Written by : Knowledge Centre Team

2025-12-12

795 Views

7 minutes read

Share

The first paycheque, no matter how small, puts your faith back on the pedestal that yes you can make it happen in time. It also brings about a lot of excitement, expectations and a fog of confusion about the things you should do with it. Being a finite amount, unlike your aspirations, the cheque limits your options.

Therefore, you must prioritise. In summary, you only have three choices with this money:

Your journey has just begun into the financial world, and we are here to help you set your priorities straight.

Provided that your primary role is not of an investment manager, you will not need to know the nitty-gritty of every investment plan. However, you do need to know how to prioritise your outflows so that you can have a prosperous and comfortable financial future.

The first part is the relation between your current income and your future wealth, i.e. Your current savings are proportional to your future wealth. In this scenario, the only real choice you have is about your present expenses. The more controlled your current expenses, the higher your savings will be, and so on.

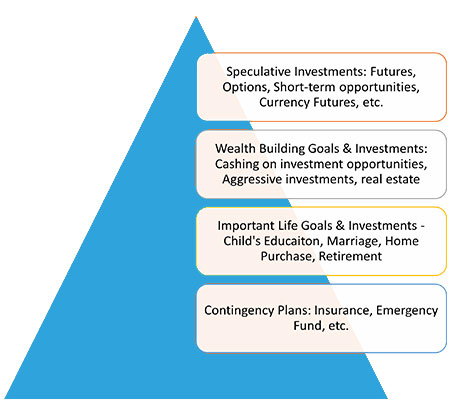

The second part is about what to do with your savings. So, here’s your financial needs pyramid:

The priority starts at the bottom. That is the foundational level, and as your surplus increases so does your choice of investment avenues.

As per this pyramid, you need to start with contingency planning; i.e. securing yourself against the uncertainties of life. You can transfer the risk of the financial burden for some of these uncertainties while others you will need to bear.

Here’s a list of uncertain and financially taxing situations and how you can survive them:

So, out of your first paycheque, the saved money should be directed towards insurance first, then towards the emergency fund. The size of this emergency fund can be anywhere between three to six months of your income.

Once your emergency fund pool is ready and all insurance plans are in place, you can start planning for your long-term goals.

You can buy the term insurance cover completely online. All you need to do is use the online term plan calculator to check your term insurance need and calculate your premium. The part where you need to be thoughtful is while selecting the benefits under the plan.

So, here you will need to know a little about the plan, what it covers and how it works. You might have to make the following choices –

You should select a policy term which at least covers your life until your retirement. However, given the present employment scenarios, a little longer cover would be better. Although, in any circumstance try to keep your premium payment term only up to 60.

Once you have selected all these options, you will see your premium. You can change the frequency of premium payment to check the amount with your preferred mode of payment

Premium calculation is just the beginning of the term insurance purchase process. After you are satisfied with the estimated premium amount and benefits, go ahead and pay the premium. After successful payment, you will need to fill the proposal form.

Try to provide as accurate information as possible and attach related proofs and documents as asked. After you have submitted the application form and documents, you may receive the appointment options for a medical check-up at a nearby clinic.

This is a necessary step to avoid any complication in case of a claim. The insurer may take a few days to issue the policy after your medical exam.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.