Written by : Knowledge Centre Team

2025-12-05

3975 Views

6 minutes read

Share

Your expenses, throughout your life, follow a cyclical trend. They vary depending on life’s circumstances and different milestones that are reached.

For example, your child has secured admission to a top-notch Indian or international university, and you have taken out a huge loan to finance their education. Although repayments typically begin post-completion of the programme, most banks expect payment of interest during such “moratorium” periods. This repayment can spike your expenses at least until your child secures stable employment.

There could be similar intermittent expenses, such as a car loan or wedding expenses etc. When you are in stable employment, you can easily manage your finances. However, in case of the policyholder’s unfortunate absence, a term insurance plan will be a shield for the family against financial distress.

Key Takeaways

|

The 5-year term life insurance policy is a short-term version of the typical long-term life insurance plan. Term life insurance is typically a long-term financial protection cover for your family, which can have a tenure of over 40 years.

A term life insurance plan is a pure protection plan that offers a benefit amount to your nominees upon the policyholder’s untimely demise. Any unfortunate event can be stressful for the family, both emotionally and financially. If the policyholder is the primary breadwinner, the family would require a financial cushion to rely on.

A term insurance plan helps your family continue with their lives and manage their financial position. This plan secures an adequate sum assured for your family at a nominal premium cost.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

A 5-year term life insurance works the same as the standard term insurance plan. However, the cover is only available for a short period. It is also a reason why both plans have similar primary features. Some of the salient features of a 5-year term plan are:

A 5-year term life insurance policy covers you for a period of five years. These plans are appropriate for individuals who have financial commitments and have dependents who would require financial support in case of an unfortunate event. The death benefit of a 5-year term plan can ensure a financially stress-free life for the family.

Individuals approaching mid-life can also buy this policy, provided they are medically fit to be offered a term life cover. Individuals with limited or lower levels of income can also buy this insurance plan because the premium is lower compared to whole life plans or longer-term plans.

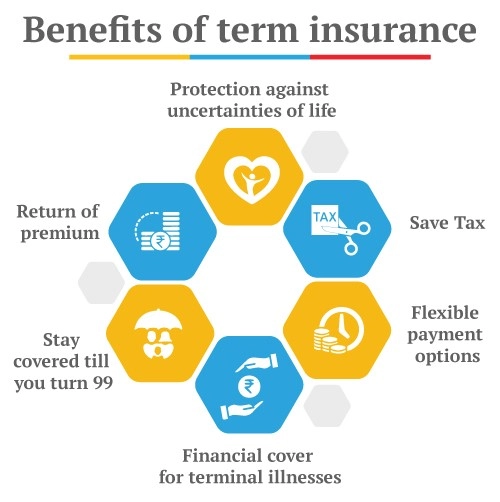

Some of the benefits of 5-year term plans are listed below:

The 5-year term life insurance plan differs from the standard term insurance plan to the extent of its usage. The following table provides the details:

| Parameter | 5-Year Term Plan | Long Term Plan |

|---|---|---|

Tenure | 5 years | 10 years to 99 – Age at purchase |

Useful for | Short-Term Financial Obligations | Corpus for Family to Maintain Lifestyle |

Premiums | More affordable as compared to a long-term plan | Premium increases with tenure |

Create Inheritance | Usually not meant for this | Useful to create an inheritance |

Death Benefit | Can be limited to the covered specific financial obligation/liability | Should be at least 10 times the annual income of the insured |

A sum assured equal to 10 times your annual income is usually sufficient for this purpose. However, in the case of a 5-year term life insurance policy, it will help you secure your family from a short-term liability. For example, a 5-year loan for home improvement. Thus, you should check for certain specific features of such a plan that can help look after your objective of buying short-term life insurance:

You can buy the 5-year term life insurance online or offline once you are satisfied with the above parameters.

A 5-year life insurance plan is best-suited to meet short-term financial obligations. However, you should also consider having a standard term life cover for your family. It will help offer adequate cover for your dependents with the amount necessary for maintaining their living standards and meeting their goals.

At Canara HSBC Life Insurance, we offer flexible term plans, which allow you to customise your cover, add your spouse, and even opt for return of premium benefits. Backed by a consistently high claim settlement ratio of 99.4%, you can trust us to stand by your family when it matters most. In fact, our online support channels are easily accessible, along with 15,700 partner branches for offline visits.

Make short-term protection a long-term advantage by choosing a partner who values your trust and future.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.