Written by : Knowledge Centre Team

2025-08-02

897 Views

8 minutes read

Share

The difference between life insurance and life assurance is so subtle that it’s easy to confuse them as one of the same thing. You and your spouse have dreamt of so many life goals such as building a house, educating your children, and so on. You are diligently saving towards your goals, but you are keen to mitigate risks so that your family gets a financial safety net even in your absence.

Key Takeaways

|

But before you decide between life insurance and assurance as to which option best suits your needs, it’s important to understand what each one actually means. Both offer financial protection, but in slightly different ways. Let’s start by understanding what life insurance is and how it works.

If you sign up for life insurance, the insurance company will issue a policy to you promising to pay a pre-fixed amount to your nominee in case of your unfortunate demise.

In return for this promise, you must pay nominal amounts, called “premiums”, periodically from the date of signing up for such a policy.

The insurance amount “promised” by the insurance company is called “life insurance coverage” or “sum assured” and is generally ten times your annual income. This amount ensures that your family is not deprived of necessities, in your absence.

Life assurance covers you for life. It is more popularly called the “whole life policy”. Life assurance policies have 2 key benefits:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Both life insurance and life assurance are risk mitigation instruments and pay out a fixed amount after your demise. So, the risk cover is guaranteed.

| Parameter | Life Insurance | Life Assurance |

|---|---|---|

| Duration of Coverage | Fixed Term | Whole Life |

| Premium Amount | Premium is lower than Life Assurance | Premium is higher than Life Insurance |

| Coverage Validity | No coverage after the term ends | No term. Whole life coverage |

| Payout Condition | The sum assured is paid out only if the insured person dies during the policy term | The sum assured is paid out whenever the insured person dies |

| Flexibility of Sum Assured | The sum assured can be decreased | The sum assured cannot be decreased. |

Life insurance and assurance work in the same way and are similar to any insurance policy. You pay a premium and get a financial risk covered in return. The risk differs in the type of policy-health, life, and motor.

In life insurance and assurance, the risk is similar in nature. In case of your unfortunate demise, your family will face financial challenges apart from the grief of losing you. The financial challenges could be severe if you are the sole/significant breadwinner of the family.

The premium paid is used by the insurance company to cover the financial loss so that the family can sustain its livelihood. The insurance company pays the “sum assured”, which is defined in advance, to your nominee, on your unfortunate demise.

Life insurance policies have affordable premiums and are light on the pocket. The benefits far outweigh the premiums that you pay. This contribution is worthwhile because death is unpredictable.

For example, Ramesh is 40 years old and earns about ₹ 12 lakhs per annum. He has no known illnesses and his medical history is clear. He avails a pure life insurance policy of 20 years tenure, also called the “term plan” with a sum assured of ₹ 1 crore.

If Ramesh passes away at 58, his nominee is paid the sum assured. However, if Ramesh passes away at 65, no sum assured is paid out because the term of the policy is 20 years.

Ramesh is 40 years old and earns about ₹ 12 lakhs per annum. He has no known illnesses and his medical history is clear. He avails a life assurance policy, with a sum assured of ₹ 1 crore. Ramesh passes away at the age of 75. His family is paid the sum assured of Rs 1 crore.

Saving money to build a corpus is a time-tested method to plan your future. This method is definitely useful in creating wealth, albeit, in the long run. What if, life has some other plans for you? Risks to life and health do not come with advance notification.

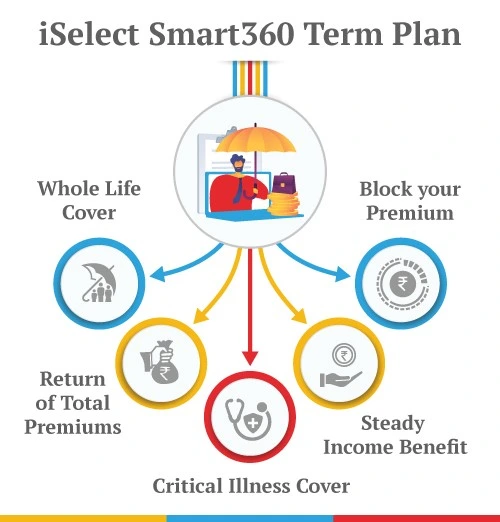

Canara HSBC Life Insurance offers the iSelect Smart360 Term Plan that offers features which combine the benefits of term life insurance and whole life insurance:

You can also choose other features to help you maintain an adequate life cover without having to buy a new term life cover. Apart from this the plan also gives you the option to cover your homemaker or employed spouse under the same plan.

Term life insurance is ideal if you are exploring insurance coverage only for a specific period.

Let’s say you are 40 and have a 10-year-old child. You want an “income-replacement” risk cover until your child grows up and starts earning on his/her own. A 15-20-year term policy should be sufficient because your child would be 25-30 years of age by then.

Term insurance plans are more affordable as compared to whole-life plans. If you cannot invest in higher premiums, you can buy a term plan.

Click here to use - Term Insurance Premium Calculator

If you are the sole income earner in your family, your untimely demise can bring your family to a standstill.

A life insurance policy can come to their rescue so that they do not face any hardships. Your timely contribution in the form of a premium can play an important role in your family’s well-being forever.

While both life insurance and life assurance offer financial protection, they cater to slightly different needs. Term life insurance is best suited for individuals seeking cost-effective coverage for a specific time frame, ensuring income replacement during crucial years. Life assurance, or whole life insurance, offers lifelong coverage and can help create a financial legacy for loved ones.

Choosing between the two depends on your financial goals, responsibilities, and how long you want the protection to last. By understanding how each works, you can make a more informed decision that aligns with your long-term plans and your family’s future needs.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.