Written by : Knowledge Centre Team

2026-07-28

1108 Views

7 minutes read

Share

Every parent earns to fulfil the needs of the family and future goals of their children like higher education and marriage, etc. As parents our happiness is tied to the children’s happiness and success in life. This is why you would earn, save and invest a major chunk of your income in long-term financial instruments.

Child saving plans are the best investment cum insurance plans that can ensure the financial security of children’s future goals.

Most insurers are offering child plans with market-linked and pure endowment products. ULIPs are the best investment plan for child education if you are open to investing in both debt and equity funds. Whereas a traditional endowment plan is a better option when you want a specific amount assured at maturity.

Here are five more tips that will help to choose the best child plans as per the child’s future goal:

For example, you have bought a ULIP plan with a life cover of ₹10 lakhs and an annual premium of ₹1 lakh. You want to accumulate ₹20 lakhs in 15 years and will be contributing throughout the policy term. But, in case of your demise in the seventh policy year, your family will still receive:

This feature is called the premium protection option, and it ensures continuous investments from the insurer into the plan after your demise. Thus, the investment value of the plan keeps growing until maturity.

If you want to invest in equity funds and benefit from the high-risk high-growth possibility, you need to ensure a few things:

In case you don’t feel comfortable investing in equity funds, you can still use the safer debt funds option in the ULIP child plans. However, if you are looking for a guaranteed maturity value you can consider an endowment plan.

Read more about ULIP as an investment for your child.

Endowment plans are one of the safest long-term investments. You can easily estimate your maturity value from these plans at the beginning of the investment. So, if you have a financial goal with a definite future value, these plans could be the best option for you.

For example, you want to provide a corpus of ₹15 lakhs to your daughter’s marriage 20 years from now.

Additionally, these plans provide additional bonuses for long-term investors. So, if you are investing for 30 years, you can expect better growth of your funds than if you invest only for 15.

Understand that both of these plans are life insurance plans, and life insurance plays a crucial role in their performance. For instance, both the plans will offer a sum assured of life cover, which your family will receive immediately upon your death within the policy term.

If you need the plan to add to your family’s overall life cover umbrella, the plan’s life cover should be equal to or larger than this amount. Also, the life cover amount in a plan decides how much you can invest in that plan in a financial year without losing the tax benefits.

For example, if your ULIP plan’s life cover sum assured is ₹20 lakhs, your maximum annual investment in the plan should not exceed ₹2 lakhs (10% of S.A.).

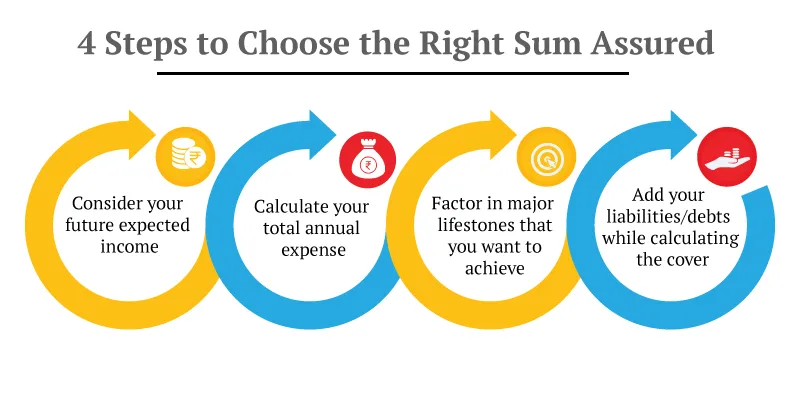

The size of the corpus you can build at the maturity of the child plan depends on the following three factors:

Premium payment term cannot exceed the policy term. But it can decide the amount of money you can invest in the plan. Thus, the premium payment term is an important factor to consider if you wish to achieve bigger goals.

The ULIP plan offers automatic portfolio management strategies for aggressive investors. So that, you can manage your portfolio risk and allocation even when you are not looking into it.

So, if you have enough time on your side, why not give equity a chance to boost your funds over time with the right investment plan.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.