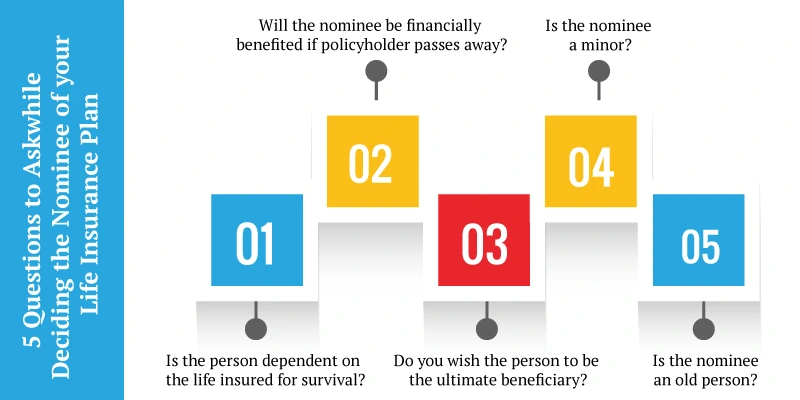

Written by : Knowledge Centre Team

2025-08-01

1272 Views

10 minutes read

Share

Life insurance helps you safeguard your family’s future. Having a life insurance policy becomes more important when there is only one breadwinner in the family, generally the male spouse. In such cases, the female spouse and the children become hugely dependent on them.

So, a life insurance policy takes care of your family when you are the only earner and something unfortunate happens to you. But what if you die with loads of debt and the proceeds from your policy go towards settling your debts?

The benefit amount can also be taken by the creditors and other family members. This will leave your spouse with no money when she will need it the most.

As the breadwinner what you can do is to buy the insurance policy under the Married Women’s Property (MWP) Act. This will ensure financial safety for your spouse.

Key Takeaways

|

If you buy your life insurance policy under the MWP act then you ensure the fact that the sum assured of the policy will go on to your wife and children only. It makes sure that their interests are the first and foremost.

Parties like creditors, relatives, etc cannot claim the amount. This is because once the policy you purchase is available under the MWP Act, it is not attached by the court for repayment of any debt that exists.

Thus, in this way, a life insurance plan under the Married Women's Property Act 1874 safeguards your wife’s and children’s financial interest even after you are gone.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

According to section 6 of the Married Women’s Property (MWP) Act:

Thus, buying a life insurance policy under this act can save your dependents from the burden of debts and family disputes.

Example:

Akshay has a business of tiles. He has taken some loans for the business. He purchased a policy under the MWP Act and named his wife the beneficiary.

After some time, he died in an accident. Now, the creditors who gave the loan to Akshay, approached the courts for them to be paid off from the assets of the family.

Although the court has attached multiple assets owned by Akshay to settle the debt, it cannot attach the MWP policy. Policy’s entire proceeds can only be used for the benefit of surviving wife and children of Akshay.

Life insurance is meant to give your family financial aid after you are gone. But in case you have outstanding loans or debts, your creditors may legally take the payout, leaving your family members with little or nothing. Here, the Married Women Property (MWP) Act comes in handy. When you buy your life insurance policy under the MWP Act, your policy proceeds will be legally secured, and the proceeds can pass only to your wife and children.

It leaves the benefits fully in the hands of your family with no outside interference, and they will be able to handle the household expenses, the education of their children and other obligations without any hassles. This is a basic but effective provision that will make your life insurance an insured security cover for your family in the future.

Now that you know what the MWP Act is, let’s look at who should buy the policy under the MWP Act.

Any married man (who has to be a resident of India) can choose to take the insurance policy under the MWP Act. This also includes the divorcees and the widowers as they can name their child in the beneficiaries.

If you have a business to run or a salaried person with ongoing loans and liabilities, then you should consider buying your policy under the MWP Act.

This can also be considered when you want to protect your wife and children from creditors and relatives who can have bad intentions.

The process to purchase any type of life insurance policy under the Married Women’s Property Act is simple and is almost the same as buying a normal life insurance policy.

When you decide to buy any insurance plan, you first have to fill out an application form. For enrolling your plan under the MWP Act, you need to fill out another form apart from the application, which will state that you will buy this policy under the MWP Act.

You then have to enter the details of the beneficiary, such as the name, your relation, and age. You may also need to decide the share in the benefit in terms of %.

Remember, the beneficiaries that you can choose under this act can only be amongst the following:

The beneficiaries once chosen by you cannot be changed at a later time. At the time of death, the policy benefits are received by the trust that is selected by you. These cannot be claimed by the debtors nor will they form the part of the estate of the policyholder. It will only be claimed by the wife/child.

Life is not predictable, and if you are the sole earning member of your family, it is your responsibility to make your family secure financially even when you are not around. Purchasing a life insurance policy under the Married Women's Property Act 1874 ensures that your wife and children receive the insurance fund without any legal complication or claim by creditors. This provides a sum that the wife can use to manage herself and her children. She can also use the death benefit received to fulfil her children’s goals, such as higher education.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.