Written by : Knowledge Centre Team

2025-12-21

891 Views

5 minutes read

Share

You work hard and earn a living so that you can take care of the needs and goals of you and your family members. One such goal you work for is Retirement. You hustle during your work life so that you live happily and stress-free post your retirement.

After retirement, you can spend more time with your family, travel to some beautiful destinations and try new hobbies, etc. But with the enjoyable part of retirement, there come financial challenges too.

You no longer receive any external source of income when you retire. You have your savings and other investments (if made) to rely upon. Thus, you have to make sure you have saved enough and have a big corpus at your disposal.

Other challenges that arise with retirement are:

So, with these challenges of retirement, you must buy yourself a plan that keeps you protected against these challenges and that too for a longer period.

Whole life insurance can be a good alternative.

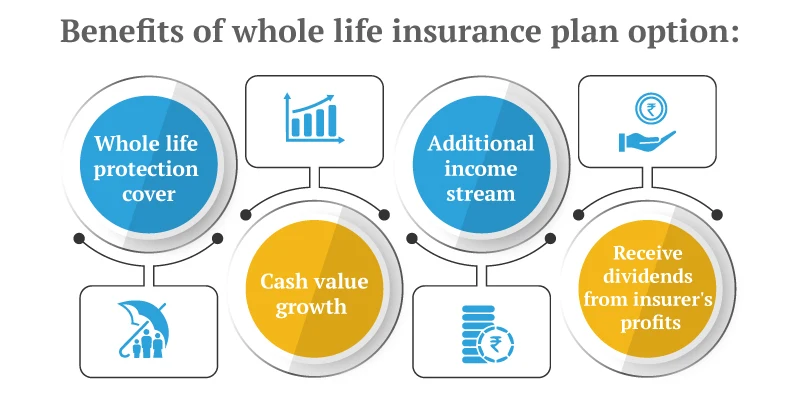

As the term itself suggests, whole life insurance is a type of life insurance plan which covers you for as long as you live. These plans require you to pay premiums for a limited period and in turn provide you with death benefits as well as maturity/survival benefits. This is based on the fact that you pay regular premiums.

For example, at the age of 30, you decide to buy a whole life insurance policy for yourself. Your premium payment term is of 30 years. So, under this, you will have to pay premiums only till you turn 60 and you will be covered for as long as you live.

After you buy a whole life insurance policy, you must be interested in knowing the working of it. Here’s how it works:

Whole life insurance plans which can build cash value and has chances to increase your investment’s value can be seriously considered if you are planning for your retirement.

In India, Whole life insurance plans are essentially term plans that provide you with extended life coverage. Some ULIPs also provide you with the option to extend your cover. Here is how these can help.

Term life insurance policies require you to pay a premium to the insurance companies to keep your policy running.

Various term plans like Canara HSBC Life Insurance iSelect Smart360 Term Plan have a feature of return of premiums. The amount that you have paid towards the premium over the years will be added to your fund at maturity. This gives an extra boost to your corpus when you retire.

Whole life ULIPs also offer you a partial withdrawals facility. You can withdraw the amount from the fund’s value. In retirement, these features come in handy when you face an emergency and need urgent money.

Partial withdrawals made after the lock-in period (5 years in most ULIPs) are completely tax-free. In policies like Promise4Growth Plus, there is no limit on the number of partial withdrawals you can make.

Buying term insurance with an extended life cover helps you build an asset that will come in handy in your retirement. The sum assured to be received is certain. This can be used to achieve your family’s needs and goals. Here is how it can help

Policies like iSelect Smart360 Term Plan provide you with a guaranteed surrender value or a special surrender value if you decide to quit it before maturity.

You are eligible to avail of tax deductions up to Rs 1.5 lakh for the premiums paid towards your term life insurance as per Section 80C of the Income Tax Act 1961. Thus, your tax liability is decreased. Also, the maturity benefit that you will receive is exempt from tax under section 10(10)D.

Apart from these, the loans you take against the policy are also tax-free.

Now that you know how a whole life insurance plan can prove to be a good asset considering your retirement, the next question that would arise will be regarding the right time of buying life insurance.

Well, the earlier you decide to buy the better it will be for you. This is because of the following reasons:

Thus, depending on the type of whole life insurance you buy, you have access to multiple benefits. Some of these, like the return of premium and partial withdrawals, can be greatly supportive during retirement.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.