Written by : Knowledge Centre Team

2025-10-09

3889 Views

7 minutes read

Share

Mortality Protection Gap or MPG is a data that is released by the world’s largest re-insurer, Swiss-Re every year. MPG shows the gap between the required financial protection and present life cover of the people in a country.

According to the latest data (2020), Indian people have the largest MPG of about 83%. This means if they need a term insurance plan of Rs. 100, they only have about Rs. 17 as the sum assured in their term insurance plans.

With such overall statistics, when it comes to women in the country, their participation is even lower whether earning or not. Now one of the big reasons is that India is still dominated by single-income families.

Thus, the life insurance majorly concerns the male member of the family who is earning. Does this mean that women in double-income families are buying adequate term insurance?

Probably not, as the Swiss-Re study points out. Even when women are the breadwinner in the family they tend to prioritise health over life. So, either they do not feel the need to buy term insurance or get a small life cover plan.

Even after buying many discontinue the policy after a few years considering term insurance cover to be unimportant.

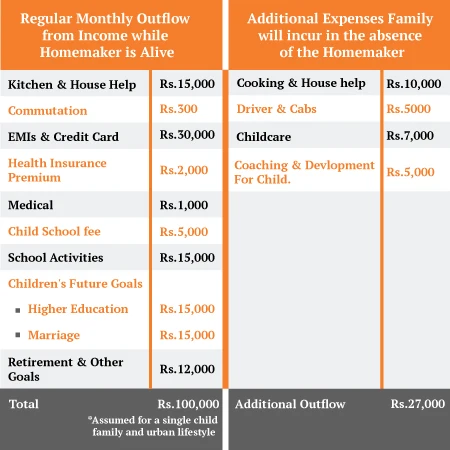

There cannot be a greater myth than that the homemaker does not have financial value for the family. Although it is difficult to estimate the value, it’s not impossible.

Estimating the economic value of a homemaker without a formal income needs the replacement method of calculation.

For example, homemakers contribute to the family and children’s welfare, and in their absence all of it must be replaced. But most of these replacement services will cost money:

If your family’s monthly budget looks something similar to the table above, you can see the impact of the additional outflow. You will need to adjust that extra Rs. 27,000 within your monthly budget.

This will directly impact your investments towards your children’s and your own financial goals. Unless the homemaker also has a term insurance plan with adequate life cover.

You may find the premium slightly high for this term insurance cover. But, in any case, you should have a life cover which is at least 10 times your annual take-home income; i.e. Rs. 1.2 Crore in the example above.

Term insurance or life cover is important but definitely not sufficient financial protection for your family. You should always consider additional benefits or riders with the term insurance plan.

You can buy riders like personal accident and critical illness cover with your term cover and enhance your family’s financial safety.

You can use certain features offered by the term insurance plans, for instance the iSelect Smart360 Term Plan, to ensure a financially less stressful time for your family:

Not really. This is the most promising feature of a term insurance cover, especially when you are younger. For example, Rs. 1 crore term plan will cost about Rs. 5500 a year if you are 30 years old female. If you choose to pay this premium every month, you will not even feel its presence (i.e. Rs. 500 p.m.) in your monthly budget.

Single-Premium Option

In fact, if you feel that a commitment of the next 30 years for premium is too much, you can even choose to pay the entire premium in one instance. You pay a little over Rs. 1 lakh for a life cover of Rs. 1 crore, which continues till you are 60.

Do you see any more reasons to not have adequate financial protection for your family?

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.