Written by : Knowledge Centre Team

2025-08-02

1188 Views

11 minutes read

Share

It’s terrible when we fall into a drastic income cut due to unexpected situations like Covid-19 and do not have an emergency corpus to take care of our contingencies. Many people have had to face hardships on the money front in this pandemic. But as they say, it is never too late. People who have missed out on building an emergency corpus could create one in the months ahead through systematic planning.

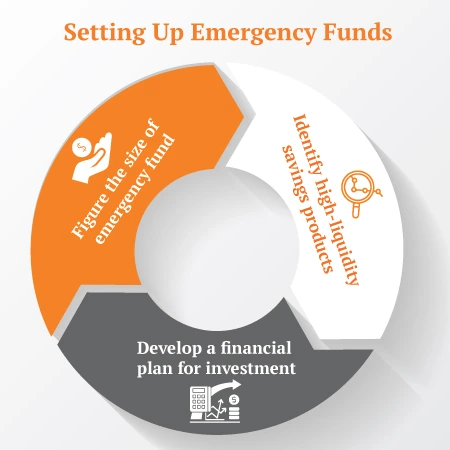

An emergency corpus is critical in uncertain times and with an emergency corpus in place, you could live worry free. Many investors get carried away by the promise of higher returns on equity and end up never building an emergency corpus for themselves. An emergency fund can be in form - from sufficient deposits in a savings account, to a unit linked insurance plan that allows pre-withdrawals in times of emergency. Ensure whatever the source be, it is accessible in a day or two to help in any crisis, should you face a sudden dip in earnings from disruptions due to a market shutdown, natural calamity etc. Such emergency corpus can help pay for major expenses like children’s education, an equated monthly installment or even usual household expenses, if needed.

Depending on your income and regular expenses, an emergency fund can be anything between three to six months of your monthly income. If you plan to start an emergency fund now, take account of the amount of money you need for your living expenses, money payable towards school fees, EMIs payable, and other unavoidable expenses. Also, it is advised you review these every few months to monitor and incorporate any increase in expenses. You may even choose to divide your emergency fund into 2 categories, and choose saving instruments accordingly.

Health and term insurance are a must to ensure a secure financial future for your family. In addition, unit-linked insurance policies (ULIP) that promise to pay returns at the end of the tenure are also considerable options. Apart from financial security, insurance policies are also a smart way to build wealth. While investment options such as equity and mutual funds play an important role in long-term wealth creation, there are several plans that can help fulfill both cover and savings needs.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.