Written by : Knowledge Centre Team

2026-07-28

1340 Views

11 minutes read

Share

The best jobs go to the most qualified people. This liner means much more in today’s hypercompetitive world that has millions of well-qualified people entering the workforce each year. To remain ahead, candidates constantly upgrade themselves with better skills, the latest qualifications, and training programs. With increasing awareness about the importance of education, this number is only set to increase over the decades. And getting quality education means investing money. Either people buy child insurance plans or they opt for education loans.

An undergraduate degree may no longer suffice to demonstrate deep expertise in the chosen field. Industry practitioners are going one step ahead of a master’s degree and opting for the intensive PhD program. As a parent, you must draw a child education plan to support him/her until s/he attains a post-graduate degree at a University of repute.

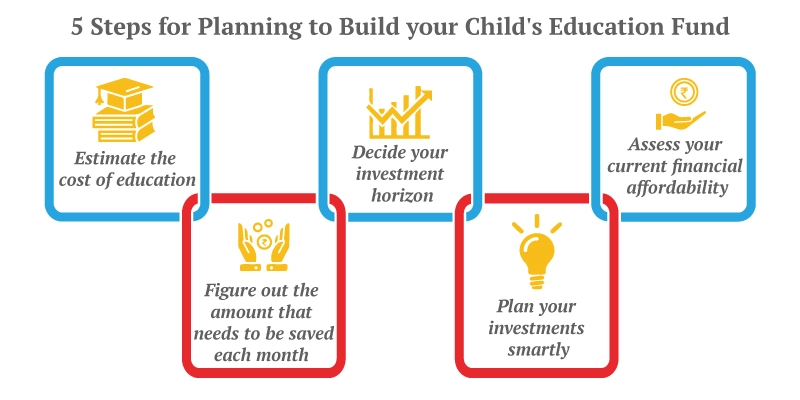

Higher education has to be planned more meticulously because this is the stage at which your child will opt for super-specialization and this will define his core niche/expertise. Following some of these broad guidelines could help you make a wise choice.

Institutions that figure in one list may not figure in another because each list has its focus area (public universities, deemed universities, technical colleges, B-Schools, etc) and also based on the college’s interest to disclose details and participate. NAAC, NIRF are some of the government-backed ratings in India.

The quality of the institution signals brilliance creates a positive perception and increases acceptance. This opens many doors more quickly for the candidate. In healthcare, the doctor’s alma mater gives the initial confidence to trust his/her ability to deal with human life. After all, would you like to risk your life in the hands of a doctor who graduated from an unknown college on a remote island?

Here’s everything you should know about a child insurance plan.

In 15 years, factoring in inflation, these courses would cost in the range of Rs. 30 Lakhs to Rs. 70 Lakhs. You can work backwards to save or invest to reach this figure.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

These plans allow you to invest in a mix of equity and debt instruments so that you can take advantage of market movements and benefit from equity growth

The plans have many features to help you benefit from the market growth, even when you are not following the markets continuously:

You may want to safeguard your goal, not only from the uncertainties of life but also from the uncertainties of financial markets. You can invest in any of the following:

Investment in insurance policies gives you the comprehensive benefit of investment, insurance cover, and tax deduction. The life cover assures you that your family will still educate the child, as planned, if, unfortunately, you are not around then.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.