10 Common Myths About Child Insurance Plans

Many parents overlook child insurance plans due to persistent misconceptions. Below, we debunk the top 10 myths with facts to help you make informed decisions.

Myth #1: Only Offers Insurance Cover for the Child:

Child insurance plans primarily protect the parent (policyholder), not just the child. Any insurance plan covers the income-earning person, and a child insurance plan is no exception. The policy ensures that a child’s dreams and aspirations are never let down, even in the absence of the income-earning parent.

You can also use the policy for other financial goals, such as wealth accumulation and retirement goals. For such goals, the policy will benefit your surviving partner in case of your early demise. Thus, the policy always covers the parent who is holding or buying the policy.

Myth #2: Only Beneficial When the Child Gets Enrolled for Higher Studies:

Child insurance plans offer flexibility; you're free to use the money for anything, with no conditions. This myth is prevalent because most parents buy the best child education plan to support their child’s higher education goals. Thus, the policy term is such that you receive a lump-sum amount when your child turns 18. This is the time when they would join the university for undergraduate studies.

Professional degree programs and global education are costlier than schooling. Therefore, the need for a systematic investment that grows your money over time becomes essential. However, you may choose to use the money for your child’s hobbies, entrepreneurial ideas, or even marriage.

Myth #3: Policy Terminates if the Policyholder Passes Away:

In reality, continuation is your choice; you can select this option at purchase. The "Premium Protection option" (or premium waiver benefit) ensures the plan continues, with the insurer covering future premiums to meet your financial goals.

Thus, in case of the untimely demise of the parent (policyholder), the family would get the sum assured, and the policy would continue. Future premium payments would be waived off. At the end of the policy period, the family would get the fund value.

Myth #4: It May Not Be Able to Meet Education Costs in the Future Due to Inflation:

Child plans offer equity-linked options to combat inflation effectively. You can choose child plans where you can also invest in equity funds. Equity is a high-risk, high-reward investment capable of beating inflation through long-term investment. Thus, you need the following two factors for relative safety and to enjoy growth:

Myth #5: Death Benefit is Provided Only in a Lump Sum:

Child plans offer flexible payout options beyond a single lump sum, even after the policyholder's death. Milestone-based payouts and partial withdrawals are allowed even after the untimely demise of the parent. The sum assured is paid immediately after the demise. Future premium payments are waived off to avoid burdening the family. At the end of the term, the family would receive the fund value.

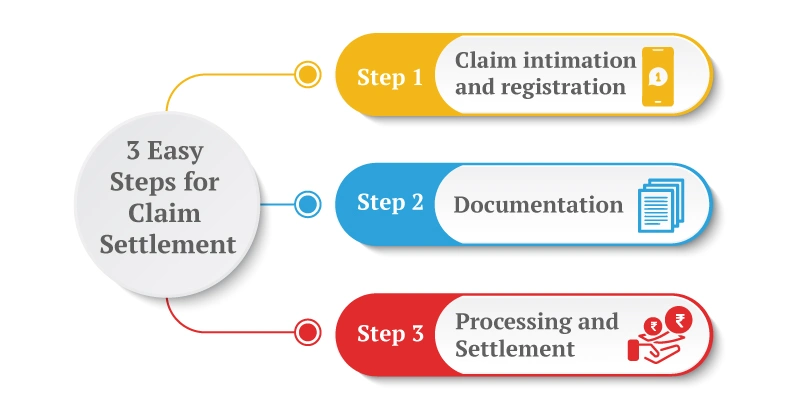

Myth #6: Claims of the Policies are Often Rejected:

In reality, child insurance claims are processed smoothly when documentation is complete, and policy terms are met. Reputable insurers maintain high claim settlement ratios, often above 98% for life plans, ensuring families receive benefits without unnecessary delays. Common rejection reasons, like missing documents or non-disclosure, are avoidable with transparency at purchase and timely claim filing. Check for settlement ratios, customer service reviews, and defined timelines before signing up for child life insurance plans in India.