Written by : Knowledge Centre Team

2025-07-05

4878 Views

7 minutes read

Share

Life does not come with guarantees. For most of us, family is our priority. You should always have plans to protect them financially under all circumstances. When you do financial planning, you create goals for yourself to give the best life to your loved ones.

You have to take care of your parents, your children's education, marriage, and build a retirement corpus for yourself and your spouse. If you pass away, your family will not only go through mental stress but also financial stress.

Term insurance is the simplest form of life insurance that financially protects your family if you pass away during the policy term. It ensures the dreams you have envisioned for your loved ones are fulfilled, whether you are with them or not. Choosing the right term plan helps secure your entire family's future, giving you peace of mind today.

Key Takeaways

|

You can buy a term insurance plan at an affordable price and get a high sum assured under the plan. You can buy a term insurance plan based on your liabilities and your annual income. The term plan should ideally be at least 15 to 20 times your annual income. If you have an existing loan, like a home loan, you should factor in the loan amount while choosing a cover.

For example, if you have a home loan of ₹50 lakh, and your annual expenses are ₹6 lakh, you should opt for a cover of ₹1.5 crore. In the event of your death, the sum assured will be paid to your beneficiary as a lump sum amount.

Your spouse or other nominee receives the benefit amount, which they can use for:

In this way, term insurance covers your family and loved ones in your absence.

Times have changed, and now the man is no longer the only breadwinner of the family. More and more women are working, and the households today are dependent on the income of both partners.

Let us take an example of Mr Shah's family. Mr Shah has taken a home loan, and a large part of his salary goes into paying the EMIs, while the rest he saves for future financial goals. Mrs Shah is also working, and she takes care of household expenses.

In the above example, both are equally important in running the household and achieving future goals. In such cases, you must take out a term insurance plan to cover your spouse too. If something happens to either of you, your partner and other family members can maintain the same standard of living. You can either opt for a joint term insurance plan or buy separate term plans for yourself and your spouse.

Yes, a term plan can benefit a buyer. To understand how, let us look at the types of term insurance plans you can opt for:

For example, if you purchase a 30-year term plan with a return of premium option, covering ₹50 lakh and costing ₹12,000 annually, you will receive ₹3,60,000 upon policy maturity after 30 years. In case of your unfortunate death during the policy term, the beneficiary will receive ₹50 lakh.

If you want to provide the best term insurance cover to your family, you need to look for a few features in the plan. For example, iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers multiple benefits to your family in a single term plan:

Depending on your needs, you can choose a lump sum of 25%, 50%, or 75%. For example, if the cover amount is ₹1 crore and you have a home loan of ₹50 lakh, 50% can be taken as a lump sum, and the remaining amount as monthly income.

You Get Built-In Riders: The iSelect Smart360 Term Plan is one of those term plans that offers a terminal illness insurance benefit as a default option with the life cover. Thus, if you are diagnosed with a terminal illness, the plan will release the funds to support your treatment costs.

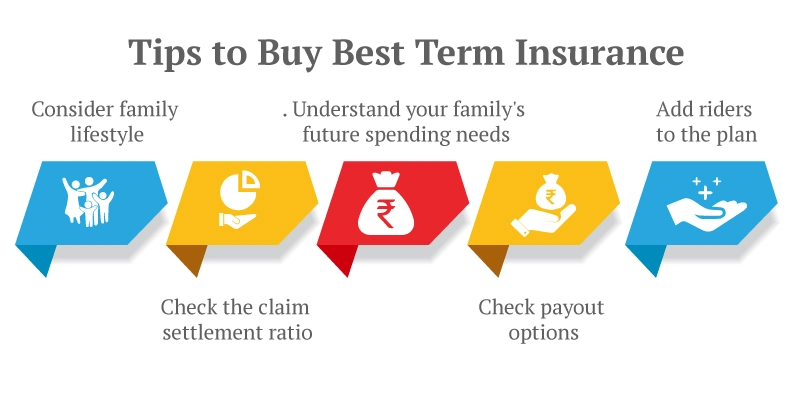

Your term insurance sum assured should fully protect your family’s lifestyle and future goals if you are not there to support them. Here are some key factors to consider:

Cover All Liabilities: Add up your existing debts like home loans, car loans, or personal loans. Your insurance should be enough to clear these so your family does not face repayments alone.

Replace Your Income: Choose a cover that is at least 15 to 20 times your annual income. This helps replace your income and maintain your family’s standard of living for years.

Plan for Children’s Future Needs: Think ahead to big expenses such as your children’s school fees, higher education, or marriage costs. Include these in your total cover.

Consider Daily Living Costs: Factor in your family’s monthly household expenses, such as food, utilities, and healthcare, for the years they might rely on this cover.

Account for Inflation: Always remember that expenses increase over time. It’s wise to add an extra amount to keep up with rising costs.

Review Regularly: As your income, loans, or family needs change, revisit your cover to make sure it stays relevant.

For example, if you earn ₹10 lakh a year, have a home loan of ₹40 lakh, and expect to spend around ₹30 lakh for your children’s future, a suitable sum assured could be about ₹2 crore. This ensures your family can manage daily expenses, repay loans, and achieve life goals even in your absence.

When you buy a term plan, you do it for your family and their secure future. By paying a small premium, you provide them with financial security and peace of mind. Many people wait for the so-called right age to buy term insurance. First waiting to get married, then to have children. But the truth is, there is no perfect age. There is only the right time, and that time is now.

Securing a term insurance plan today means your loved ones are protected from life’s uncertainties, no matter what happens tomorrow. So, choose a reliable plan, calculate the right sum assured, and invest in your family’s future security, because nothing is more important than their peace of mind.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.