Written by : Knowledge Centre Team

2025-12-20

897 Views

8 minutes read

Share

Are you working on retirement planning for Rs. 5 Crore and working towards creating this retirement corpus? If yes, you are on the right path to building a sustainable future for yourself and your family. But will Rs. 5 Crore be sufficient? It depends on a multitude of factors such as your age, lifestyle, current and projected expenses etc. It also depends on how much can you save diligently to build your retirement kitty.

If you currently lead a modest lifestyle, you will most probably continue the same even post-retirement.

Most organizations have a mandatory retirement age. Even if your health permits you may not be allowed to continue working full-time. Income ceases to exist post-retirement. You will have to still manage your household expenses. Paying bills is possible only if you have a sufficient retirement corpus that can keep giving you cash flows for the rest of your life.

Look at the factors that should shape the size of your retirement corpus:

Let’s say Ramesh is a 30-year-old married man bound to retire at 60. He invests in different asset classes and anticipates a cumulative 12% rate of interest per annum. The inflation rate is hovering at ~ 6%. His monthly expenses are Rs. 50,000 besides an annual expenditure of Rs. 1,00,000 on health and vacation. He expects his expenses to reduce to 75% of his current expenses post-retirement.

Ramesh needs ~ Rs. 5 Cr on retirement. He can either invest ~Rs. 15 lakhs as a lump sum one-time investment or invest ~ Rs. 1.7 lakhs annually for the next 30 years. He can also choose to invest ~ Rs. 15,000 each month for the next 30 years to reach his financial goal.

Once you have made an approximate budget of how much you may need then, you must carefully evaluate investment options. Some popular options that are used for long-term plans are listed below:

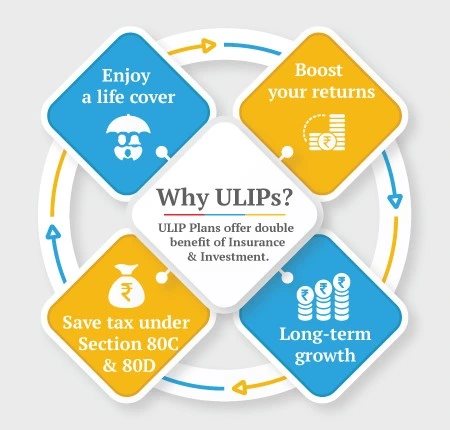

ULIPs are solid investment options because you can choose to put your money in diverse funds. Early exposure to equity can help you generate wealth. When you inch closer to retirement, move your money to debt funds to preserve capital. The returns from ULIPs are exempt from tax under section 10(10D).

ULIPs like Invest 4G from Canara HSBC Life Insurance allow you to continue your plan till the age of 99. This means you can use the same plan to build a retirement corpus and withdraw your pension. This pension will enjoy tax exemption under section 10(10D) of the Income Tax Act, 1961.

PPF stands for Public Provident Fund. It is a sovereign guaranteed investment and comes with tax benefits. PPF offers a 7.1% rate of interest. The amount deposited in PPF accounts is deductible, under Section 80C, from taxable income whereas all withdrawals are exempt from taxes. Partial withdrawals are allowed from the 7th year.

NPS stands for National Pension Scheme. Investments in NPS are exempt from taxes both at maturity and annuity (up to 40%) stages. On retirement, you can withdraw 60% of the accumulated corpus and choose to avail pension from the balance of 40%. Contributions to NPS are deductible, under sections 80C section 80CCD(1b), from taxable income.

Ageing is an irreversible process. Your health, as well as your financial health, are both equally important. Ideally, you should start saving for retirement as soon as you start working. This helps you to invest small amounts and build a huge corpus such as Rs.5 Crore. Basis the retirement age, the monthly investment should also be calculated. This will ensure you remain in a comfortable financial position when you hang up your boots.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.