Written by : Knowledge Centre Team

2025-11-05

985 Views

5 minutes read

Share

You have made up your mind to include life insurance in your investment portfolio. You want to now go ahead and apply for life insurance but are unsure of how to buy a life insurance policy. Who should you speak to or what should you do next? Most net savvy people will immediately log online and compare on policy aggregator sites or go straight to the insurer’s site to understand the life insurance application procedure.

Buying an insurance policy has never been as easy as it is now. Some of the channels to sign up for a life insurance policy are listed below:

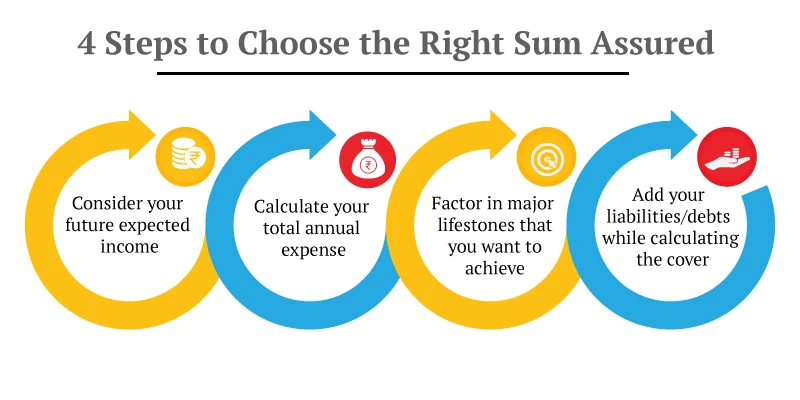

| Sum Assured Sum Assured (SA) is the guaranteed, fixed, lump sum amount payable to your nominee in case of your demise. SA is also used in endowment plans to indicate the guaranteed, fixed, lump sum amount payable to you on the maturity of the policy. | |

| Nominee The person named, by you, to receive the SA and/or Funds from your investment in case of your demise. | Riders A feature in a life insurance policy that either provides additional coverage or add-on benefits/ |

| Bonus The profit made by insurance companies, by investing the premiums in bonds/debt instruments, is distributed amongst policyholders. | Surrender Value The amount receivable if you decide to exit the policy before the maturity date. Surrendering is possible only after the lock-in period if any. |

If you are concerned about your post-retired life, you must explore pension plans and wealth preservation techniques alongside growth. GuaranteedIncome4Life and Guaranteed Savings Plan pay out fixed cash flows after investing for defined payment terms.

The undisputable option for wealth creation is Promise4Growth Plus that allows you to automatically rebalance your portfolio depending on your pre-defined equity: debt allocation. You can also systematically transfer funds from one to another so that you benefit from the bull runs and conserve capital during a bear market.

If you are saving for retirement, keep at least 20% of your current income aside and invest in aggressive growth plans such as Promise4Growth Plus or deferred annuities that can give you and your spouse, Pension4Life.

The charges for undergoing the medical tests are borne by the insurer, although, in some cases, the applicant may be asked to bear the same.

Buying a life insurance policy has not been simpler at any point earlier. The procedure is simple. If you are not comfortable with technology, there are multiple offline channels to know more about the options available. The staff at the branch, your insurance advisor or even the online customer support staff can help you seamlessly navigate the process.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.