Written by : Knowledge Centre Team

2025-11-02

4899 Views

7 minutes read

Share

Term Insurance is considered the purest and simplest form of life insurance. It helps in making your family financially secure and stable in your absence. A few key traits of a term insurance plan are very clear, such as a low premium cost. However, you should expect more from your term insurance.

If any unexpected things happen, the nominee(s) (as chosen by the person) will get the assured amount of money. Now, with the best term insurance plans, you can have certain expectations. Before that, let's understand the working of a term insurance.

Key Takeaways

|

A term insurance plan is designed to offer financial protection to your family in case something happens to you during the policy period. You pay a fixed premium regularly, and in return, you get the lump sum amount, known as the sum assured. Let’s break down how it works.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

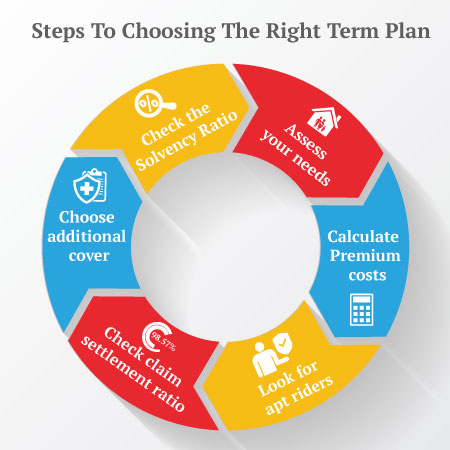

Here are the seven most useful expectations you should have from your term plan:

It is easy to see the financial contribution of the earning spouse to the family. But the non-earning spouse also contributes a lot to the family. However, it is difficult to put in financial terms, the absence of the non-earning spouse may also result in an increased financial burden.

Thus, the best term insurance plans not only cover the earning member of the family but also the non-earning one.

The term insurance also gives you the option of joint cover. The joint cover implies that both partners are the owners of this policy are covered under the same policy. In case anything happens to any partner, the family doesn’t suffer any financial setback. In other words, with a good term life policy, the homemaker also gets the term cover.

In a nutshell, the family with a term insurance plan gets good financial security in the absence of the earning member. The iSelect Smart360 Term Plan by Canara HSBC Life Insurance can meet all seven expectations above.

Term insurance plans can offer far more than just a comfortable survival for your family after your untimely demise. Term insurance remains the ray of hope for families even when they lose the breadwinner, as owning this policy.

Ideally, the term insurance should offer ‘enough money for your family to sustain their life if anything unfortunate befalls you, it provides adequate cover to you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.