Written by : Knowledge Centre Team

2025-08-02

1094 Views

8 minutes read

Share

In today’s day and age, women are taking up more responsibilities in life and working towards being financially secure. Contrary to the common belief, women nowadays are more focused on maximizing their earnings through investments and have become savvier about choosing saving plans and making tax decisions. As a result, more and more households in India are becoming double-income to tackle the increasing inflation and tax liability.

With more and more women taking center-stage in the financial decision-making for the family, we are witnessing an age of changing mindsets towards financial sustainability. Read and learn more in this blog on how women can procure financial benefits in today’s time.

Key Takeaways

|

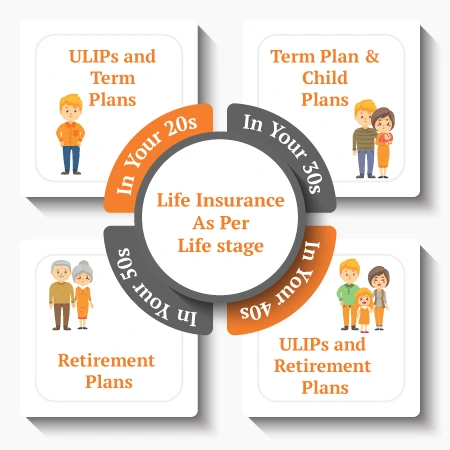

Every decade of your life brings new responsibilities and financial goals. Understanding where to invest and what to prioritise at each stage helps build long-term financial security with confidence. Here’s how women can plan their finances better in their 20s, 30s, and 40s.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

At this age, as you near your retirement, it is advisable that you start shifting some of your riskier investments to less-risky avenues such as debt mutual funds and bank fixed deposits (FDs) while keeping a portion of your equity investments. Also, it is prudent that you make sure to set up different sources of income to support your lifestyle needs post-retirement by opting for monthly income plans, Public Provident Fund (PPF), and Senior Citizen Savings Scheme (SCSS) once you turn 60.

By purchasing the right investment options at an appropriate age will help keep yourself and your family financially secure.

Early financial planning prepares women for the unexpected. Simple routines of maintaining monthly budgets, monitoring expenditure, initiating automatic investments such as SIPs, and becoming familiar with financial products give them confidence and security. These routines not only increase your savings but also enable you to make independent decisions throughout life.

With growing financial awareness and increasing responsibilities, women today need smart investment options that offer both safety and growth for their unique life goals. Listed below are some investment options:

1. Savings Bank Account:

Several banks in India offer ‘women’s savings accounts’ that provide cash-backs and discounts to women who spend on wellness, shopping, food, and entertainment through the bank’s debit card. With a savings bank account, both working women and homemakers can avail of earnings while they spend. Additionally, there are discounts offered to women who opt for medical tests specific to female health, so that women prioritise their health and well-being. You can also open a ‘Junior Account’ to fund their children’s education, and link the account to a Recurring Deposit (RD) or a Systematic Investment Plan (SIP) so that there is no minimum balance requirement for the savings bank account.

2. Health and Life Insurance Plans:

As a woman, you can benefit from the available medical insurance schemes and dedicated premium rates customised to suit female health needs. At the same time, life insurance companies offer personalised financial coverage to women, keeping women-centric health ailments such as breast cancer in focus. Thus, you can benefit by investing in a health and life insurance policy. Typically, women applicants are eligible for reduced premium rates and discounts up to a certain age. Even homemakers can now avail of term life insurance protection under their spouse’s policy, thanks to the Married Women Protection Act (MWPA).

3. ULIPs and Equity Mutual Funds:

Investment in equity mutual funds enables women to pool their funds into diversified investments taken care of by expert fund managers. This can result in better returns in the long run than plain vanilla savings. This makes them suitable for long-term goals such as retirement planning, saving for children's education, or launching a business in the future. Likewise, Unit-Linked Insurance Plans (ULIPs) combine insurance and investment in a single plan. A portion of your premium provides life cover, and the remaining amount is invested in equity or debt funds depending on the amount of risk you can bear. ULIPs are tax-efficient and enable the creation of a stable, goal-based wealth over the years.

4. Recurring Deposits and Fixed Deposits:

Recurring Deposits (RDs) are perfect for women who like to save money gradually. You can deposit a fixed amount of money every month and take a higher amount with interest when the term ends. This makes RDs ideal for building an emergency fund or saving for short-term expenses like annual insurance premiums or vacations. Fixed deposits (FDs), on the other hand, enable you to deposit a huge amount of money for a specific period, and you get a fixed rate of interest. FDs are low-risk investments that provide you with guaranteed returns, keep your capital safe, and provide you with options to withdraw your money. This makes FDs a favourite among women who like stability and security in their savings.

In India, women nowadays play an essential part in their family’s well-being, both emotionally and financially. Both working and homemakers are becoming increasingly aware of their needs for financial stability. There are various investment options and schemes that help women become empowered and support their lives financially while looking after their health and family.

By understanding and choosing the right investment options at every stage of life, women can build financial independence with confidence. At Canara HSBC Life Insurance, we offer a wide range of insurance and investment plans designed to empower women with financial security, tax benefits, and peace of mind for a stable and fulfilling future.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.