure your child’s secure future. As a parent, your prime responsibility is to make sure your children can receive the higher education they need to build their successful careers. You can kick start securing your child’s future with the best child insurance plan.

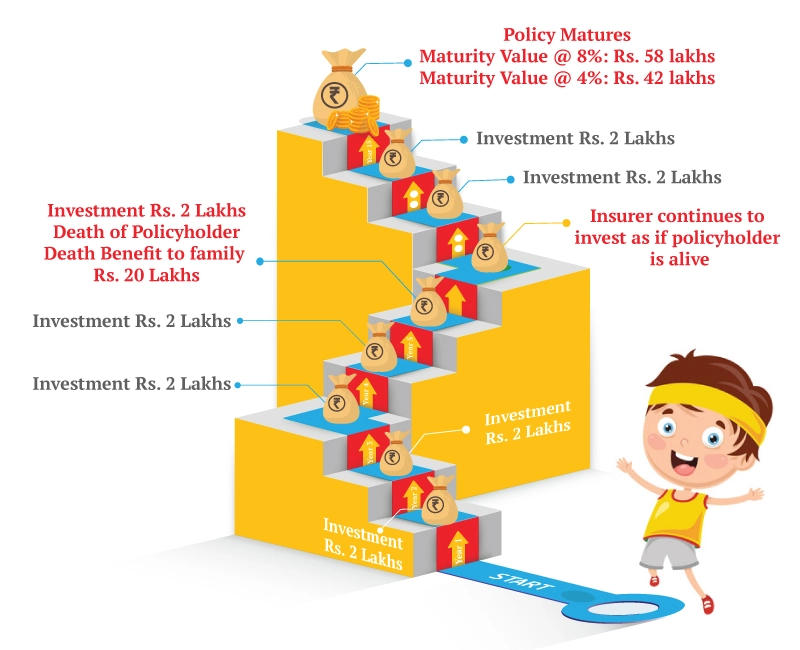

Child ULIP and endowment life plans are the types of investments that can protect the goal during your life and even after your demise.

Promise4Growth Plus ULIP offers the following two Bonuses:

Now you can easily decide what is the best investment for a child's education.

The cost of education has been one of the fastest-growing expenses in India. The average cost of an engineering course in India from a reputed institution can go up to ₹ 5 Lakhs per annum. The fee for private colleges is even higher than the public ones.

Here is an estimate of the educational cost, if your child enrols into a 4-year engineering course in any stream:

Learn how to plan for the best higher education of your child.

Now, if you compound all these costs with the inflation rate, the amounts will grow to be much higher in 10 years. The inflation rate in higher education has been about 5 – 10% p.a. in India and 3 to 5% p.a. in more developed countries.

Thus, you not only need a good investment option to beat inflation as well as tide over the taxes, but you also need to protect the goal. You can do so, by either:

or

Various investment instruments can work as a child education plan. Depending upon your risk appetite, you can invest in different instruments:

You need to safeguard your savings from the three risks - inflation, taxes and market volatility. Thus, you have the option of investing in the following:

All three options offer safe and tax-free growth to your money. However, there are a few limitations there:

If your investment risk appetite allows, you may want to aim for higher growth for the investment term. Equity is one of the most promising and well-regulated aggressive investments. Here’s how you can allocate your money to equities:

Buying a child insurance plan will ensure that your children will not face any financial worries if something happens to you. Life is pretty unpredictable and hence, you should be prepared to protect those who you love.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.