Written by : Knowledge Centre Team

2026-01-08

887 Views

7 minutes read

Share

Well-being and the safety of your family always remain your topmost priority. You work hard and earn a living to make sure that you have enough wealth to help your family members achieve their goals. Life insurance is a class of financial instruments that can help you fulfil your financial obligations to your family.

Life insurance is the answer to questions like - What if something happens to you? Who will then take care of your loved ones? How will they look after their needs and goals?

With such an important place, a life insurance plan is a financial term you should know almost everything about. Let’s dive deeper into the details in this blog.

Key Takeaways

|

The purpose of life insurance is to protect your family’s future in your absence. Life insurance becomes necessary if you are the breadwinner for the family. It gives you peace of mind, and your family will be secured financially.

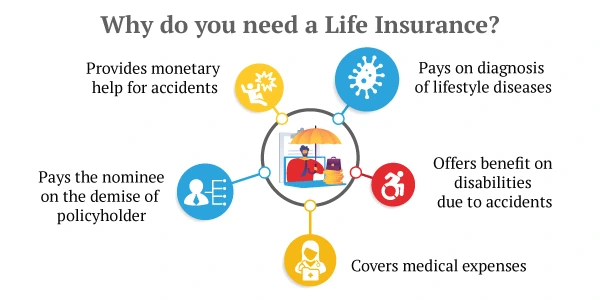

However, safety is not the only reason to have life insurance. Here are a few important reasons why life insurance is a must for you:

a. Long-term financial protection of your dependents

b. Building tax-free wealth over a long time

c. Funding your retirement

d. Preserving your money from inflation and taxes

e. Generating tax-free income

Life insurance has an investment solution for each important financial milestone you need to cover in life like a child’s goal and retirement. Thus, for one reason or the other, you will need life insurance.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Providing life cover to you is the major benefit of life insurance, but surely not the only one. Here are other things life insurance brings to the table.

Based on your financial goal, you can choose a different type of life insurance plan. Here are the most popular types of life insurance plans in India:

Now that you're familiar with the various types of life insurance, it's also important to understand the associated terms. These terms remain almost the same in all the life insurance policy types:

Life insurance is the best investment you can make to ensure the financial safety of your loved ones. Also, there is no single period in which life insurance is beneficial. It is important at every stage of your life, be it your early twenties, or when you are married and expecting to have a child. Life insurance plays a huge part.

By choosing Canara HSBC Life Insurance, you gain access to flexible plans, reliable coverage, and investment-linked options such as ULIPs that help you achieve both protection and wealth creation goals. The right policy ensures that no matter what life brings, your family’s dreams and lifestyle remain safeguarded.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.