Written by : Knowledge Centre Team

2026-07-30

1306 Views

7 minutes read

Share

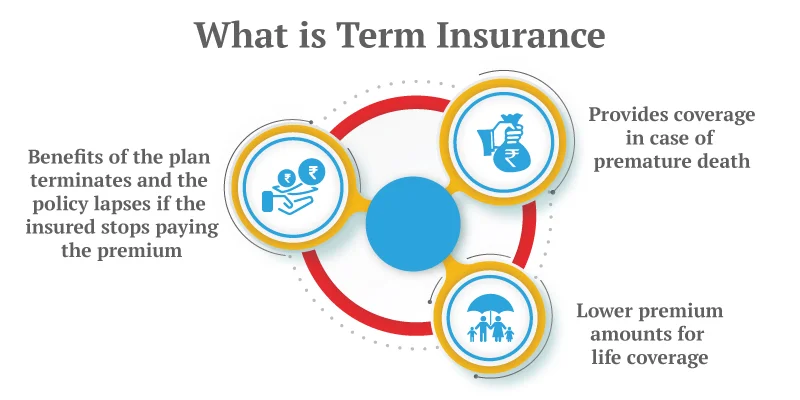

Term insurance plans are no longer simply paying for life cover plans. They have features which can make yours and your dependents’ lives more manageable. Do you have a term insurance cover? Have you explored all the benefits and the new way in which you can avail of a term life insurance plan?

If not, here’s a step-by-step process to help you buy the best term plan online.

Key Takeaways

|

Nowadays, everything is available online, not just for learning, but you can also buy almost anything from the comfort of your own home. Here are five easy steps that will guide you to the term insurance plan that suits your needs the best:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

This is easier said than done. Thus, a better option is to let the benefit payout happen in a regular mode. With iSelect Smart360 Term Plan by Canara HSBC Life Insurance, you can choose a growing income option for your family.

For example, in the case of Sandeep, he could divide his sum assured of ₹1 crore into a lump sum and regular income mode in a ratio of 50:50. This will ensure:

A lump sum of ₹50 lakh, which the spouse can invest to meet the child’s future goals and pay off any liabilities.

A regular income of about ₹35,000 (slightly more than current expenses), which will also grow each year by ₹3500 (10% simple interest) to account for inflation.

Check your existing life insurance plan and see how many of these benefits are available to you, and determine which one to buy.

Choosing a term insurance plan is about customising the cover to match your family’s present and future needs. It gives your loved ones financial support even when life takes unexpected turns. The good news is that most of these options are now available online, making the entire process easier, faster, and more transparent. Whether you are buying it for the first time or planning to upgrade your current plan, take the time to compare and understand what suits your life stage best.

We not only offer a secure online platform to purchase term plans like iSelect Smart360 Term Plan by Canara HSBC Life Insurance, but also peace of mind regarding your loved ones' security. Our 99.52% claim settlement ratio is a testament to our reliability.

Make a smart choice today to protect your family’s dreams tomorrow.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.