Written by : Knowledge Centre Team

2025-12-20

1086 Views

8 minutes read

Share

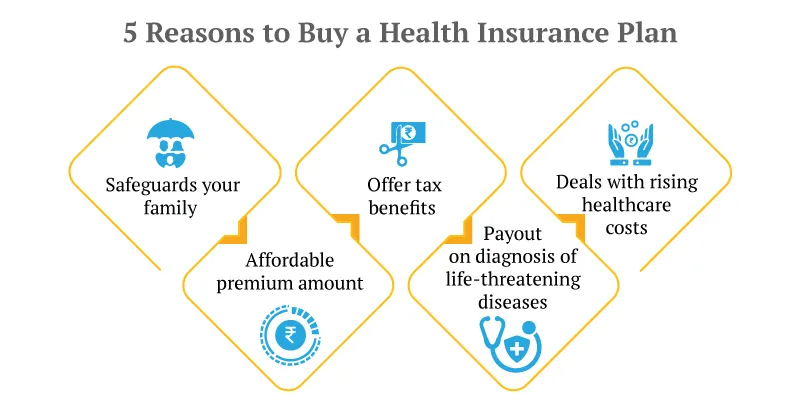

Health insurance, as the name suggests, helps you financially against all kinds of health issues, or at least that is the expectation. However, health insurance is designed to work as a tool to bring your financial life back on track after an emergency:

Before you discard your existing health cover and start looking for one that covers IVF costs, understand if you need it. In medical terms, IVF is a way to resolve pregnancy woes. That means IVF itself is not a medical condition and doesn’t put you at major health risk.

However, the purpose of IVF is a successful pregnancy, that is, childbirth.

Childbirth or maternity expenses are covered by almost every family floater health insurance plan. Even better, your employer’s group medical insurance would offer to help with the maternity costs.

So, while IVF itself is not a health risk, your health insurance will cover any side effects of IVF and related medical costs.

Also Read about Cashless Treatment

Although IVF is not covered by insurance, there are certain risks involved in IVF treatment that can be covered if you have an insurance plan. Here are some of those risks:

The mentioned risks can affect the life of the mother who is undergoing IVF treatment.

You will find two different kinds of medical issues or illnesses – one which requires hospitalisation, or surgery and medication for recovery, and two which could be life-threatening even with treatment.

There are two different types of health insurance plans:

The health insurance coverage you have for your entire family and the Mediclaim cover you receive through your employer fall into this category. Defined contribution means the premium cost for health insurance is defined. However, the benefit will depend on the actual expense.

The cost of IVF and similar treatments, if covered, will fall under this type of health insurance plan.

A little less popular, yet equally important, these plans help you against life-threatening illnesses like cancer. This is why they are also called critical health insurance plans. You can buy a critical health cover as a rider with your term or health insurance plan.

These health plans have a defined benefit amount, meaning you will receive a fixed sum upon diagnosis of a covered illness. The amount you spend on treatment doesn’t affect your benefit from the plan.

Since IVF treatment is not a life-threatening situation, critical health plans are unlikely to cover this cost or condition.

You can cover maternity and related expenses with a family floater health cover (defined contribution plan). These plans will also cover the newborn from day one.

With critical health insurance you have a few options:

Term insurance plans generally include terminal health cover by default. So, the term insurance plan works both as a life cover and critical health cover.

If you decide to buy critical health cover separately, you have the following three options:

Ideally, your contingency portfolio should include both plans.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

You need to look for the following features in critical health insurance:

This will take care of the ongoing health and medical expenses involved in cancer treatment. Hence, you can easily get cancer treatment without any financial burden.

If you opt for this feature, the premiums after the death of the policyholder shall be paid by the Insurance Company. The term plan won’t end after the policyholder’s death and will continue till full term.

As far as your financial needs go, health insurance must be on priority. Whether you are looking for IVF cover or not, a family floater and critical health are must have covers. These life insurance plans will ensure long-term financial safety for your family.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.